Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Nuevos Desarrollos

en Teoría del Comercio Internacional

y su Análisis Empírico

Timothy J. Kehoe

University of Minnesota y Federal Reserve Bank of Minneapolis

Universitat de Barcelona

Mayo 2006

www.econ.umn.edu/~tkehoe/ub-06.html

Outline:

1. Standard theory (hybrid Heckscher-Ohlin/New Trade Theory)

does not well when matched with the data on the growth and

composition of trade.

2. Applied general equilibrium models that put the standard theory

to work do not well in predicting the impact of trade

liberalization experiences like NAFTA.

3. Much of the growth of trade after a trade liberalization

experience is growth on the extensive margin. Models need to

allow for corner solutions or fixed costs.

4. Modeling the fixed costs may explain why real exchange rate

data indicate that more arbitrage across countries that have a

strong bilateral trade relationship.

5. The major determinant of large macroeconomic fluctuations in

Mexico is fluctuations in total factor productivity. If trade

liberalization and the 1995 financial crisis have had large

macroeconomic effects, it is through their effects on TFP.

1. Standard theory (hybrid Heckscher-Ohlin/New Trade

Theory) does not well when matched with the data on the

growth and composition of trade.

In the 1980s and 1990s trade economists reached a consensus that

North-North trade — trade among rich countries — was driven by

forces captured by the New Trade Theory and North-South trade

— trade between rich countries and poor countries — was driven

by forces captured by Heckscher-Ohlin theory. (South-South trade

was negligible.)

A. V. Deardorff, “Testing Trade Theories and Predicting Trade

Flows,” in R. W. Jones and P. B. Kenen, editors, Handbook of

International Economics, volume l, North-Holland, 1984, 467-517.

J. Markusen, “Explaining the Volume of Trade: An Eclectic

Approach,” American Economic Review, 76 (1986), 1002-1011.

In fact, a calibrated version of this hybrid model does not

match the data.

R. Bergoeing and T. J. Kehoe, “Trade Theory and Trade Facts,”

Federal Reserve Bank of Minneapolis, 2003.

TRADE THEORY

Traditional trade theory — Ricardo, Heckscher-Ohlin — says

countries trade because they are different.

In 1990 by far the largest bilateral trade relation in the world was

U.S.-Canada. The largest two-digit SITC export of the United

States to Canada was 78 Road Vehicles. The largest two-digit

SITC export of Canada to the United States was 78 Road Vehicles.

The New Trade Theory — increasing returns, taste for variety,

monopolistic competition — explains how similar countries can

engage in a lot of intraindustry trade.

Helpman and Krugman (1985)

Markusen (1986)

TRADE THEORY AND TRADE FACTS

x Some recent trade facts

x A “New Trade Theory” model

x Accounting for the facts

x Intermediate goods?

x Policy?

How important is the quantitative failure of the New

Trade Theory?

Where should trade theory and applications go from

here?

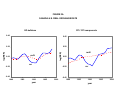

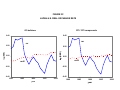

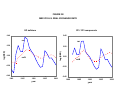

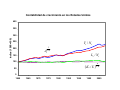

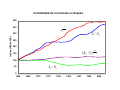

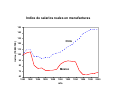

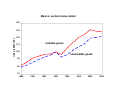

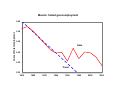

SOME RECENT TRADE FACTS

x The ratio of trade to product has increased.

World trade/world GDP increased by 59.3 percent 1961-1990.

OECD-OECD trade/OECD GDP increased by 111.5 percent

1961-1990.

x Trade has become more concentrated among industrialized

countries

OECD-OECD trade/OECD-RW trade increased by 87.1 percent

1961-1990.

x Trade among industrialized countries is mostly intraindustry

trade

Grubel-Lloyd index for OECD-OECD trade in 1990 is 68.4.

Grubel-Lloyd index for OECD-RW trade in 1990 is 38.1.

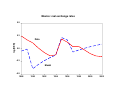

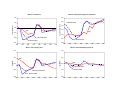

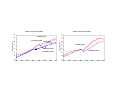

OECD-OECD Trade / OECD GDP

0.12

0.10

0.08

0.06

0.04

0.02

0.00

1960

1963

1966

1969

1972

1975

year

1978

1981

1984

1987

1990

OECD-OECD Trade / OECD-RW Trade

1.80

1.60

1.40

1.20

1.00

0.80

0.60

0.40

0.20

0.00

1960

1963

1966

1969

1972

1975

year

1978

1981

1984

1987

1990

Helpman and Krugman (1985):

“These....empirical weaknesses of conventional trade

theory...become understandable once economies of scale and

imperfect competition are introduced into our analysis.”

Markusen, Melvin, Kaempfer, and Maskus (1995):

“Thus, nonhomogeneous demand leads to a decrease in NorthSouth trade and to an increase in intraindustry trade among the

northern industrialized countries. These are the stylized facts that

were to be explained.”

Goal: To measure how much of the increase in the ratio of

trade to output in the OECD and of the concentration of world

trade among OECD countries can be accounted for by the

“New Trade Theory.”

PUNCHLINE

In a calibrated general equilibrium model,

the New Trade Theory cannot account for the

increase in the ratio of trade to output in the

OECD.

Back-of-the-envelope calculations:

Suppose that the world consists of the OECD and the only trade is

manufactures.

With Dixit-Stiglitz preferences, country j exports all of its

production of manufactures Ymj except for the fraction s j Y j / Y oe

that it retains for domestic consumption.

World imports:

M

World trade/GDP:

M

Y oe

World trade/GDP:

n

¦j

M Ymoe

Ymoe Y oe

j

j

1

s

Y

m.

1

1 ¦

n

j

oe

Y

j 2

m

s

(

)

.

oe

1

Y

M

Y oe

n

M Ymoe

Ymoe Y oe

1 ¦

n

j

oe

Y

j 2

m

s

(

)

.

oe

1

Y

1 ¦ j 1 ( s j ) 2 goes from 0.663 in 1961 to 0.827 in 1990.

Ymoe / Y oe goes from 0.295 in 1961 to 0.222 in 1990.

0.663 u 0.295 0.196 | 0.184 0.827 u 0.222 .

Effects cancel!

A “NEW TRADE THEORY” MODEL

Environment:

x Static: endowments of factors are exogenous

x 2 regions: OECD and rest of world

x 2 traded goods: homogeneous — primaries (CRS) and

differentiated — manufactures (IRS)

x 1 nontraded good — services (CRS)

x 2 factors: (effective) labor and capital

x Identical technologies and preferences (love for variety) across

regions

x Primaries are inferior to manufactures

We only consider merchandise trade in both the data and in

the model.

Key Features of the Model

Consumers' problem:

max

s.t.

E p (c pj J p )K E m ( ³ cmj ( z ) U dz p )K / U E s (csj J s )K 1

Dw

K

q p c pj ³ w qm ( z )cmj ( z )dz p qsj csj d r j k j w j h j .

D

Firms' problems

Primaries and Services: Standard CRS problems.

Ypj

T p ( K pj )D p ( H pj )1D p

Ys j

Ts ( K sj )D s ( H sj )1D s

Manufactures: Standard (Dixit-Stiglitz) monopolistically

competitive problem:

x Fixed cost.

Ym ( z )

max ª¬Tm K m ( z )Dm H m ( z )1Dm F ,0 º¼

x Firm z sets its price qm ( z ) to max profits given all of the

other prices.

n

Ym ( z ) ¦ j 1 Cmj ( z ) Cmrw ( z ) .

1

1K

Cmj ( z )

Em (r j K j w j H j q p J p N j qsj J s N j )

1

1U

U

1U

qm ( z ) ª ³ D w qm ( z c) dz cº

¬

¼

UK

U (1K )

(1U )

U

K

1K

'

U

K

1

ª

º

1U

1K 1K

'

Em « ³ w qm ( z c) dz c

» E s qs

D

¬

¼

x Every firm is uniquely associated with only one variety

(symmetry).

x Free entry.

[0, d w ] with d w finite and endogenously determined.

x Dw

K

1K

E p qp

1

1K

1

1K

Volume of Trade

Let s j be the share of country j , j

production of manufactures,

sj

³D

j

1,..., n, rw , in the world

Ym ( z )dz / ³D w Ym ( z )dz

Ymj / Ymw .

The imports by country j from the OECD are

M oej (1 s rw s j )Cmj

M oerw (1 s rw )Cmrw .

