Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

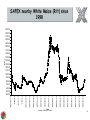

Agricultural Derivatives 101 The Agricultural Products Division of the JSE Copyright © 2005 JSE Limited Agriculture in South Africa • 3,5 – 4,0% contribution to GDP (but 40% of population dependant on agriculture) • 10% of South African exports (by value) • Major agric export earner = sugar (maize, wine, fruit) • Farmers: 50 000 commercial 240 000 small scale farmers 3m subsistence farmers • 13% of South Africa is arable land (only 20% is high potential) • Major limiting resource is WATER • RSA = 6% of African population 4% of African land area 25 – 30% of maize produced in Africa 10% of wheat produced in Africa 50 – 60% of maize produced in SADC Copyright © 2005 JSE Limited . 2 Agriculture in South Africa • 1930 – early 90’s Regulated Marketing Centralized marketing Centralized price determination • 1995 Agricultural market deregulated Control Boards / Marketing Boards scrapped NO centralized price determination Copyright © 2005 JSE Limited . 3 Agricultural marketing in South Africa is a whole new ball game in a deregulated market place Agricultural marketing in South Africa is a whole new ball game in a deregulated market place Agricultural Markets • Regulated Advantages: Disadvantages: • Free Market Disadvantages: Advantages: No price risk Information supply Cost to economy Distortion to economy Price Risk Information Unfair Competition Opportunities Economic Basis Copyright © 2005 JSE Limited . 6 Challenges of the Free Market • • • • Unfair Competition – not level playing field One sided – inputs / outputs (no link) Requires decisions Requires sourcing and interpretation of information • Does not respect tradition or history • Makes use of technological progress Copyright © 2005 JSE Limited . 7 Background to Derivatives • Mesopotamia, China, France, USA - agriculture • Fluctuating Prices depending on supply and demand of product • Forward Contracts • Standardized Forward Contracts to facilitate trading • Add guarantee to the market • Futures Contracts • Financial Markets Copyright © 2005 JSE Limited . 8 A futures market is... • A trading operation that provides market participants with a price determination mechanism and a price risk management facility through which they can manage their exposure to adverse price movements on the underlying physical market and where performance by both counterparties to the contract is guaranteed Copyright © 2005 JSE Limited . 9 It is NOT a “get rich quick” scheme Copyright © 2005 JSE Limited …. it is to avoid losing money! Copyright © 2005 JSE Limited The Agricultural Derivatives Market in South Africa • • • • • • • Establishment of the South African Futures Exchange (SAFEX) in 1988 to trade financial derivative instruments Establishment of the Agricultural Markets Division of SAFEX in 1995 separate membership start-up capital raised by the issue of seats Initial futures contracts (chilled beef and potatoes) not successful White and yellow maize contracts listed in 1996 August 2001 - became Agricultural Products Division of the JSE Securities Exchange South Africa Presently trade maize, wheat, sunflower seeds and soyabean futures and options contracts Recognised as the price discovery facility for grains in South and Southern Africa Copyright © 2005 JSE Limited . 12 futures contracts ..... • standardised agreement through exchange (product, quality, quantity, time & place) • indirect locked-in price • physical delivery not implied • profit / loss profile exactly opposite to physical market • basis risk • margins payable Copyright © 2005 JSE Limited WHY use a futures market ? ..........for two very good reasons ! • price determination and • price-risk management Copyright © 2005 JSE Limited Maize Price determinants • South African Demand and Supply - role of weather - input suppliers - crop estimates committee • Regional Demand and Supply - actual economic demand ? • International Demand and Supply • Exchange Rates Copyright © 2005 JSE Limited . 