Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

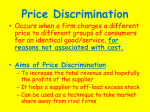

PRICE STRATEGY AND MONOPOLISTIC COMPETITION Afonso Sebastião Feliciano Grosso Joana Fernandes Ricardo Costa Susana Serôdio Lisbon, February 2006 PRICE STRATEGY THE IMPORTANCE OF PRICE Price means one thing to the consumer and something else to the seller. CONSUMER The cost of something SELLER Price is revenue, the primary source of profits WHAT IS PRICE? • Price is that which is given up in an exchange to acquire a good or service. • Price is typically the money exchanged for the good or service. • Prices are the key to revenues, which in turn are the key to profits for an organization. PRICE STRATEGY REVENUE Revenue is the price charged to customers multiplied by the number of units sold. It’s what pays for every activity of the company: production, finance, sales, distribution, and so on. PROFIT What’s left over is profit. Managers usually strive to charge a price that will earn a fair profit. To earn profit, a managers must choose a price that is not too high or too low, a price that equals the perceived value to customers. If a price is set to high in consumers’ minds, the perceived value will be less than the cost, and sales opportunity will be lost. PRICING OBJECTIVES To survive in today’s highly competitive marketplace, companies need pricing objectives that are specific, attainable, and measurable. Realistic pricing goals then require periodic monitoring to determine the effectiveness of company’s strategy. LONG-TERM PRICING Long-term pricing framework for a good or service should be a logical extension of the pricing objectives. It is necessary to choose a price strategy that defines the initial price and gives direction for price movements over the lifecycle. Lifecycle of the product: • Introductory stage – management usually sets prices high during the introductory stage. But, if the target market is highly sensitive, management often finds it better to price the product at the market level or lower. • Growth stage – Prices generally begin to stabilize as the product enters the growth stage. • Maturity stage – Maturity usually brings further price decreases as competition increases and inefficient, high-cost firms are eliminated. • Decline stage – The final stage of the lifecycle may see further price decreases as the few remaining competitors try to salvage the last vestiges of demand LONG-TERM PRICING Price Skimming Selling at a high price, sacrificing high sales to gain a high profit, therefore “skimming” the market. This strategy is often used to target “early adopters” of a product/service. These early adopters are relatively less price sensitive because either their need for the product is more than others or they understand the value of the product better than others. This strategy is employed only for limited duration to recover most of the investment made to build the product. LONG-TERM PRICING Price Skimming Diário de Notícias, 26 de Junho de 2005 LONG-TERM PRICING Penetration price Is the pricing technique of setting a relatively low initial entry price, a price that is often lower than the eventual market price. The expectation is that the initial low price will secure market acceptance by breaking down existing brand loyalties. The advantages of penetration pricing to the firm: • It can result in fast diffusion and adoption; • It can create goodwill among the all-important early adopter segment; • It creates cost control and cost reduction pressures from the start, leading to greater efficiency; • It discourages the entry of competitors; • It can be based on marginal cost pricing; LONG-TERM PRICING Penetration price The main disadvantages with penetration pricing is that: • It establishes long term price expectations for the product; • Image preconceptions for the brand and company; • It’s difficult to eventually raise prices. Penetration pricing attracts only the switchers (bargain hunters) It is most appropriate when: • Product demand is highly price elastic; • Substantial economics of scale area available; • The product is suitable for a mass market – sufficient demand; • The product will face stiff competition soon after introduction. LONG-TERM PRICING Penetration price This strategy is particularly adequate to introduction of products of regular buying, because the difference between them and the existent products is not obvious. For example, in the 80’s CP