Total imports in the OECD from the other OECD countries are

n

M

oe

oe

n

j 2

rw

oe

M

(1

s

(

s

)

/(1

s

))

C

¦

¦

m .

j

oe

j 1

rw

j 1

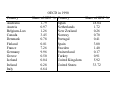

OECD in 1990

Country

Australia

Austria

Belgium-Lux

Canada

Denmark

Finland

France

Germany

Greece

Iceland

Ireland

Italy

Share of GDP %

1.79

0.97

1.26

3.45

0.78

0.81

7.26

9.96

0.50

0.04

0.28

6.64

Country

Japan

Netherlands

New Zealand

Norway

Portugal

Spain

Sweden

Switzerland

Turkey

United Kingdom

United States

Share of GDP %

18.04

1.72

0.26

0.70

0.41

3.00

1.40

0.17

0.91

5.92

33.72

ACCOUNTING FOR THE FACTS

Compare the changes that the model predicts for 1961-1990 with

what actually took place.

Focus on key variables:

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manfacturing GDP/OECD GDP

Calibrate to 1990 data.

Backcast to 1961 by imposing changes in parameters:

relative sizes of countries in the OECD

populations

sectoral productivities

endowments

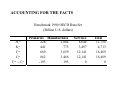

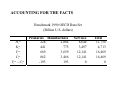

ACCOUNTING FOR THE FACTS

Benchmark 1990 OECD Data Set

(Billion U.S. dollars)

H ioe

K ioe

Yi oe

Cioe

Yi oe Cioe

Primaries Manufactures

228

2,884

441

775

669

3,659

862

3,466

-193

193

Services

8,644

3,497

12,141

12,141

0

Total

11,756

4,713

16,469

16,469

0

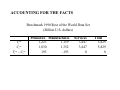

ACCOUNTING FOR THE FACTS

Benchmark 1990 Rest of the World Data Set

(Billion U.S. dollars)

Yi rw

Cirw

Yi rw Cirw

Primaries Manufactures

1,223

1,159

1,030

1,352

193

-193

Services

3,447

3,447

0

Total

5,829

5,829

0

ACCOUNTING FOR THE FACTS

x N oe

x

¦

i

854 , N rw

rw

Y

p ,m , s i

x Set q p qm ( z )

values).

xU

4, 428 .

¦

i

rw

C

p ,m , s i

qs

w

5,829 .

r

1 (quantities are 1990

1/1.2 (Morrison 1990, Martins, Scarpetta, and Pilat 1996).

x Normalize d w

100 .

x Calibrate H rw , K rw so that benchmark data set is an

equilibrium.

x Alternative calibrations of utility parameters J p , J s , and K .

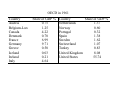

OECD in 1961

Country

Austria

Belgium-Lux

Canada

Denmark

France

Germany

Greece

Iceland

Ireland

Italy

Share of GDP %

0.75

1.25

4.22

0.70

6.99

9.71

0.50

0.03

0.21

4.64

Country

Share of GDP %

Netherlands

1.37

Norway

0.60

Portugal

0.32

Spain

1.38

Sweden

1.62

Switzerland

1.07

Turkey

0.83

United Kingdom

8.08

United States

55.74

Numerical Experiments

Calculate equilibrium in 1961:

T p ,1961

T m ,1961

T s ,1961

N oe

T p ,1990

T m ,1990 /1.01429 , F1961

F1990 /1.01429

T s ,1990 /1.00529 (Echevarria 1997)

536, N rw

2,545

Numerical Experiments

oe

oe

rw

rw

Choose H1961

, K1961

, H1961

, K1961

so that

¦

¦

¦

¦

i

oe

oe

Y

/

N

1990

p ,m , s i ,1990

oe

i p ,m , s i ,1961

Y

i

oe

1961

/N

rw

rw

Y

/

N

1990

p ,m , s i ,1990

rw

i p ,m , s i ,1961

Y

rw

1961

/N

oe

oe

K1961

K1990

oe

oe

H1961

H1990

q p ,1961 (Yprw,1961 C prw,1961 )

¦

i p ,m , s

rw

i ,1961 i ,1961

q

Y

2.400

2.055

0.050

How Can the Model Work in Matching the Facts?

x The ratio of trade to product has increased:

The size distribution of countries has become more equal

(Helpman-Krugman).

x Trade has become more concentrated among industrialized

countries:

OECD countries have comparative advantage in manufactures,

while the RW has comparative advantage in primaries.

Because they are inferior to manufactures, primaries become

less important in trade as the world becomes richer

(Markusen).

How Can the Model Work in Matching the Facts?

x Trade among industrialized countries is largely intraindustry

trade:

OECD countries export manufactures. Because of taste for

variety, every country consumes some manufactures from

every other country (Dixit-Stiglitz).

x The different total factor productivity growth rates across

sectors imply that the price of manufactures relative to

primaries and services has fallen sharply between 1961 and

1990. If price elasticities of demand are not equal to one, a lot

can happen.

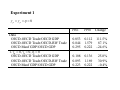

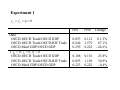

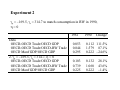

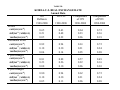

Experiment 1

Jp

Jp K

0

Data

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

1. Jp = 0, Js = 0, K = 0

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

1961

1990

Change

0.053

0.844

0.295

0.112

1.579

0.222

111.5%

87.1%

24.6%

0.108

0.893

0.223

0.136

1.169

0.222

25.8%

30.9%

0.4%

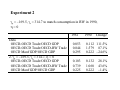

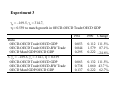

Experiment 2

Jp = 169.5, Js = 314.7 to match consumption in RW in 1990,

K=0

1961

Data

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

2. Jp = 169.5, Js = 314.7, K = 0

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

1990

Change

0.053

0.844

0.295

0.112 111.5%

1.579 87.1%

0.222 24.6%

0.103

0.739

0.225

0.132

1.060

0.222

28.1%

43.6%

1.4%

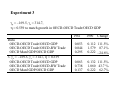

Experiment 3

Jp = 169.5, Js = 314.7,

K = 0.559 to match growth in OECD-OECD Trade/OECD GDP

1961

Data

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

3. Jp = 169.5, Js = 314.7, K = 0.559

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

1990

Change

0.053

0.844

0.295

0.112 111.5%

1.579 87.1%

0.222 24.6%

0.063

0.738

0.137

0.132 111.5%

1.060 43.7 %

0.222 62.7%

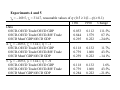

Experiments 4 and 5

Jp = 169.5, Js = 314.7, reasonable values of K ( 0.5 t 1/(1 K ) t 0.1)

1961

1990

Change

Data

OECD-OECD Trade/OECD GDP

0.053

0.112

111.5%

OECD-OECD Trade/OECD-RW Trade

0.844

1.579

87.1%

OECD Manf GDP/OECD GDP

0.295

0.222

24.6%

4. Jp = 169.5, Js = 314.7, K = 1

OECD-OECD Trade/OECD GDP

0.118

0.132

11.7%

OECD-OECD Trade/OECD-RW Trade

0.739

1.060

43.5%

OECD Manf GDP/OECD GDP

0.259

0.222

14.1%

5. Jp = 169.5, Js = 314.7, K = 9

OECD-OECD Trade/OECD GDP

0.118

0.132

1.6%

OECD-OECD Trade/OECD-RW Trade

0.739

1.060

43.5%

OECD Manf GDP/OECD GDP

0.284

0.222

21.8%

Sensitivity Analysis:

Alternative Calibration Methodologies

x Alternative specifications of nonhomogeneity

x Gross imports calibration

x Alternative RW endowment calibration

x Alternative RW growth calibration

x Intermediate goods

INTERMEDIATE GOODS?

Ypj

j

j

ª X j ³ w X mp

º

(

z

)

dz

X

D

1

D

p

p

pp

sp

»

min «

, D

,

, T p K pj H pj amp

asp

«¬ a pp

»¼

Ym ( z )

Ys j

j

ª X j ( z ) ³ w X mm

( z , z ')dz ' X j ( z ) º

pm

«

, D

, sm , »

amm

asm »

min « a pm

«

»

Dm

1D m

F

«¬Tm K m ( z ) H m ( z ) »¼

j

ª X j ³ w X ms

º

j

(

z

)

dz

D

1

D

X

s

s

ps

min «

, D

, ss , Ts K sj H sj »

ams

ass

«¬ a ps

»¼

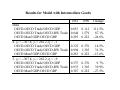

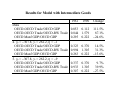

Results for Model with Intermediate Goods

1961

Data

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

4. Jp = 307.8, Js = 262.2, K = 1

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

5. Jp = 307.8, Js = 262.2, K = 9

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

1990

Change

0.053 0.112

0.844 1.579

0.295 0.222

111.5%

87.1%

24.6%

0.323 0.370

0.994 1.305

0.263 0.222

14.5%

31.3%

15.6%

0.337 0.370

0.933 1.305

0.307 0.222

9.7%

39.9%

27.5%

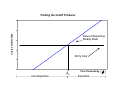

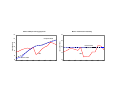

POLICY?