15 Price determination ...... • futures exchanges do not set prices, they are free markets where the forces that influence prices, notably supply and demand, are brought together in a transparent way. Copyright © 2005 JSE Limited How are prices determined? by brokers representing clients who trade on a trading floor (pit) or electronically on a trading screen the trading screen reflects the best bids (highest) and offers (lowest). Copyright © 2005 JSE Limited JAN 96 BEEF FUTURES CONTRACT 9.75 9.25 8.75 NABI 8.25 7.75 JAN FUTURE 7.25 6.75 O N D J 20 /06 07 /20 /07 03 22 /20 /07 03 06 /20 /0 03 21 8/20 /0 03 05 8/20 /09 03 22 /20 /09 03 08 /20 /10 03 23 /20 /10 03 07 /20 /11 03 24 /20 /11 03 09 /20 /12 03 29 /20 /1 03 14 2/20 /01 03 29 /20 /01 04 13 /20 /02 04 01 /20 /03 04 16 /20 /03 04 01 /20 /04 04 21 /20 /04 04 07 /20 /0 04 24 5/20 /05 04 08 /20 /06 04 24 /20 /06 04 09 /20 /07 04 /20 04 R/TON July 04 White Maize 1700 1600 1500 1400 1300 1200 1100 1000 900 800 DATE Copyright © 2005 JSE Limited 19 . Copyright © 2005 JSE Limited 2005/04/14 2005/03/31 2005/03/17 2005/03/03 1100 2005/02/17 2005/02/03 2005/01/20 2005/01/06 2004/12/23 2004/12/09 2004/11/25 2004/11/11 500 2004/10/28 2004/10/14 2004/09/30 2004/09/16 2004/09/02 2004/08/19 2004/08/05 2004/07/22 2004/07/08 2004/06/24 2004/06/10 R/Ton July 05 White Maize 1300 1200 Possibility to lock in prices of +/- R1000/t 1000 900 800 700 600 Realization of large carry over and good planting possibilities 400 Date 20 . Copyright © 2005 JSE Limited 25/10/2005 18/10/2005 11/10/2005 04/10/2005 27/09/2005 20/09/2005 13/09/2005 06/09/2005 30/08/2005 23/08/2005 16/08/2005 09/08/2005 02/08/2005 26/07/2005 19/07/2005 12/07/2005 05/07/2005 28/06/2005 21/06/2005 14/06/2005 07/06/2005 31/05/2005 24/05/2005 17/05/2005 10/05/2005 03/05/2005 26/04/2005 19/04/2005 12/04/2005 05/04/2005 29/03/2005 R/Ton July 06 White Maize 950 900 850 Where to next ?? 800 750 700 650 600 Date 21 . SAFEX nearby White Maize (R/t) since 1998 R/Ton 2300.00 2200.00 2100.00 2000.00 1900.00 1800.00 1700.00 1600.00 1500.00 1400.00 1300.00 1200.00 1100.00 1000.00 900.00 800.00 700.00 600.00 500.00 400.00 24/08/2005 31/03/2005 04/11/2004 14/06/2004 19/01/2004 22/08/2003 28/03/2003 31/10/2002 10/06/2002 11/01/2002 16/08/2001 19/03/2001 24/10/2000 06/01/2000 01/06/2000 08/11/1999 15/3/99 21/10/98 29/5/98 01/05/1998 Date Copyright © 2005 JSE Limited . 22 Price-risk management instruments .. • state intervention • hold physical stocks • forward contracts • futures contracts • options Copyright © 2005 JSE Limited To hedge or not to hedge, that is the question! Whether it is better for farmers in the production of maize to suffer the ups and downs of outrageous maize prices, or to take precautions against a sea of uncertainty and by managing price risk, end the uncertainty. RMGB (with apologies) Guarantee in Market • Structure of the market • Margin Payments - initial margin - variation margin Copyright © 2005 JSE Limited . 25 Structure of the Exchange Clearing House Clearing Member Broker Client A Client B Client C Clearing Member Trade Broker Copyright © 2005 JSE Limited Client X Client Y Client Z Margin Flows Date price Contract value Contract Action acc. Seller’s Buyer’s acc. 8/3 R550 R55000 init. margin R10000 R10000 11/3 R545 R54500 var. margin R10500 R500 R10000 (R500) 12/3 R547 R54700 var. margin R10300 R200 R10200 15/3 R540 R54000 var. margin R11000 R700 R10000 (R500) 17/3 R520 R52000 var. margin R13000 R2000 R10000 (R2000) 18/3 R510 R51000 var. margin R14000 R1000 R10000 (R1000) Seller receives margin R10000 plus profit R4000 (R550-R510 x 100) from the futures market and R510/t from the physical market. Buyer receives margin R10000, but has lost R4000 (which as a hedger will be compensated for by a lower physical purchase cost: R510/t). Copyright © 2005 JSE Limited . 27 ...... by using the futures market individuals, companies or countries selling or buying a commodity can protect themselves against price movements in the underlying physical market. This is achieved by selling or buying futures or options contracts through a broker who is a member of the futures exchange. Copyright © 2005 JSE Limited Requirements for a Successful Agric Futures Market • Liquidity in underlying spot market (volume of production, multiple buyers and multiple sellers) • Commodity must be able to be standardized • Price must be volatile (must be a need for price risk management) • No state intervention in the price making mechanism • Guaranteed contract performance (clearing & financial system) • Deliverability (infrastructure / grading regulations / warehouse receipts) Copyright © 2005 JSE Limited . 