announced the intercity service. As a promotion, the second class tickets suffered a substantial discount relatively to the usual price. This way CP could attract potential clients that didn't use the train regularly. NON-LINEAR PRICES (NLP) With a fixed price structure the company leaves a potential surplus of the market to appropriate Distinct prices to different clients We will now study other ways of appropriating the surplus, from more complex price structures NLP - QUANTITY DISCOUNT Companies P=f(Q) throw offers of quantity discount One of the reason is the existence of scale economies on processing the goods Discount for segment the demand Another reason of quantities discounts passes throw the possibility of discriminating prices between different groups If the company identifies which consumers belong to which group, they can establish different prices NLP - QUANTITY DISCOUNT Discount for segment the demand Sometimes the companies can make their clients reveal to which group they belong P1 P D1 P1 P2 (to who buys at least Q2) It's obvious that clients of type 2 will use the discount B and P2 E D2 Clients of type 1 will prefer not use the discount because CMg Q1 Q2 Q B + little triangle < E NLP - QUANTITY DISCOUNT Rappel discount The discount depends on the total volume of goods bought, and not from the expense of one time. Discount for homogeneous clients Only one consumer with demand D P P1 , Q1 P1 P2 Maximizes the revenue of the company Company can improve his situation by offering a quantity discount offering P2 to who buys at least Q2 B E A C CMg Q1 Q2 Consumer B + little triangle > E Company A+C+E>A+B Q NLP - PREÇOS POR BLOCOS REVENUE Pm Qm A+B P2 Q2 A+B+C Qm Q2 P Unity above Qm D Pm Consumer A Surplus E P2 Company can do better then C B CMg Qm Q2 Q P2 and PM in E NLP - PREÇOS POR BLOCOS P2 only when Q > Q1 P E>F The consumer will prefer buying Q2, then Qx D It's possible to P1 Revenue of the company by: F Initial price (P1) > PM Q in which the price becomes P2 > QM E P2 CMg Qx Q1 Q2 Q In both cases the P2 must go down for the consumer to buy NLP - TWO PART TARIFF Price equal to a fixed price plus a variable part (proportional to quantity bought ) - Fixed net signature Revenue of the company by making the consumer to consume more than he would do with a constant price - Some sport clubs - Internet - Cellular phones price plans Example of Portugal Telecom P Initially: D P1, Q1 Rate of activation With this tariff it's cheaper to talk after Q1 P1 P2 A and P2 for each more minute The client will keep talking until he reaches Q2 minutes of conversation A B C CMg Q Q1 Q2 Revenue of company NLP - TWO PART TARIFF Heterogeneous clients Two groups with identical number and distinct demand P - A fixed price higher than A + B tends to the exclusion of consumers 1 D2 D1 Company offer a package of Q1 at a global price of A + B, which extracts the surplus of clients 1. They will not buy any additional goods Nevertheless, consumers 2 still demand more quantity, that will be offered at P2 A Revenue of company = P2 C CMg B Q1 Q2 Q 2xA+C NLP - TWO PART TARIFF Heterogeneous clients Other ways of rising the profit Instead of offering additional units at P2, the company could offer an additional package of P + E price P D2 D1 A 1st package at A+B of Q1 units 2st package at A+B+P+E of Q2 units If F > A then by ignoring consumers 1, the company would increase their profit by selling only one package of Q2 units at a price of: F P2 P CMg B E Q1 Q2 Q A+B+P+E+F NLP - QUANTITY AND BLOCK DISCOUNT Different elasticity's of the demand, the company decides to offer the product at different prices P D1 - Package with Q1 units at global price of: A+B+C - Company would like to sell Q2 units at: (to extract all surplus) B+C+D+E+F+G A At this price consumer 2 would buy package 1. For him package 1 would cost: A+B+C B D D2 And his utility would be: E B+C+D CMg C F Q1 G Since D > A Q2 Q surplus NLP - QUANTITY AND BLOCK DISCOUNT The company needs to sell package Q2 for less than A+B+C+E+F+G For the company this price means a revenue bigger in E to the revenue of consumer 2 buying package 1 P D1 Revenue of company: A B D - Consumer buying package 1 A+B - Consumer buying package 2 A+B+E D2 E CMg C F Q1 G Q2 Q PRICE DISCRIMINATION Price discrimination exists when sales of identical goods or services are transacted at different prices from the same provider. lower prices for some consumers Price discrimination higher