In a version of our model with n OECD countries, a manufacturing

sector, and a uniform ad valorem tariff W, the ratio of exports to

income is given by

M

Y

(n 1)C f

Y

n 1

n 1 (1 W )1/(1 U )

Fixing n to replicate the size distribution of national incomes in the

OECD, and setting U 1/1.2 , a fall in W from 0.45 to 0.05 produces

an increase in the ratio of trade to output as seen in the data.

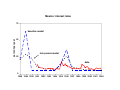

World Trade / World GDP

0.90

0.80

0.70

rho=1/2.0

0.60

0.50

0.40

rho=1/1.5

0.30

rho=1/1.1

0.20

rho=1/1.2

0.10

0.00

0

0.1

0.2

0.3

0.4

0.5

tau

0.6

0.7

0.8

0.9

1

2. Applied general equilibrium models that put the standard

theory to work do not well in predicting the impact of trade

liberalization experiences like NAFTA.

Applied general equilibrium models were the only analytical game in

town when it came to analyzing the impact of NAFTA in 1992-1993.

Typical sort of model: Static applied general equilibrium model with

large number of industries and imperfect competition (Dixit-Stiglitz or

Eastman-Stykolt) and finite number of firms in some industries. In some

numerical experiments, new capital is placed in Mexico owned by

consumers in the rest of North America to account for capital flows.

Examples:

Brown-Deardorff-Stern model of Canada, Mexico, and the United States

Cox-Harris model of Canada

Sobarzo model of Mexico

T. J. Kehoe, “An Evaluation of the Performance of Applied

General Equilibrium Models of the Impact of NAFTA,” in T. J.

Kehoe, T. N. Srinivasan, and J. Whalley, editors, Frontiers in

Applied General Equilibrium Modeling: Essays in Honor of

Herbert Scarf, Cambridge University Press, 2005, 341-77.

Research Agenda:

x Compare results of numerical experiments of models with data.

x Determine what shocks — besides NAFTA policies — were

important.

x Construct a simple applied general equilibrium model and

perform experiments with alternative specifications to determine

what was wrong with the 1992-1993 models.

Applied GE Models Can Do a Good Job!

Spain: Kehoe-Polo-Sancho (1992) evaluation of the performance

of the Kehoe-Manresa-Noyola-Polo-Sancho-Serra MEGA model

of the Spanish economy: A Shoven-Whalley type model with

perfect competition, modified to allow government and trade

deficits and unemployment (Kehoe-Serra). Spain’s entry into the

European Community in 1986 was accompanied by a fiscal reform

that introduced a value-added tax (VAT) on consumption to

replace a complex range of indirect taxes, including a turnover tax

applied at every stage of the production process. What would

happen to tax revenues? Trade reform was of secondary

importance.

Canada-U.S.: Fox (1999) evaluation of the performance of the

Brown-Stern (1989) model of the 1989 Canada-U.S. FTA.

Other changes besides policy changes are important!

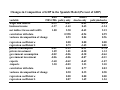

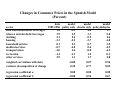

Changes in Consumer Prices in the Spanish Model

(Percent)

sector

food and nonalcoholic beverages

tobacco and alcoholic beverages

clothing

housing

household articles

medical services

transportation

recreation

other services

data

model

model

model

1985-1986 policy only shocks only policy&shocks

1.8

-2.3

4.0

1.7

3.9

2.5

3.1

5.8

2.1

5.6

0.9

6.6

-3.3

-2.2

-2.7

-4.8

0.1

2.2

0.7

2.9

-0.7

-4.8

0.6

-4.2

-4.0

2.6

-8.8

-6.2

-1.4

-1.3

1.5

0.1

2.9

1.1

1.7

2.8

weighted correlation with data

variance decomposition of change

-0.08

0.30

0.87

0.77

0.94

0.85

regression coefficient a

regression coefficient b

0.00

-0.08

0.00

0.54

0.00

0.67

Measures of Accuracy of Model Results

1. Weighted correlation coefficient.

2. Variance decomposition of the (weighted) variance of the

changes in the data:

vardec( y data , y model )

var ( y model )

.

model

data

model

var ( y

) var ( y y

)

3, 4. Estimated coefficients a and b from the (weighted)

regression

xidata

a bximodel ei .

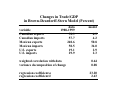

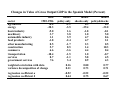

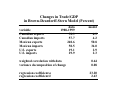

Changes in Value of Gross Output/GDP in the Spanish Model (Percent)

sector

agriculture

energy

basic industry

machinery

automobile industry

food products

other manufacturing

construction

commerce

transportation

services

government services

data

1985-1986

-0.4

-20.3

-9.0

3.7

1.1

-1.8

0.5

5.7

6.6

-18.4

8.7

7.6

weighted correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

model

policy only

-1.1

-3.5

1.6

3.8

3.9

-2.4

-1.7

8.5

-3.6

-1.5

-1.1

3.4

model

model

shocks only policy&shocks

8.3

6.9

-29.4

-32.0

-1.8

-0.1

1.0

5.0

4.7

8.6

4.7

2.1

2.3

0.5

1.4

10.3

4.4

0.4

1.0

-0.7

5.8

4.5

0.9

4.3

0.16

0.11

0.80

0.73

0.77

0.71

-0.52

0.44

-0.52

0.75

-0.52

0.67

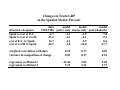

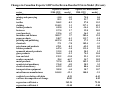

Changes in Trade/GDP

in the Spanish Model (Percent)

direction of exports

Spain to rest of E.C.

Spain to rest of world

rest of E.C. to Spain

rest of world to Spain

data

model

model

model

1985-1986 policy only shocks only policy&shocks

-6.7

-3.2

-4.9

-7.8

-33.2

-3.6

-6.1

-9.3

14.7

4.4

-3.9

0.6

-34.1

-1.8

-16.8

-17.7

weighted correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

0.69

0.02

0.77

0.17

0.90

0.24

-12.46

5.33

2.06

2.21

5.68

2.37

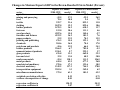

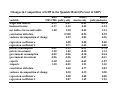

Changes in Composition of GDP in the Spanish Model (Percent of GDP)

variable

wages and salaries

business income

net indirect taxes and tariffs

data

model

1985-1986 policy only

-0.53

-0.87

-1.27

-1.63

1.80

2.50

model

shocks only

-0.02

0.45

-0.42

model

policy&shocks

-0.91

-1.24

2.15

correlation with data

variance decomposition of change

0.998

0.93

-0.94

0.04

0.99

0.96

regression coefficient a

regression coefficient b

private consumption

private investment

government consumption

government investment

exports

-imports

0.00

0.73

-1.23

1.81

-0.06

-0.06

-0.42

-0.03

0.00

-3.45

-0.51

-0.58

-0.38

-0.07

-0.69

2.23

0.00

0.85

-1.78

1.32

-0.44

-0.13

-1.07

2.10

correlation with data

variance decomposition of change

0.40

0.20

0.77

0.35

0.83

0.58

regression coefficient a

regression coefficient b

0.00

0.87

0.00

1.49

0.00

1.24

-0.81

1.09

-0.02

-0.06

-3.40

3.20

Public Finances in the Spanish Model

(Percent of GDP)

data

model

model

model

variable

1985-1986 policy only shocks only policy&shocks

indirect taxes and subsidies

2.38

3.32

-0.38

2.98

tariffs

-0.58

-0.82

-0.04

-0.83

social security payments

0.04

-0.19

-0.03

-0.22

direct taxes and transfers

-0.84

-0.66

0.93

0.26

government capital income

-0.13

-0.06

0.02

-0.04

correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

0.99

0.93

-0.70

0.08

0.92

0.86

-0.06

0.74

0.35

-1.82

-0.17

0.80

Models of NAFTA

Did Not Do a Good Job!