29 Growth of the Market... Copyright © 2005 JSE Limited . 30 Total contracts traded – futures and options 2500000 Futures Options 2000000 Contracts 1500000 1000000 500000 0 1998 1999 2000 2001 Copyright © 2005 JSE Limited 2002 2003 2004 . 31 Physical delivery in completion of a futures contract…. Copyright © 2005 JSE Limited Delivery starts at the silo …. Copyright © 2005 JSE Limited . 33 Why allow for physical delivery on the futures market. • no underlying cash market to base prices off – therefore no cash index available to settle the futures contract • guaranteed delivery to the buyer of a Safex silo receipt representing good delivery • guaranteed payment to the seller • standardisation of the contract is required (quantity, quality, place, storage) Copyright © 2005 JSE Limited . 34 Delivery onto Safex…. • physical delivery is a two day process on Safex, first the notice day followed by the delivery day • delivery can take place anytime during the delivery month ie May • commodity is deliverable all months of the year, five main hedging months with the remainder as constant delivery months • short position holder gives notice any time during the delivery month • long position holder is randomly allocated commodity as deliveries are received Copyright © 2005 JSE Limited . 35 DECEMBER 2004 M T W T F S S 30 30 11 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 21 22 23 24 25 26 27 28 29 30 30 31 31 Copyright © 2005 JSE Limited . 36 Initial margin requirements • Contracts traded before delivery require R10000 for white and yellow maize, • Extended price limits margins increase • on the first delivery day margins move to R13000 per contract and price limits removed, • from last trading day to expiry, margins are increased to R23000 per contract, Copyright © 2005 JSE Limited . 37 Detail required for delivery… • A short futures position is required in the particular delivery month before any notice can be tendered • Short position holder tenders notice through his broker – the following information is required • • • • silo receipt number quantity location date storage is paid to • Delivery notice is faxed/emailed to Safex before 12h45 on notice day Copyright © 2005 JSE Limited . 38 Copy of a delivery notice SAFEX DELIVERY NOTICE WHITE MAIZE FUTURES CONTRACT JSE VAT REGISTRATION NUMBER: 4080119391 TAX INVOICE NUMBER: WMAZ286 The undersigned short position holder hereby give notice to the Clearing House of intention to deliver as follows: Delivery Notice Ref WMAZ286 SHORT POSITION HOLDER ClientCode xyz19 MemberCode TTT ClearingMemberCode STDC NoticeDate 08-Jul-03 DeliveryDate 09-Jul-03 FuturesContract JUL 2003 WMAZ NumberOfContracts 46 QuantityTons 4600 Receipt Number 808163 806232 806200 806219 806245 795444 793299 792271 791772 Quantity 200 1000 1000 1000 1000 100 100 100 100 Silo Owner SWK SWK SWK SWK SWK SWK SWK SWK SWK Silo Location Schuttesdraai Werda Werda Werda Werda Werda Mirage Buckingham Vierfontein Storage Paid To 07-Jul-03 01-Jul-03 01-Jul-03 01-Jul-03 01-Jul-03 27-Jun-03 20-Jun-03 12-Jun-03 18-Jun-03 Days Storage 2 8 8 8 8 12 19 27 21 Storage Due Per Ton 0.62 2.48 2.48 2.48 2.48 3.72 5.89 8.37 6.51 Loc Diff PerTon 67 63 63 63 63 63 62 42 57 Discount PerTon TotalDiscount 67.62 65.48 65.48 65.48 65.48 66.72 67.89 50.37 63.51 13524 65480 65480 65480 65480 6672 6789 5037 6351 TOTAL DISCOUNT R300,293.00 For Clearing House use only: CLOSING FUTURE'S PRICE ON DAY PRIOR TO DELIVERY DAY GROSS INVOICE AMOUNT NET INVOICE AMOUNT DUE TO SHORT POSITION HOLDER R852.00 R3,919,200.00 -------------------R3,618,907.00 --------------------------------------AGRICULTURAL PRODUCTS DIVISION A DIVISION OF THE JSE SECURITIES EXCHANGE One Exchange Square Gwen Lane Sandown Copyright © 2005 JSE Limited Delivery Notice WMAZ286 Page 1 of 1 . 