Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

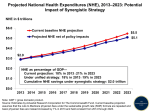

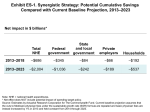

Confronting Costs: Stabilizing U.S. Health Spending While Moving Toward a High Performance System Overview and Key Findings of a New Report from The Commonwealth Fund Commission on a High Performance Health System Cathy Schoen, Senior Vice President and Stuart Guterman, Vice President and Executive Director of the Commission The Commonwealth Fund Release Charts - January 9, 2013 2 Confronting Costs - Whole System Approach • Rising health costs putting pressure on businesses and families as well as federal and state budgets - AND the economy – Spending projected to reach 21% of GDP by 2023 – up from 18% – Private health spending rising faster than Medicare per person – Premiums on a path to equal 31% of median income by 2023 – Similar market forces contributing to high and rising costs • Broad evidence we can do better if we focus on value – Evidence of waste, poorly coordinated/unsafe care, excess prices, high administrative costs – Slow spread of innovative systems – Growing concentration of market power among providers – need for more consistent payment approaches across payers • Comprehensive strategy: better health, better care at lower costs – Accelerate care system innovation and improve the way health care markets function • ARC modeled potential impact 2013 to 2023 3 Synergistic Policies to Stabilize Costs • Set target to hold total health spending growth to GDP growth, while moving toward high performance system • Three pillars - synergistic policies – Provider payment reforms to promote value and accelerate health care delivery system innovation – Policies to expand and encourage high-value choices by consumers, armed with better information on quality and costs – Systemwide action to improve how markets function, including lower administrative costs and set targets for spending growth • Potential to save a cumulative $2 trillion NHE over 10 years – $1.04 trillion in federal savings; avoid physician fee cuts – Substantial savings for families, businesses, state governments – Policies interact to align provider and consumer incentives, across public and private payers • Critical to start soon and together – savings accumulate 4 Potential Cumulative Savings by Payer Compared to Current Baseline Projection, 2013-2023 Net impact in $ billions* Total NHE Federal govt. State and Private Households local govt. employers -$686 –$345 –$84 –$66 –$192 2013-2023 -$2,004 –$1,036 –$242 –$189 –$537 2013-2018 Note: NHE = National Health Expenditures. *Net effect does NOT include potential impact of spending target policy. Source: Estimates by Actuarial Research Corporation for The Commonwealth Fund. Current baseline projection assumes that the cuts to Medicare physician fees under the sustainable growth rate (SGR) formula are repealed and basic physician fees are instead increased by 1% in 2013 and held constant from 2014 through 2023. 5 Synergistic Strategy: Cumulative Savings 2013-2023 Payment Reforms to Accelerate Delivery System Innovation • • • • ($1,333 B) Pay for value: replace the SGR with provider payment incentives to improve care Strengthen patient-centered primary care and support care teams Bundle hospital payments to focus on total cost and outcomes Align payment incentives across public and private payers Policies to Expand Options and Encourage High-Value Choices ($189 B) • Offer new Medicare Essential plan with integrated benefits through Medicare, offering positive incentives for use of high-value care and care systems • Provide positive incentives to seek care from patient-centered medical homes, care teams, and accountable care networks (Medicare, Medicaid, private plans) • Enhance clinical information to inform choice Other Systemwide Actions to Improve How Health Markets Function ($481 B) • Simplify and unify administrative policies and procedures • Reform malpractice policy and link to payment* • Target total public and private payment (combined) to grow at rate no greater than GDP per capita** * Malpractice policy savings included with provider payment policies. **Target policy was not scored. 6 Projected National Health Expenditures (NHE), 2013-2023: Potential Impact of Synergistic Strategy NHE in trillions $6.0 Current Baseline NHE projection $5.5 Projected NHE net of policy impacts $5.0 $5.1 $4.0 $2.9 $3.0 $2.0 $1.0 NHE as percent of GDP— Current projection: 18% in 2013→21% in 2023 Under unified strategy: 18% in 2013→19% in 2023 Cumulative NHE savings under synergistic strategy: $2.0 trillion $0.0 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 Note: NHE = National Health Expenditures; GDP = Gross Domestic Product. Source: Estimates by Actuarial Research Corporation for The Commonwealth Fund. Current baseline projection assumes that the cuts to Medicare physician fees under the sustainable growth rate (SGR) formula are repealed and basic physician fees are instead increased by 1% in 2013 and held constant from 2014 through 2023. Provider Revenues Continue to Grow: Impact on Projected Annual Spending for Hospital and Physician, 2013-2023 Spending in billions $1,800 Hospital (Baseline) $1,600 Hospital (Net of Policy Impacts) $1,646 Physician (Baseline) $1,400 $1,509 Physician (Net of Policy Impacts) $1,200 $1,000 $1,122 $902 $1,055 $800 $597 $600 Projected growth of hospital spending, 2013-2023: --Baseline projection: 82% (6.2% annual) --Net of policy impact: 67% (5.3% annual) Projected growth of physician spending, 2013-2023: --Baseline projection: 88% (6.5% annual) --Net of policy impact: 77% (5.9% annual) $400 $200 $0 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 Data: Estimates by Actuarial Research Corporation for The Commonwealth Fund. Current baseline projection assumes that the cuts to Medicare physician fees under the sustainable growth rate (SGR) formula are repealed and basic physician fees are instead increased by 1% in 2013 and held constant from 2014 through 2023. 