Ex-post evaluations of the performance of applied GE models are

essential if policy makers are to have confidence in the results

produced by this sort of model.

Just as importantly, they help make applied GE analysis a

scientific discipline in which there are well-defined puzzles and

clear successes and failures for alternative hypotheses.

Changes in Trade/GDP

in Brown-Deardorff-Stern Model (Percent)

variable

Canadian exports

Canadian imports

Mexican exports

Mexican imports

U.S. exports

U.S. imports

data

1988-1999

52.9

57.7

240.6

50.5

19.1

29.9

weighted correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

model

4.3

4.2

50.8

34.0

2.9

2.3

0.64

0.08

23.20

2.43

Changes in Canadian Exports/ GDP in the Brown-Deardorff-Stern Model (Percent)

sector

agriculture

mining and quarrying

food

textiles

clothing

leather products

footwear

wood products

furniture and fixtures

paper products

printing and publishing

chemicals

petroleum and products

rubber products

nonmetal mineral products

glass products

iron and steel

nonferrous metals

metal products

nonelectrical machinery

electrical machinery

transportation equipment

miscellaneous manufactures

weighted correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

exports to Mexico

1988–1999

model

122.5

3.1

-34.0

-0.3

89.3

2.2

268.2

-0.9

1544.3

1.3

443.0

1.4

517.0

3.7

232.6

4.7

3801.7

2.7

240.7

-4.3

6187.4

-2.0

37.1

-7.8

678.1

-8.5

647.4

-1.0

333.5

-1.8

264.4

-2.2

195.2

-15.0

38.4

-64.7

767.0

-10.0

376.8

-8.9

633.9

-26.2

305.8

-4.4

1404.5

-12.1

exports to United States

1988–1999

model

106.1

3.4

75.8

0.4

91.7

8.9

97.8

15.3

237.1

45.3

-14.4

11.3

32.8

28.3

36.5

0.1

282.6

12.5

113.7

-1.8

37.2

-1.6

109.4

-3.1

-42.5

0.5

113.4

9.5

20.5

1.2

74.5

30.4

92.1

12.9

34.7

18.5

102.2

15.2

28.9

3.3

88.6

14.5

30.7

10.7

100.0

-2.1

-0.91

0.003

-0.43

0.02

249.24

-15.48

79.20

-2.80

Changes in Mexican Exports/GDP in the Brown-Deardorff-Stern Model (Percent)

sector

agriculture

mining and quarrying

food

textiles

clothing

leather products

footwear

wood products

furniture and fixtures

paper products

printing and publishing

chemicals

petroleum and products

rubber products

nonmetal mineral products

glass products

iron and steel

nonferrous metals

metal products

nonelectrical machinery

electrical machinery

transportation equipment

miscellaneous manufactures

weighted correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

exports to Canada

1988–1999

model

-20.5

-4.1

-35.5

27.3

70.4

10.8

939.7

21.6

1847.0

19.2

1470.3

36.2

153.0

38.6

4387.6

15.0

4933.2

36.2

23.9

32.9

476.3

15.0

204.6

36.0

-10.6

32.9

2366.2

-6.7

1396.1

5.7

676.8

13.3

32.5

19.4

-35.4

138.1

610.4

41.9

570.6

17.3

1349.2

137.3

2303.4

3.3

379.4

61.1

exports to United States

1988–1999

model

-15.0

2.5

-22.9

26.9

9.4

7.5

832.3

11.8

829.6

18.6

618.3

11.7

111.1

4.6

145.6

-2.7

181.2

7.6

70.3

13.9

122.1

3.9

70.4

17.0

66.4

34.1

783.8

-5.3

222.3

3.7

469.8

32.3

40.9

30.8

111.2

156.5

477.2

26.8

123.6

18.5

744.9

178.0

349.0

6.2

181.5

43.2

0.19

0.01

0.71

0.04

120.32

2.07

38.13

3.87

Changes in U.S. Exports/GDP in the Brown-Deardorff-Stern Model (Percent)

sector

agriculture

mining and quarrying

food

textiles

clothing

leather products

footwear

wood products

furniture and fixtures

paper products

printing and publishing

chemicals

petroleum and products

rubber products

nonmetal mineral products

glass products

iron and steel

nonferrous metals

metal products

nonelectrical machinery

electrical machinery

transportation equipment

miscellaneous manufactures

weighted correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

exports to Canada

1988–1999

model

-24.1

5.1

-23.6

1.0

62.4

12.7

177.2

44.0

145.5

56.7

29.9

7.9

48.8

45.7

76.4

6.7

83.8

35.6

-20.5

18.9

50.8

3.9

49.8

21.8

-6.9

0.8

95.6

19.1

56.5

11.9

50.5

4.4

0.6

11.6

-20.7

-6.7

66.7

18.2

36.2

9.9

154.4

14.9

36.5

-4.6

117.3

11.5

exports to Mexico

1988–1999

model

6.5

7.9

-19.8

0.5

37.7

13.0

850.5

18.6

543.0

50.3

87.7

15.5

33.1

35.4

25.7

7.0

224.1

18.6

-41.9

-3.9

507.9

-1.1

61.5

-8.4

-41.1

-7.4

165.6

12.8

55.9

0.8

112.9

42.3

144.5

-2.8

-28.7

-55.1

301.4

5.4

350.8

-2.9

167.8

-10.9

290.3

9.9

362.3

-9.4

-0.01

0.14

37.27

-0.02

0.50

0.02

190.89

3.42

Changes in Canadian Trade/GDP

in Cox-Harris Model (Percent)

variable

total trade

trade with Mexico

trade with United States

data

1988-2000

57.2

280.0

76.2

weighted correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

model

10.0

52.2

20.0

0.99

0.52

38.40

1.93

Changes in Canadian Trade/GDP in the Cox-Harris Model (Percent)

sector

agriculture

forestry

fishing

mining

food, beverages, and tobacco

rubber and plastics

textiles and leather

wood and paper

steel and metal products

transportation equipment

machinery and appliances

nonmetallic minerals

refineries

chemicals and misc. manufactures

total exports

1988-2000

model

-13.7

-4.1

215.5

-11.5

81.5

-5.4

21.7

-7.0

50.9

18.6

194.4

24.5

201.1

108.8

31.9

7.3

30.2

19.5

66.3

3.5

112.9

57.1

102.7

31.8

20.3

-2.7

53.3

28.1

total imports

1988-2000

model

4.6

7.2

-21.5

7.1

107.3

9.5

32.1

4.0

60.0

3.8

87.7

13.8

24.6

18.2

97.3

7.2

52.2

10.0

29.7

3.0

65.0

13.3

3.6

7.3

5.1

1.5

92.5

10.4

weighted correlation with data

variance decomposition of change

0.49

0.32

0.85

0.08

41.85

0.81

22.00

3.55

regression coefficient a

regression coefficient b

What Do We Learn from these Evaluations?

The Spanish model seems to have been far more successful in

predicting the consequences of policy changes than the three

models of NAFTA, but

x Kehoe, Polo, and Sancho (KPS) knew the structure of their

model well enough to precisely identify the relationships

between the variables in their model with those in the data;

x KPS were able to use the model to carry out numerical exercises

to incorporate the impact of exogenous shocks.

KPS had an incentive to show their model in the best possible

light.

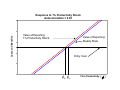

3. Much of the growth of trade after a trade liberalization

experience is growth on the extensive margin. Models need

to allow for corner solutions or fixed costs.

T. J. Kehoe and K. J. Ruhl, “How Important is the New Goods

Margin in International Trade?” Federal Reserve Bank of

Minneapolis, 2002.

K. J. Ruhl, “Solving the Elasticity Puzzle in International

Economics,” University of Texas at Austin, 2005.

What happens to the least-traded goods:

Over the business cycle?

During trade liberalization?

Indirect evidence on the extensive margin

4. Modeling the fixed costs may explain why real exchange rate

data indicate that more arbitrage across countries that have

a strong bilateral trade relationship.

C. M. Betts and T. J. Kehoe, “Real Exchange Rate Movements and

the Relative Price of Nontraded Goods,” University of Minnesota

and University of Southern California, 2003.

C. M. Betts and T. J. Kehoe, “U.S. Real Exchange Rate

Fluctuations and Relative Price Fluctuations,” University of

Minnesota and University of Southern California, 2003.