prices for others. Price discrimination conditions: Monopoly power Firms must have some price setting power, monopolies or oligopolies Elasticity of demand There must be a different price elasticity of demand for the product from each group of consumers. Separation of the market The firm must be able to split the market into different sub-groups of consumers and then prevent discount customers from becoming resellers, and so competitors. PRICE DISCRIMINATION The purpose of price discrimination is to capture the market's consumer surplus and turn it into producer surplus. The aims of price discrimination: To increase the total revenue and/or profits of the supplier! Some consumers do benefit from this type of pricing - they are "priced into the market" when with one price they might not have been able to afford a product. For most consumers however the price they pay reflects pretty closely what they are willing to pay. PRICE DISCRIMINATION A single price (P) is available to all customers. The revenue is represented by area P,A,Q,O. Consumer surplus: area above line segment P,A. P1 is charged to the low elasticity segment, and P2 is charged to the high elasticity segment. The total revenue from the first segment is equal to the area P1,B,Q1,O. The total revenue from the second segment is equal to the area E,C,Q2,Q1. The sum of these areas is greater than the area without discrimination. The more prices that are introduced, the greater the sum of the revenue areas, and the more of the consumer surplus is captured by the producer. PRICE DISCRIMINATION Types of price discrimination First-degree price discrimination The monopolist sells different units of output for different prices and these prices may differ from person to person. Second-degree price discrimination The monopolist sells different units of output for different prices, but every individual who buys the same amount of the good pays the same price. Thus prices differ across the units of the good, but not across people. Third-degree price discrimination The monopolist sells output to different people for different prices, but every unit of output sold to a given person sells for the same price. PRICE DISCRIMINATION First-degree price discrimination Under first-degree price discrimination, each unit of the good is sold to the individual who values it most highly. The value of goods is subjective. A customer with low price elasticity is less deterred by a higher price than a customer with high price elasticity of demand. As long as the price elasticity for a customer is less than one, it is very advantageous to increase the price: the seller gets more money for less goods. With an increase of the price elasticity tends to rise above one. It is assumed that the consumer passively reacts to the price set by the seller, and that the seller knows the demand curve of the customer. In practice there is a bargaining situation: the customer may try to influence the price, such as by pretending to like the product less than he or she really does, and by "threatening" not to buy it. PRICE DISCRIMINATION First-degree price discrimination willingness to pay willingness to pay MC MC quantity quantity Here are two consumers’ demand curves for a good along with the constant marginal cost curve. The producer sells each unit of the good at the maximum price it will command, which yields it the maximum possible profit. PRICE DISCRIMINATION www.cr1.dircon.co.uk First-degree price discrimination The producer’s goal is to maximize its profits subject to the constrain that the consumers are just willing to purchase the good. The outcome will be the Pareto efficiency!! The producer’s profit can’t be increased, since it’s already the maximal possible profit, and the consumer’s surplus can’t be increased without reducing the profit of the producer. PRICE DISCRIMINATION First-degree price discrimination Examples: Bargaining for carpets in Turkey www.fotosearch.de Flower markets in Amsterdam. In a Dutch auction the price starts very high and gradually falls until the first bidder bids and takes the good or service. This means that the price paid is going to be very close to the maximum price the consumer is willing to pay, thereby allowing the producer to extract as much consumer surplus as it possibly can. image58.webshots.com A doctor in a small town who charges his patients different prices, based on their ability to pay. www.themetrofoundation.org