39 Copy of a assignment notice SAFEX ASSIGNMENT NOTICE WHITE MAIZE FUTURES CONTRACT JSE VAT REGISTRATION NUMBER: 4080119391 TAX INVOICE NUMBER: WMAZ286 The undersigned short position holder hereby give notice to the Clearing House of intention to deliver as follows: Delivery Notice Ref WMAZ286 SHORT POSITION HOLDER ClientCode CYH20 MemberCode ABL ClearingMemberCode VKSC NoticeDate 08-Jul-03 DeliveryDate 09-Jul-03 FuturesContract JUL 2003 WMAZ NumberOfContracts 46 QuantityTons 4600 Receipt Number 808163 806232 806200 806219 806245 795444 793299 792271 791772 Quantity 200 1000 1000 1000 1000 100 100 100 100 Silo Owner SWK SWK SWK SWK SWK SWK SWK SWK SWK Silo Location Schuttesdraai Werda Werda Werda Werda Werda Mirage Buckingham Vierfontein Storage Paid To 07-Jul-03 01-Jul-03 01-Jul-03 01-Jul-03 01-Jul-03 27-Jun-03 20-Jun-03 12-Jun-03 18-Jun-03 Days Storage 2 8 8 8 8 12 19 27 21 Storage Due Per Ton 0.62 2.48 2.48 2.48 2.48 3.72 5.89 8.37 6.51 Loc Diff PerTon 67 63 63 63 63 63 62 42 57 Discount PerTon TotalDiscount 67.62 65.48 65.48 65.48 65.48 66.72 67.89 50.37 63.51 13524 65480 65480 65480 65480 6672 6789 5037 6351 TOTAL DISCOUNT R300,293.00 For Clearing House use only: CLOSING FUTURE'S PRICE ON DAY PRIOR TO DELIVERY DAY GROSS INVOICE AMOUNT NET INVOICE AMOUNT DUE TO SHORT POSITION HOLDER R852.00 R3,919,200.00 -------------------R3,618,907.00 --------------------------------------AGRICULTURAL PRODUCTS DIVISION A DIVISION OF THE JSE SECURITIES EXCHANGE One Exchange Square Gwen Lane Copyright © 2005 JSE Limited Sandown . 40 Delivery Notice WMAZ286 Page 1 of 1 Settlement as follows… • broker will deliver silo receipt by 12h00 on the delivery day • silo receipt has to be signed off • payment is finalised by 12h00 on delivery day • buyer’s broker can pick up silo receipt from 14h00 on delivery day • initial margin to both buyer and seller will be returned the following day Copyright © 2005 JSE Limited . 41 Lets step outside for some refreshments….. Copyright © 2005 JSE Limited . 42 Welcome back ! Lets look at your “OPTIONS” Copyright © 2005 JSE Limited DUCK or DIVE Hope you’ve taken out travel insurance ! Copyright © 2005 JSE Limited . 44 Price-risk management instruments .. • state intervention • hold physical stocks • forward contracts • futures contracts • exchange traded options Copyright © 2005 JSE Limited OPTIONS….another type of insurance! Fire Hail R/TON White Maize PRICE RISK Yellow Maize DATE Drought Floods Copyright © 2005 JSE Limited . 46 Futures vs Options • as a buyer, fundamentally different risks • buyer and seller of futures assume the same risk, and face a legally binding obligation – margin requirements • seller of an option has legally binding obligation if the option is exercised • buyer of an option has no legally binding obligation, BUT to pay for the option (premium) • the most a buyer of an option can lose is the price paid for the option (the premium agreed on) • the seller of an option is potentially exposed in the same fashion as a futures contract (variation margin) Copyright © 2005 JSE Limited willing buyer\willing seller • Two types of options: – PUT options (floor price insurance) A farmer would buy this instrument – CALL options (ceiling price insurance) Millers interested in this insurance Copyright © 2005 JSE Limited . 48 Buying floor price insurance…. • as a buyer of floor price insurance (PUT options) you buy the RIGHT but not the obligation to sell maize at an agreed floor price • a seller of PUT options is OBLIGATED to buy your product should you exercise your right • the PUT option trade involves a willing buyer\willing seller at an agreed premium for a specific strike price • the buyer can exercise the right to sell maize at any time (American style options) • the buyer pays premium (negotiated on market) • seller receives the premium, but is margined by the exchange to make sure that he can meet his commitment Copyright © 2005 JSE Limited . 