5. The major determinant of large macroeconomic fluctuations

in Mexico is fluctuations in total factor productivity. If

trade liberalization and the 1995 financial crisis have had

large macroeconomic effects, it is through their effects on

TFP.

R. Bergoeing, P. J. Kehoe, T. J. Kehoe, and R. Soto “A Decade

Lost and Found: Mexico and Chile in the 1980s,” Review of

Economic Dynamics, 5 (2002), 166-205.

T. J. Kehoe and E. C. Prescott, “Great Depressions of the

Twentieth Century,” Review of Economic Dynamics, 5 (2002), 118.

T. J. Kehoe and K. J. Ruhl, “Sudden Stops, Sectoral Reallocations,

and Productivity Drops,” University of Minnesota, 2006.

1. Standard theory (hybrid Heckscher-Ohlin/New Trade

Theory) does not well when matched with the data on the

growth and composition of trade.

In the 1980s and 1990s trade economists reached a consensus that

North-North trade — trade among rich countries — was driven by

forces captured by the New Trade Theory and North-South trade

— trade between rich countries and poor countries — was driven

by forces captured by Heckscher-Ohlin theory. (South-South trade

was negligible.)

A. V. Deardorff, “Testing Trade Theories and Predicting Trade

Flows,” in R. W. Jones and P. B. Kenen, editors, Handbook of

International Economics, volume l, North-Holland, 1984, 467-517.

J. Markusen, “Explaining the Volume of Trade: An Eclectic

Approach,” American Economic Review, 76 (1986), 1002-1011.

In fact, a calibrated version of this hybrid model does not

match the data.

R. Bergoeing and T. J. Kehoe, “Trade Theory and Trade Facts,”

Federal Reserve Bank of Minneapolis, 2003.

TRADE THEORY

Traditional trade theory — Ricardo, Heckscher-Ohlin — says

countries trade because they are different.

In 1990 by far the largest bilateral trade relation in the world was

U.S.-Canada. The largest two-digit SITC export of the United

States to Canada was 78 Road Vehicles. The largest two-digit

SITC export of Canada to the United States was 78 Road Vehicles.

The New Trade Theory — increasing returns, taste for variety,

monopolistic competition — explains how similar countries can

engage in a lot of intraindustry trade.

Helpman and Krugman (1985)

Markusen (1986)

TRADE THEORY AND TRADE FACTS

x Some recent trade facts

x A “New Trade Theory” model

x Accounting for the facts

x Intermediate goods?

x Policy?

How important is the quantitative failure of the New

Trade Theory?

Where should trade theory and applications go from

here?

SOME RECENT TRADE FACTS

x The ratio of trade to product has increased.

World trade/world GDP increased by 59.3 percent 1961-1990.

OECD-OECD trade/OECD GDP increased by 111.5 percent

1961-1990.

x Trade has become more concentrated among industrialized

countries

OECD-OECD trade/OECD-RW trade increased by 87.1 percent

1961-1990.

x Trade among industrialized countries is mostly intraindustry

trade

Grubel-Lloyd index for OECD-OECD trade in 1990 is 68.4.

Grubel-Lloyd index for OECD-RW trade in 1990 is 38.1.

OECD-OECD Trade / OECD GDP

0.12

0.10

0.08

0.06

0.04

0.02

0.00

1960

1963

1966

1969

1972

1975

year

1978

1981

1984

1987

1990

OECD-OECD Trade / OECD-RW Trade

1.80

1.60

1.40

1.20

1.00

0.80

0.60

0.40

0.20

0.00

1960

1963

1966

1969

1972

1975

year

1978

1981

1984

1987

1990

Helpman and Krugman (1985):

“These....empirical weaknesses of conventional trade

theory...become understandable once economies of scale and

imperfect competition are introduced into our analysis.”

Markusen, Melvin, Kaempfer, and Maskus (1995):

“Thus, nonhomogeneous demand leads to a decrease in NorthSouth trade and to an increase in intraindustry trade among the

northern industrialized countries. These are the stylized facts that

were to be explained.”

Goal: To measure how much of the increase in the ratio of

trade to output in the OECD and of the concentration of world

trade among OECD countries can be accounted for by the

“New Trade Theory.”

PUNCHLINE

In a calibrated general equilibrium model,

the New Trade Theory cannot account for the

increase in the ratio of trade to output in the

OECD.

Back-of-the-envelope calculations:

Suppose that the world consists of the OECD and the only trade is

manufactures.

With Dixit-Stiglitz preferences, country j exports all of its

production of manufactures Ymj except for the fraction s j Y j / Y oe

that it retains for domestic consumption.

World imports:

M

World trade/GDP:

M

Y oe

World trade/GDP:

n

¦j

M Ymoe

Ymoe Y oe

j

j

1

s

Y

m.

1

1 ¦

n

j

oe

Y

j 2

m

s

(

)

.

oe

1

Y

M

Y oe

n

M Ymoe

Ymoe Y oe

1 ¦

n

j

oe

Y

j 2

m

s

(

)

.

oe

1

Y

1 ¦ j 1 ( s j ) 2 goes from 0.663 in 1961 to 0.827 in 1990.

Ymoe / Y oe goes from 0.295 in 1961 to 0.222 in 1990.

0.663 u 0.295 0.196 | 0.184 0.827 u 0.222 .

Effects cancel!

A “NEW TRADE THEORY” MODEL

Environment:

x Static: endowments of factors are exogenous

x 2 regions: OECD and rest of world

x 2 traded goods: homogeneous — primaries (CRS) and

differentiated — manufactures (IRS)

x 1 nontraded good — services (CRS)

x 2 factors: (effective) labor and capital

x Identical technologies and preferences (love for variety) across

regions

x Primaries are inferior to manufactures

We only consider merchandise trade in both the data and in

the model.

Key Features of the Model

Consumers' problem:

max

s.t.

E p (c pj J p )K E m ( ³ cmj ( z ) U dz p )K / U E s (csj J s )K 1

Dw

K

q p c pj ³ w qm ( z )cmj ( z )dz p qsj csj d r j k j w j h j .

D

Firms' problems

Primaries and Services: Standard CRS problems.

Ypj

T p ( K pj )D p ( H pj )1D p

Ys j

Ts ( K sj )D s ( H sj )1D s

Manufactures: Standard (Dixit-Stiglitz) monopolistically

competitive problem:

x Fixed cost.

Ym ( z )

max ª¬Tm K m ( z )Dm H m ( z )1Dm F ,0 º¼

x Firm z sets its price qm ( z ) to max profits given all of the

other prices.

n

Ym ( z ) ¦ j 1 Cmj ( z ) Cmrw ( z ) .

1

1K

Cmj ( z )

Em (r j K j w j H j q p J p N j qsj J s N j )

1

1U

U

1U

qm ( z ) ª ³ D w qm ( z c) dz cº

¬

¼

UK

U (1K )

(1U )

U

K

1K

'

U

K

1

ª

º

1U

1K 1K

'

Em « ³ w qm ( z c) dz c

» E s qs

D

¬

¼

x Every firm is uniquely associated with only one variety

(symmetry).

x Free entry.

[0, d w ] with d w finite and endogenously determined.

x Dw

K

1K

E p qp

1

1K

1

1K

Volume of Trade

Let s j be the share of country j , j

production of manufactures,

sj

³D

j

1,..., n, rw , in the world

Ym ( z )dz / ³D w Ym ( z )dz

Ymj / Ymw .

The imports by country j from the OECD are

M oej (1 s rw s j )Cmj

M oerw (1 s rw )Cmrw .

Total imports in the OECD from the other OECD countries are

n

M

oe

oe

n

j 2

rw

oe

M

(1

s

(

s

)

/(1

s

))

C

¦

¦

m .

j

oe

j 1

rw

j 1

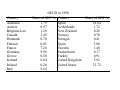

OECD in 1990

Country

Australia

Austria

Belgium-Lux

Canada

Denmark

Finland

France

Germany

Greece

Iceland

Ireland

Italy

Share of GDP %

1.79

0.97

1.26

3.45

0.78

0.81

7.26

9.96

0.50

0.04

0.28

6.64

Country

Japan

Netherlands

New Zealand

Norway

Portugal

Spain

Sweden

Switzerland

Turkey

United Kingdom

United States

Share of GDP %

18.04

1.72

0.26

0.70

0.41

3.00

1.40

0.17

0.91

5.92

33.72

ACCOUNTING FOR THE FACTS

Compare the changes that the model predicts for 1961-1990 with

what actually took place.

Focus on key variables:

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manfacturing GDP/OECD GDP

Calibrate to 1990 data.