PRICE DISCRIMINATION Second-degree price discrimination In the First Degree it’s Hard to discriminate… In perfect price discrimination (First Degree Discrimination): To set the right prices the monopolist has to know the demand curves of the consumers. Not enough: Consumers of one type may pretend to be consumers of another type; No effective way to tell them apart Alternative Method: Construct price-quantity packages that will induce the consumer to choose the package meant for him: Self-selection. PRICE DISCRIMINATION Second-degree price discrimination Price per unit is not constant but depends on how much is bought; Non-linear pricing; Commonly used by public utilities; Price per unit of electricity; Sometimes available in other industries; Bulk discounts for great quantities. PRICE DISCRIMINATION Second-degree price discrimination “Self-selection problem” High end customer would choose to buy x01 at price A with a surplus of B instead of x02 with no surplus. willingness to pay Customer - 2 High-end Customer - 1 Low-end B Quantity: x02 Price: A+B+C Quantity: Price: A x01 One solution: Offer x02 at price A+C A C x01 x02 quantity PRICE DISCRIMINATION Second-degree price discrimination “Reduction of output for consumer 1” willingness to pay Profits increase: Customer - 2 High-end Customer - 1 Low-end The decrease of A is smaller than the increase of C. B A Decreasing x01: A decreases; C increases C x02 x01 x03 quantity PRICE DISCRIMINATION Second-degree price discrimination “Profit maximization solution” Low-demand costumer: willingness to pay • Quantity: x0m Customer - 2 High-end • Price: A • Surplus: 0 B High-demand costumer: Customer - 1 Low-end • Quantity: x02 • Price: A+C+D Point where marginal benefits and costs of quantity reduction balance C • Surplus: B A D quantity x0m x02 PRICE DISCRIMINATION Second-degree price discrimination “In practice” Self-selection encouraged by adjusting the quality of the good instead of its quantity. Example: Airline companies: Business tickets: Other tickets: No restrictions; Stay over Saturday night, buy 14 days in advance, etc; Business travelers are willing to pay for business tickets; Tourists consider the restrictions acceptable; Company profits more than by selling tickets at a flat price. PRICE DISCRIMINATION Third-degree price discrimination Different prices for different people Same price for a given group student’s discounts; senior citizen’s discounts,...; Profit maximization: max[p1(y1)y1 + p2 (y 2 )y 2 - c(y1 + y 2 )] y1 ,y 2 MR1 (y1 ) = MC(y1 + y 2 ) MR2 (y 2 ) = MC(y1 + y 2 ) The marginal cost of producing one extra unit of output must be equal to the marginal revenue in each market PRICE DISCRIMINATION Third-degree price discrimination The market with the higher prices must have the lower elasticity p1 y1 1 - 1 1 = p2 y 2 1 e(y1 ) e(y 2 ) IF (p1 > p2 ) 1- 1 < - 1 1 e1 (y1 ) e2 (y 2 ) e1 (y1 ) < e2 (y 2 ) Standard elasticity formula for marginal revenue PRICE DISCRIMINATION Third-degree price discrimination Example – movie tickets PRICE D1 - Ordinary citizen D2 - Students, Senior citizens If the monopolist can charge only one price, he will charge p1* , but he sells only to Market 1 D1 P1* With price discrimination, it will also sell at p2* to Market 2 P2* D2 q1* Output PRICE DISCRIMINATION Bundling Packages of related goods offered for sale together cost savings Complementarities Dissiminate products (software – the many people use it, the better) Consumers with different preferences good 1 good 2 price = 100 bundle type A 200 100 2 x 100 1 x 300 type B 100 200 2 x 100 1 x 300 400 600 MONOPOLISTIC COMPETITION Definition a market structure in which many firms sell products that are similar but not identical. Characteristics of Monopolistic Competition • Many Sellers - Firms Compete • Product Differentiation - Each firm faces downward-sloping demand curve. • Free Entry - Economic Profits are zero Examples of monopolistic competition: • Books, CDs, movies, computer software, restaurants, sodas MONOPOLISTIC COMPETITION Demand directed to the firm • A firm has its own product portfolio and its own market demand. • Each firm tries to differentiate its product. • The position and the elasticity of the search directed to each product are influenced by the portfolio of existing products in the market. • Demand of each product faces downward-sloping demand curve. • When a new product get into the market, the demand of each initial product