49 Option terms ? • Premium the price you agree to pay for an option • Strike price the price at which you buy or sell the product will be in R20 price intervals for APD • Volatility in simple terms it’s a measure of how fast or slow the market is moving over a given time period regardless of direction. In other words it tells what the probability is of a price occurring within a certain time period Copyright © 2005 JSE Limited . 50 When is your option worth something ? • in-the-money: option which is made up of both time and intrinsic value. In the case of a put the strike price is above where the market is trading • at-the-money : the premuim consists of time value and the strike price is near to the current trading levels • out-the-money :the premium is entirely time premium. With puts the strike price is below the market trading levels Copyright © 2005 JSE Limited . 51 Illustration for Put Options Current market trading at R620 800 Put In the money by R180 720 Put In the money by R100 620 Put At the money 580 Put Out the money by R40 400 Put Out the money by R220 Copyright © 2005 JSE Limited . 52 Premium costs Bid Offer Jul WMAZ 660 P 2000 per contract ie R20 per ton 2500 Jul WMAZ 700 P 4000 4800 Jul WMAZ 720 P 6000 6500 Jul WMAZ 780 P 8000 9000 The higher the floor price you want the more it will cost you Copyright © 2005 JSE Limited . 53 An producer example..no 1 • Farmer Brown would like to manage his price risk using Put options: – He buys a JulWMAZ 700 Put for R60 in Dec the previous year – In June when the option contract expires, the underlying market is trading at R900….. The put option expires worthless and he sells his maize at R900 less the premium cost of R60, therefore R840 Safex price, after hedging he still makes an additional R140 Copyright © 2005 JSE Limited . 54 An producer example..no 2 • Farmer Brown would like to manage his price risk using Put options: – He buys a JulWMAZ 700 Put for R60 in Dec the previous year – In June when the option contract expires, the underlying market is trading at R700….. The put option expires at the money and no option is automatically exercised. He can sell his maize in the cash market for R700 less the premium cost of R60, therefore R640 Safex price as per his original hedge price Copyright © 2005 JSE Limited . 55 An producer example..no3 • Farmer Brown would like to manage his price risk using Put options: – He buys a JulWMAZ 700 Put for R60 in Dec the previous year – In June when the option contract expires, the underlying market is trading at R500….. The put option expires in the money by R200, he exercised his option and sells his maize at R700 less the premium cost of R60, therefore attaining the R640 Safex price, by hedging he has achieve a price which is R200 better then no hedge at all Copyright © 2005 JSE Limited . 56 Buying options to manage price risk can only result in a win-win situation, once you have decided on the relevant strike price and paid the premium, if it expires in the money you have read the market well and reap the rewards, if it expires out the money you lose the premium but can sell your product at a higher market price CJS (with sincere apologies) Copyright © 2005 JSE Limited . 57 Buying ceiling price insurance…. • as a buyer of CALL options you buy the RIGHT but not the obligation to BUY maize at an agreed ceiling price • a seller of CALL options is OBLIGATED to sell you product should you exercise your right • the CALL option trade involves a willing buyer\willing seller at an agreed premium for a specific strike price • the buyer can exercise the right to BUY maize at any time (American style options) Copyright © 2005 JSE Limited . 58 Illustration for Call Options Current market trading at R620 400 Call In the money by R220 560 Call In the money by R80 620 Call At the money 700 Call Out the money by R80 780 Call Out the money by R160 Copyright © 2005 JSE Limited . 59 Bid Offer Jul WMAZ 660 C 8000 8500 Jul WMAZ 700 C 6000 6500 Jul WMAZ 720 C 4000 4500 Jul WMAZ 760 C 2000 3000 The lower the ceiling price, the higher the price (premium) of the option Copyright © 2005 JSE Limited . 60 WITH THE HELP OF A REGISTERED JSE AGRICULTURAL BROKER, BE GUIDED TO MAKE THE RIGHT DECISIONS ! Copyright © 2005 JSE Limited . 61 Failure is an opportunity to begin again, more intelligently – Henry Ford Copyright © 2005 JSE Limited . 62