Backcast to 1961 by imposing changes in parameters:

relative sizes of countries in the OECD

populations

sectoral productivities

endowments

ACCOUNTING FOR THE FACTS

Benchmark 1990 OECD Data Set

(Billion U.S. dollars)

H ioe

K ioe

Yi oe

Cioe

Yi oe Cioe

Primaries Manufactures

228

2,884

441

775

669

3,659

862

3,466

-193

193

Services

8,644

3,497

12,141

12,141

0

Total

11,756

4,713

16,469

16,469

0

ACCOUNTING FOR THE FACTS

Benchmark 1990 Rest of the World Data Set

(Billion U.S. dollars)

Yi rw

Cirw

Yi rw Cirw

Primaries Manufactures

1,223

1,159

1,030

1,352

193

-193

Services

3,447

3,447

0

Total

5,829

5,829

0

ACCOUNTING FOR THE FACTS

x N oe

x

¦

i

854 , N rw

rw

Y

p ,m , s i

x Set q p qm ( z )

values).

xU

4, 428 .

¦

i

rw

C

p ,m , s i

qs

w

5,829 .

r

1 (quantities are 1990

1/1.2 (Morrison 1990, Martins, Scarpetta, and Pilat 1996).

x Normalize d w

100 .

x Calibrate H rw , K rw so that benchmark data set is an

equilibrium.

x Alternative calibrations of utility parameters J p , J s , and K .

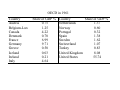

OECD in 1961

Country

Austria

Belgium-Lux

Canada

Denmark

France

Germany

Greece

Iceland

Ireland

Italy

Share of GDP %

0.75

1.25

4.22

0.70

6.99

9.71

0.50

0.03

0.21

4.64

Country

Share of GDP %

Netherlands

1.37

Norway

0.60

Portugal

0.32

Spain

1.38

Sweden

1.62

Switzerland

1.07

Turkey

0.83

United Kingdom

8.08

United States

55.74

Numerical Experiments

Calculate equilibrium in 1961:

T p ,1961

T m ,1961

T s ,1961

N oe

T p ,1990

T m ,1990 /1.01429 , F1961

F1990 /1.01429

T s ,1990 /1.00529 (Echevarria 1997)

536, N rw

2,545

Numerical Experiments

oe

oe

rw

rw

Choose H1961

, K1961

, H1961

, K1961

so that

¦

¦

¦

¦

i

oe

oe

Y

/

N

1990

p ,m , s i ,1990

oe

i p ,m , s i ,1961

Y

i

oe

1961

/N

rw

rw

Y

/

N

1990

p ,m , s i ,1990

rw

i p ,m , s i ,1961

Y

rw

1961

/N

oe

oe

K1961

K1990

oe

oe

H1961

H1990

q p ,1961 (Yprw,1961 C prw,1961 )

¦

i p ,m , s

rw

i ,1961 i ,1961

q

Y

2.400

2.055

0.050

How Can the Model Work in Matching the Facts?

x The ratio of trade to product has increased:

The size distribution of countries has become more equal

(Helpman-Krugman).

x Trade has become more concentrated among industrialized

countries:

OECD countries have comparative advantage in manufactures,

while the RW has comparative advantage in primaries.

Because they are inferior to manufactures, primaries become

less important in trade as the world becomes richer

(Markusen).

How Can the Model Work in Matching the Facts?

x Trade among industrialized countries is largely intraindustry

trade:

OECD countries export manufactures. Because of taste for

variety, every country consumes some manufactures from

every other country (Dixit-Stiglitz).

x The different total factor productivity growth rates across

sectors imply that the price of manufactures relative to

primaries and services has fallen sharply between 1961 and

1990. If price elasticities of demand are not equal to one, a lot

can happen.

Experiment 1

Jp

Jp K

0

Data

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

1. Jp = 0, Js = 0, K = 0

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

1961

1990

Change

0.053

0.844

0.295

0.112

1.579

0.222

111.5%

87.1%

24.6%

0.108

0.893

0.223

0.136

1.169

0.222

25.8%

30.9%

0.4%

Experiment 2

Jp = 169.5, Js = 314.7 to match consumption in RW in 1990,

K=0

1961

Data

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

2. Jp = 169.5, Js = 314.7, K = 0

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

1990

Change

0.053

0.844

0.295

0.112 111.5%

1.579 87.1%

0.222 24.6%

0.103

0.739

0.225

0.132

1.060

0.222

28.1%

43.6%

1.4%

Experiment 3

Jp = 169.5, Js = 314.7,

K = 0.559 to match growth in OECD-OECD Trade/OECD GDP

1961

Data

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

3. Jp = 169.5, Js = 314.7, K = 0.559

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

1990

Change

0.053

0.844

0.295

0.112 111.5%

1.579 87.1%

0.222 24.6%

0.063

0.738

0.137

0.132 111.5%

1.060 43.7 %

0.222 62.7%

Experiments 4 and 5

Jp = 169.5, Js = 314.7, reasonable values of K ( 0.5 t 1/(1 K ) t 0.1)

1961

1990

Change

Data

OECD-OECD Trade/OECD GDP

0.053

0.112

111.5%

OECD-OECD Trade/OECD-RW Trade

0.844

1.579

87.1%

OECD Manf GDP/OECD GDP

0.295

0.222

24.6%

4. Jp = 169.5, Js = 314.7, K = 1

OECD-OECD Trade/OECD GDP

0.118

0.132

11.7%

OECD-OECD Trade/OECD-RW Trade

0.739

1.060

43.5%

OECD Manf GDP/OECD GDP

0.259

0.222

14.1%

5. Jp = 169.5, Js = 314.7, K = 9

OECD-OECD Trade/OECD GDP

0.118

0.132

1.6%

OECD-OECD Trade/OECD-RW Trade

0.739

1.060

43.5%

OECD Manf GDP/OECD GDP

0.284

0.222

21.8%

Sensitivity Analysis:

Alternative Calibration Methodologies

x Alternative specifications of nonhomogeneity

x Gross imports calibration

x Alternative RW endowment calibration

x Alternative RW growth calibration

x Intermediate goods

INTERMEDIATE GOODS?

Ypj

j

j

ª X j ³ w X mp

º

(

z

)

dz

X

D

1

D

p

p

pp

sp

»

min «

, D

,

, T p K pj H pj amp

asp

«¬ a pp

»¼

Ym ( z )

Ys j

j

ª X j ( z ) ³ w X mm

( z , z ')dz ' X j ( z ) º

pm

«

, D

, sm , »

amm

asm »

min « a pm

«

»

Dm

1D m

F

«¬Tm K m ( z ) H m ( z ) »¼

j

ª X j ³ w X ms

º

j

(

z

)

dz

D

1

D

X

s

s

ps

min «

, D

, ss , Ts K sj H sj »

ams

ass

«¬ a ps

»¼

Results for Model with Intermediate Goods

1961

Data

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

4. Jp = 307.8, Js = 262.2, K = 1

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

5. Jp = 307.8, Js = 262.2, K = 9

OECD-OECD Trade/OECD GDP

OECD-OECD Trade/OECD-RW Trade

OECD Manf GDP/OECD GDP

1990

Change

0.053 0.112

0.844 1.579

0.295 0.222

111.5%

87.1%

24.6%

0.323 0.370

0.994 1.305

0.263 0.222

14.5%

31.3%

15.6%

0.337 0.370

0.933 1.305

0.307 0.222

9.7%

39.9%

27.5%

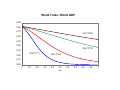

POLICY?

In a version of our model with n OECD countries, a manufacturing

sector, and a uniform ad valorem tariff W, the ratio of exports to

income is given by

M

Y

(n 1)C f

Y

n 1

n 1 (1 W )1/(1 U )

Fixing n to replicate the size distribution of national incomes in the

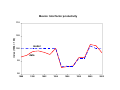

OECD, and setting U 1/1.2 , a fall in W from 0.45 to 0.05 produces

an increase in the ratio of trade to output as seen in the data.

World Trade / World GDP

0.90

0.80

0.70

rho=1/2.0

0.60

0.50

0.40

rho=1/1.5

0.30

rho=1/1.1

0.20

rho=1/1.2

0.10

0.00

0

0.1

0.2

0.3

0.4

0.5

tau

0.6

0.7

0.8

0.9

1

2. Applied general equilibrium models that put the standard

theory to work do not well in predicting the impact of trade

liberalization experiences like NAFTA.