it’s modified. P P’ D’ P’’ D’’ y’’ y’ y MONOPOLISTIC COMPETITION Managing in a Monopolistic Competition Market • The market power allows the company to practice prices above the marginal costs (MC), and act like a monopolistic firm. • Product quantity that a firm sells depends on the price they established to the product, like a monopolistic firm. • The presence of other substitute products in the market, make demand more elastic than in the monopolistic market. • The firm has a limited market power. MONOPOLISTIC COMPETITION The Short-Run Equilibrium • Each firm in monopolistically competitive market follows the monopolist's rule for maximizing profit • It chooses the output level where marginal revenue (MR) is equal to the marginal cost (MC) • It sets the price using the demand curve (D) to ensure that consumers will buy the amount produced: P D MC y’ – Firm product amount P’ – Firm Price D – Market Demand MR – Marginal Revenue MC – Marginal Costs ATC – Average Total Costs ATC P’ ATC D’ y’ MR y MONOPOLISTIC COMPETITION The Short-Run Equilibrium • We can determine whether or not the monopolistically competitive firm is earning a profit or loss by comparing price and average total cost (ATC) • If P > ATC, the firm is earning a profit • If P < ATC, the firm is earning a loss • If P = ATC, the firm is earning zero economic profit P D MC y’ – Firm product amount P’ – Firm Price D – Market Demand MR – Marginal Revenue MC – Marginal Costs ATC – Average Total Costs ATC P’ Profit ATC Losses D’ y’ MR y MONOPOLISTIC COMPETITION The Long-Run Equilibrium • When firms in monopolistic competition are making profit, new firms have an incentive to enter the market • This increases the number of products from which consumers can choose. • Thus, the demand curve faced by each firm shifts to the left . • When firms monopolistic competition are incurring losses, firms in the market will have an incentive to exit • Consumers will have fewer products for each to choose. • Thus, the demand curve for each firm shifts to the right. P MC y’ – Firm product amount P’ – Firm Price D – Market Demand d – Firm Demand MR – Marginal Revenue MC – Marginal Costs ATC – Average Total Costs ATC D P’ d y’ MR y MONOPOLISTIC COMPETITION The Long-Run Equilibrium • The process of exit and continues until firms are earning zero profits. • This means that the demand curve and the average total cost curve are tangent to each other • At this point, price is equal to average total cost (ATC) and the firm is earning zero economic profit. P MC y’ – Firm product amount P’ – Firm Price D – Market Demand d – Firm Demand MR – Marginal Revenue MC – Marginal Costs ATC – Average Total Costs ATC D P’ d y’ MR y MONOPOLISTIC COMPETITION Strategies to prevent (or to postpone) the result of Null Profits • Product Differentiation: • Publicity • Introduction of new products • Costumer loyalty • Innovate to prevent the appearing of long-term • Entry barriers • Keep “business secret” and “strategic plans”, in a way to delay the necessary time to competition copy our product MONOPOLISTIC COMPETITION Example - The MEGT Company has estimated the following demand equation to its product: QD = 12000 - 4000P - The firm Total Costs are 4000€ when noting is produced. This costs increases by 0,5€ for each unit produced. TC = 4000 + 0,5Q 1 – We are facing a short-run or a long-run scenario? 2 – Specify the marginal cost function Short-Run MC =0,50 3 – Write an equation for total revenue in terms of output TR = P * QD = (3 - QD / 4000) * QD = 3QD - QD / 4000 2 4 – Specify the marginal revenue function MR = 3 - 2Q / 2000 MONOPOLISTIC COMPETITION Example (cont.) - The MEGT Company has estimated the following demand equation to its product: QD = 12000 - 4000P - The firm Total Costs are 4000€ when noting is produced. This costs increases by 0,5€ for each unit produced. TC = 4000 + 0,5Q 5 – At what level of output will profits be maximized? MC = MR <=> 0.5 = 3 - 2Q / 2000 <=> Q = 5000 6 - What price will be charged? P = 3 - 5000 / 4000 = 1.75 7 – What will total profits or losses be? Pr ofits = P * Q - TC = = (1,75 * 5000) - (4000 + 0,5 * 5000) = = 2250 BIBLIOGRAPHY Mata, J. (2001), Economia da empresa, 2th ed., Fundação Calouste de Gulbenkian, pp. 261-346 Varian, H. (2003), Intermediate Microeconomics: A Modern Approach, 6th ed., W. W. Norton & Co Images http://www.dircon.co.uk http://en.wikipedia.org http://faculty.inverhiks.edu/rmitche/marketing/chap17and18i.htm