7 8 Confronting Costs While Improving Performance • Comprehensive, market-wide approach needed with focus on value, care system innovation • Confronting cost growth requires – Accelerating spread of patient-centered, coordinated care systems, on foundation of primary care and teams – Intensified multi-payer efforts to hold care systems accountable – Information systems to compare, learn, and spur action • Substantial federal savings could offset cost of repealing scheduled cuts in physician fees (SGR) • High stakes for the economy – not just federal budget – Rising health spending saps resources that could be invested wages, jobs, schools, roads, science/technology • Key to act soon and together – Public and private payers acting in concert 9 Thank You! David Blumenthal, M.D. President Chair, Commission on a High Performance Health System [email protected] Stuart Guterman Vice President Executive Director, Commission on a High Performance Health System [email protected] Mark Zezza Senior Program Officer, Payment and System Reform [email protected] The Commonwealth Fund Commission on a High Performance Health System Melinda Abrams Vice President, Patient-Centered Coordinated Care [email protected] Actuarial Research Corporation staff, under the direction of Jim Mays, developed the estimates for this report. For more information, please visit: www.commonwealthfund.org 10 Background Additional Report Exhibits • Chart 11: High Performance Health System Framework and Criteria to Guide Policies to Stabilize Spending Growth • Chart 12: International Health Spending Comparison, 1980-2010 • Chart 13: Projected Total Spending by Major Payer • Chart 14: Projected Rates of Increase Medicare Cost Per Person Compared to Private Insurance and GDP • Chart 15: Private Premium Increases Compared to Wages and Incomes, Actual and Projected to 2021 11 Framework: High Performance Health System Criteria to Stabilize Spending Growth • Set targets for total spending growth • Pay for value to accelerate delivery system reform for better outcomes, better care, at lower costs • Address the system-wide causes of health spending growth – not just federal health costs • Align incentives for providers and consumers across public and private payers • Protect access and enhance equity, but also engage and inform consumers • Invest in information systems to guide action 12 International Spending on Health, 1980–2010 Average spending on health per capita ($US PPP) Total health expenditures as percent of GDP 18 $8,000 US $7,000 16 SWIZ NETH $6,000 14 CAN 12 GER FR 10 AUS UK 8 JPN US NETH FR GER CAN SWIZ UK JPN AUS Note: PPP = Purchasing power parity. Source: Commonwealth Fund analysis, based on OECD Health Data 2012. 2004 2002 2000 1998 1996 1994 1992 1990 1988 1986 1984 1982 2010 2008 2006 2004 2002 2000 1998 1996 1994 1992 1990 0 1988 $0 1986 2 1984 $1,000 1982 4 1980 $2,000 1980 6 2010 $3,000 2008 $4,000 2006 $5,000 Projected U.S National Health Expenditures (NHE) by Source, 2013-2023 $ Billions NHE 13 $5.5 Trillion 32% Federal Government 18% State & Local Government 5000 $4.0 Trillion 4000 $2.9 Trillion 31% 3000 28% 2000 18% 24% 18% 25% 1000 26% 26% 28% 26% 2013 2018 2023 18% 19% 21% Private Employers (including "other private revenue") Households 0 %GDP: Source: Estimates by Actuarial Research Corporation for The Commonwealth Fund. 14 Medicare Spending Per Enrollee Projected to Increase Slower than Private Insurance Spending Per Enrollee and GDP Per Capita Annual rate of growth, in percent 8.0 GDP per capita 7.0 Medicare spending per enrollee 6.0 Employer-sponsored insurance spending per enrollee 5.0 3.7 4.0 3.0 4.6 4.5 3.8 2.9 2.7 2.0 1.0 0.0 2008–2011 2011–2021 (projected) Note: GDP = Gross Domestic Product. Source: CMS Office of the Actuary, National Health Expenditure Projections, 2011–2021, updated June 2012. 15 Premiums Rising Faster Than Inflation and Wages Cumulative Changes in Insurance Premiums and Workers’ Earnings, 1999–2012 Projected Average Family Premium as a Percentage of Median Family Income, 2013–2021 Percent Percent Health Insurance Premiums 200% 180% Workers' Contribution to Premiums 180% Workers' Earnings 160% 172% Overall Inflation 140% 35 30 25 120% 22 23 20 100% 15 12 13 80% 60% 47% 10 38% 5 15 17 18 18 18 18 19 24 25 26 26 27 28 29 30 31 20 20% 0% 2012 2011 2010 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 0 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 40% Projected Data: Kaiser Family Foundation/Health Research and Educational Trust, Employer Health Benefits Annual Surveys, 1999–2012. Data: Fund authors’ estimates based on CPS ASEC 2001–12, Kaiser/HRET 2001–12, CMS OACT 2012–21. Source: Commonwealth Fund Commission, Confronting Costs, January 2013