Applied general equilibrium models were the only analytical game in

town when it came to analyzing the impact of NAFTA in 1992-1993.

Typical sort of model: Static applied general equilibrium model with

large number of industries and imperfect competition (Dixit-Stiglitz or

Eastman-Stykolt) and finite number of firms in some industries. In some

numerical experiments, new capital is placed in Mexico owned by

consumers in the rest of North America to account for capital flows.

Examples:

Brown-Deardorff-Stern model of Canada, Mexico, and the United States

Cox-Harris model of Canada

Sobarzo model of Mexico

T. J. Kehoe, “An Evaluation of the Performance of Applied

General Equilibrium Models of the Impact of NAFTA,” in T. J.

Kehoe, T. N. Srinivasan, and J. Whalley, editors, Frontiers in

Applied General Equilibrium Modeling: Essays in Honor of

Herbert Scarf, Cambridge University Press, 2005, 341-77.

Research Agenda:

x Compare results of numerical experiments of models with data.

x Determine what shocks — besides NAFTA policies — were

important.

x Construct a simple applied general equilibrium model and

perform experiments with alternative specifications to determine

what was wrong with the 1992-1993 models.

Applied GE Models Can Do a Good Job!

Spain: Kehoe-Polo-Sancho (1992) evaluation of the performance

of the Kehoe-Manresa-Noyola-Polo-Sancho-Serra MEGA model

of the Spanish economy: A Shoven-Whalley type model with

perfect competition, modified to allow government and trade

deficits and unemployment (Kehoe-Serra). Spain’s entry into the

European Community in 1986 was accompanied by a fiscal reform

that introduced a value-added tax (VAT) on consumption to

replace a complex range of indirect taxes, including a turnover tax

applied at every stage of the production process. What would

happen to tax revenues? Trade reform was of secondary

importance.

Canada-U.S.: Fox (1999) evaluation of the performance of the

Brown-Stern (1989) model of the 1989 Canada-U.S. FTA.

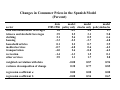

Other changes besides policy changes are important!

Changes in Consumer Prices in the Spanish Model

(Percent)

sector

food and nonalcoholic beverages

tobacco and alcoholic beverages

clothing

housing

household articles

medical services

transportation

recreation

other services

data

model

model

model

1985-1986 policy only shocks only policy&shocks

1.8

-2.3

4.0

1.7

3.9

2.5

3.1

5.8

2.1

5.6

0.9

6.6

-3.3

-2.2

-2.7

-4.8

0.1

2.2

0.7

2.9

-0.7

-4.8

0.6

-4.2

-4.0

2.6

-8.8

-6.2

-1.4

-1.3

1.5

0.1

2.9

1.1

1.7

2.8

weighted correlation with data

variance decomposition of change

-0.08

0.30

0.87

0.77

0.94

0.85

regression coefficient a

regression coefficient b

0.00

-0.08

0.00

0.54

0.00

0.67

Measures of Accuracy of Model Results

1. Weighted correlation coefficient.

2. Variance decomposition of the (weighted) variance of the

changes in the data:

vardec( y data , y model )

var ( y model )

.

model

data

model

var ( y

) var ( y y

)

3, 4. Estimated coefficients a and b from the (weighted)

regression

xidata

a bximodel ei .

Changes in Value of Gross Output/GDP in the Spanish Model (Percent)

sector

agriculture

energy

basic industry

machinery

automobile industry

food products

other manufacturing

construction

commerce

transportation

services

government services

data

1985-1986

-0.4

-20.3

-9.0

3.7

1.1

-1.8

0.5

5.7

6.6

-18.4

8.7

7.6

weighted correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

model

policy only

-1.1

-3.5

1.6

3.8

3.9

-2.4

-1.7

8.5

-3.6

-1.5

-1.1

3.4

model

model

shocks only policy&shocks

8.3

6.9

-29.4

-32.0

-1.8

-0.1

1.0

5.0

4.7

8.6

4.7

2.1

2.3

0.5

1.4

10.3

4.4

0.4

1.0

-0.7

5.8

4.5

0.9

4.3

0.16

0.11

0.80

0.73

0.77

0.71

-0.52

0.44

-0.52

0.75

-0.52

0.67

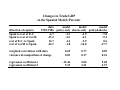

Changes in Trade/GDP

in the Spanish Model (Percent)

direction of exports

Spain to rest of E.C.

Spain to rest of world

rest of E.C. to Spain

rest of world to Spain

data

model

model

model

1985-1986 policy only shocks only policy&shocks

-6.7

-3.2

-4.9

-7.8

-33.2

-3.6

-6.1

-9.3

14.7

4.4

-3.9

0.6

-34.1

-1.8

-16.8

-17.7

weighted correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

0.69

0.02

0.77

0.17

0.90

0.24

-12.46

5.33

2.06

2.21

5.68

2.37

Changes in Composition of GDP in the Spanish Model (Percent of GDP)

variable

wages and salaries

business income

net indirect taxes and tariffs

data

model

1985-1986 policy only

-0.53

-0.87

-1.27

-1.63

1.80

2.50

model

shocks only

-0.02

0.45

-0.42

model

policy&shocks

-0.91

-1.24

2.15

correlation with data

variance decomposition of change

0.998

0.93

-0.94

0.04

0.99

0.96

regression coefficient a

regression coefficient b

private consumption

private investment

government consumption

government investment

exports

-imports

0.00

0.73

-1.23

1.81

-0.06

-0.06

-0.42

-0.03

0.00

-3.45

-0.51

-0.58

-0.38

-0.07

-0.69

2.23

0.00

0.85

-1.78

1.32

-0.44

-0.13

-1.07

2.10

correlation with data

variance decomposition of change

0.40

0.20

0.77

0.35

0.83

0.58

regression coefficient a

regression coefficient b

0.00

0.87

0.00

1.49

0.00

1.24

-0.81

1.09

-0.02

-0.06

-3.40

3.20

Public Finances in the Spanish Model

(Percent of GDP)

data

model

model

model

variable

1985-1986 policy only shocks only policy&shocks

indirect taxes and subsidies

2.38

3.32

-0.38

2.98

tariffs

-0.58

-0.82

-0.04

-0.83

social security payments

0.04

-0.19

-0.03

-0.22

direct taxes and transfers

-0.84

-0.66

0.93

0.26

government capital income

-0.13

-0.06

0.02

-0.04

correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

0.99

0.93

-0.70

0.08

0.92

0.86

-0.06

0.74

0.35

-1.82

-0.17

0.80

Models of NAFTA

Did Not Do a Good Job!

Ex-post evaluations of the performance of applied GE models are

essential if policy makers are to have confidence in the results

produced by this sort of model.

Just as importantly, they help make applied GE analysis a

scientific discipline in which there are well-defined puzzles and

clear successes and failures for alternative hypotheses.

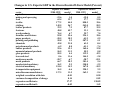

Changes in Trade/GDP

in Brown-Deardorff-Stern Model (Percent)

variable

Canadian exports

Canadian imports

Mexican exports

Mexican imports

U.S. exports

U.S. imports

data

1988-1999

52.9

57.7

240.6

50.5

19.1

29.9

weighted correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

model

4.3

4.2

50.8

34.0

2.9

2.3

0.64

0.08

23.20

2.43

Changes in Canadian Exports/ GDP in the Brown-Deardorff-Stern Model (Percent)

sector

agriculture

mining and quarrying

food

textiles

clothing

leather products

footwear

wood products

furniture and fixtures

paper products

printing and publishing

chemicals

petroleum and products

rubber products

nonmetal mineral products

glass products

iron and steel

nonferrous metals

metal products

nonelectrical machinery

electrical machinery

transportation equipment

miscellaneous manufactures

weighted correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

exports to Mexico

1988–1999

model

122.5

3.1

-34.0

-0.3

89.3

2.2

268.2

-0.9

1544.3

1.3

443.0

1.4

517.0

3.7

232.6

4.7

3801.7

2.7

240.7

-4.3

6187.4

-2.0

37.1

-7.8

678.1

-8.5

647.4

-1.0

333.5

-1.8

264.4

-2.2

195.2

-15.0

38.4

-64.7

767.0

-10.0

376.8

-8.9

633.9

-26.2

305.8

-4.4

1404.5

-12.1

exports to United States

1988–1999

model

106.1

3.4

75.8

0.4

91.7

8.9

97.8

15.3

237.1

45.3

-14.4

11.3

32.8

28.3

36.5

0.1

282.6

12.5

113.7

-1.8

37.2

-1.6

109.4

-3.1

-42.5

0.5

113.4

9.5

20.5

1.2

74.5

30.4

92.1

12.9

34.7

18.5

102.2

15.2

28.9

3.3

88.6

14.5

30.7

10.7

100.0

-2.1

-0.91

0.003

-0.43

0.02

249.24

-15.48

79.20

-2.80

Changes in Mexican Exports/GDP in the Brown-Deardorff-Stern Model (Percent)

sector

agriculture

mining and quarrying

food

textiles

clothing

leather products

footwear

wood products

furniture and fixtures

paper products

printing and publishing

chemicals

petroleum and products

rubber products

nonmetal mineral products

glass products

iron and steel

nonferrous metals

metal products

nonelectrical machinery

electrical machinery

transportation equipment

miscellaneous manufactures

weighted correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

exports to Canada

1988–1999

model

-20.5

-4.1

-35.5

27.3

70.4

10.8

939.7

21.6

1847.0

19.2

1470.3

36.2

153.0

38.6

4387.6

15.0

4933.2

36.2

23.9

32.9

476.3

15.0

204.6

36.0

-10.6

32.9

2366.2

-6.7

1396.1

5.7

676.8

13.3

32.5

19.4

-35.4

138.1

610.4

41.9

570.6

17.3

1349.2

137.3

2303.4

3.3

379.4

61.1

exports to United States

1988–1999

model

-15.0

2.5

-22.9

26.9

9.4

7.5

832.3

11.8

829.6

18.6

618.3

11.7

111.1

4.6

145.6

-2.7

181.2

7.6

70.3

13.9

122.1

3.9

70.4

17.0

66.4

34.1

783.8

-5.3

222.3

3.7

469.8

32.3

40.9

30.8

111.2

156.5

477.2

26.8

123.6

18.5

744.9

178.0

349.0

6.2

181.5

43.2

0.19

0.01

0.71

0.04

120.32

2.07

38.13

3.87

Changes in U.S. Exports/GDP in the Brown-Deardorff-Stern Model (Percent)

sector

agriculture

mining and quarrying

food

textiles

clothing

leather products

footwear

wood products

furniture and fixtures

paper products

printing and publishing

chemicals

petroleum and products

rubber products

nonmetal mineral products

glass products

iron and steel

nonferrous metals

metal products

nonelectrical machinery

electrical machinery

transportation equipment

miscellaneous manufactures

weighted correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

exports to Canada

1988–1999

model

-24.1

5.1

-23.6

1.0

62.4

12.7

177.2

44.0

145.5

56.7

29.9

7.9

48.8

45.7

76.4

6.7

83.8

35.6

-20.5

18.9

50.8

3.9

49.8

21.8

-6.9

0.8

95.6

19.1

56.5

11.9

50.5

4.4

0.6

11.6

-20.7

-6.7

66.7

18.2

36.2

9.9

154.4

14.9

36.5

-4.6

117.3

11.5

exports to Mexico

1988–1999

model

6.5

7.9

-19.8

0.5

37.7

13.0

850.5

18.6

543.0

50.3

87.7

15.5

33.1

35.4

25.7

7.0

224.1

18.6

-41.9

-3.9

507.9

-1.1

61.5

-8.4

-41.1

-7.4

165.6

12.8

55.9

0.8

112.9

42.3

144.5

-2.8

-28.7

-55.1

301.4

5.4

350.8

-2.9

167.8

-10.9

290.3

9.9

362.3

-9.4

-0.01

0.14

37.27

-0.02

0.50

0.02

190.89

3.42

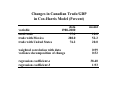

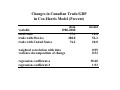

Changes in Canadian Trade/GDP

in Cox-Harris Model (Percent)

variable

total trade

trade with Mexico

trade with United States

data

1988-2000

57.2

280.0

76.2

weighted correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

model

10.0

52.2

20.0

0.99

0.52

38.40

1.93

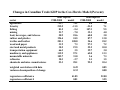

Changes in Canadian Trade/GDP in the Cox-Harris Model (Percent)

sector

agriculture

forestry

fishing

mining

food, beverages, and tobacco

rubber and plastics

textiles and leather

wood and paper

steel and metal products

transportation equipment

machinery and appliances

nonmetallic minerals

refineries

chemicals and misc. manufactures

total exports

1988-2000

model

-13.7

-4.1

215.5

-11.5

81.5

-5.4

21.7

-7.0

50.9

18.6

194.4

24.5

201.1

108.8

31.9

7.3

30.2

19.5

66.3

3.5

112.9

57.1

102.7

31.8

20.3

-2.7

53.3

28.1

total imports

1988-2000

model

4.6

7.2

-21.5

7.1

107.3

9.5

32.1

4.0

60.0

3.8

87.7

13.8

24.6

18.2

97.3

7.2

52.2

10.0

29.7

3.0

65.0

13.3

3.6

7.3

5.1

1.5

92.5

10.4

weighted correlation with data

variance decomposition of change

0.49

0.32

0.85

0.08

41.85

0.81

22.00

3.55

regression coefficient a

regression coefficient b

Changes in Mexican Trade/GDP in the Sobarzo Model (Percent)

sector

agriculture

mining

petroleum

food

beverages

tobacco

textiles

wearing apparel

leather

wood

paper

chemicals

rubber

nonmetallic mineral products

iron and steel

nonferrous metals

metal products

nonelectrical machinery

electrical machinery

transportation equipment

other manufactures

weighted correlation with data

variance decomposition of change

regression coefficient a

regression coefficient b

exports to North America

1988–2000

model

-15.3

-11.1

-23.2

-17.0

-37.6

-19.5

5.2

-6.9

42.0

5.2

-42.3

2.8

534.1

1.9

2097.3

30.0

264.3

12.4

415.1

-8.5

12.8

-7.9

41.9

-4.4

479.0

12.8

37.5

-6.2

35.9

-4.9

-40.3

-9.8

469.5

-4.4

521.7

-7.4

3189.1

1.0

224.5

-5.0

975.1

-4.5

0.61

0.0004

imports from North America

1988–2000

model

-28.2

3.4

-50.7

13.2

65.9

-6.8

11.8

-5.0

216.0

-1.8

3957.1

-11.6

833.2

-1.2

832.9

4.5

621.0

-0.4

168.9

11.7

68.1

-4.7

71.8

-2.7

792.0

-0.1

226.5

10.9

40.3

17.7

101.2

9.8

478.7

9.5

129.0

20.7

749.1

9.6

368.0

11.2

183.6

4.2

0.23

0.002

495.08

30.77

174.52

5.35

What Do We Learn from these Evaluations?

The Spanish model seems to have been far more successful in

predicting the consequences of policy changes than the three

models of NAFTA, but

x Kehoe, Polo, and Sancho (KPS) knew the structure of their

model well enough to precisely identify the relationships

between the variables in their model with those in the data;

x KPS were able to use the model to carry out numerical exercises

to incorporate the impact of exogenous shocks.

KPS had an incentive to show their model in the best possible

light.

3. Much of the growth of trade after a trade liberalization

experience is growth on the extensive margin. Models need

to allow for corner solutions or fixed costs.

T. J. Kehoe and K. J. Ruhl, “How Important is the New Goods

Margin in International Trade?” Federal Reserve Bank of

Minneapolis, 2002.

K. J. Ruhl, “Solving the Elasticity Puzzle in International

Economics,” University of Texas at Austin, 2005.

What happens to the least-traded goods:

Over the business cycle?

During trade liberalization?

Indirect evidence on the extensive margin

How Does Trade Grow?

ʀ Intensive Margin: growth in goods already traded

ʀ Extensive Margin: trade in goods not traded before

The Extensive Margin

ʀ The Extensive Margin has recently gained attention

ʀ Models

ɿ Melitz (2003)

ɿ Alessandria and Choi (2003)

ɿ Ruhl (2004)

ʀ Empirically

ɿ Hummels and Klenow (2002)

ɿ Eaton, Kortum and Kramarz (2004)

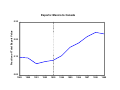

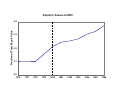

What Happens to the Extensive Margin?

ʀ During trade liberalization?

ɿ Large changes in the extensive margin

ʀ Over the business cycle?

ɿ Little change in extensive margin

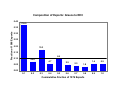

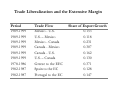

Evidence from Trade Agreements

ʀ Events

ɿ Greece’s Accession to the European Econ. Community - 1981