Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Economic calculation problem wikipedia , lookup

Brander–Spencer model wikipedia , lookup

Supply and demand wikipedia , lookup

Criticisms of the labour theory of value wikipedia , lookup

Marginal utility wikipedia , lookup

Production for use wikipedia , lookup

Marginalism wikipedia , lookup

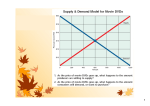

Differentiation, Curve Sketching, and Cost Functions Assumptions • When applying calculus to economics we are making approximations. True functions in economics jump from value to value. However, because the jumps are small, we can approximate with continuous functions. • We assume that the approximations are close to the actual functions. • At some point the cost functions will reach optimal values for total output. • We also assume that all economic factors remain constant. (e.g. inflation, price of supplies, demand for product, etc…) Assumptions • • • • • • • • • Desired output level is attainable. There are both fixed and variable cost. There is a positive fixed cost. Total cost increases as total quantity produced increases. At low levels of production the marginal cost decreases as production as increases. At high levels of production, the marginal cost increases as the production increases. The cost of production for a quantity, q, can be approximated by a twice continuously differentiable function: C(q). Quantity, q, is always positive. The objective of the firm is to maximize profits. Cost of Production Cost is defined as the value of everything a seller must give up to produce a good. For a given level of production, q, the cost function is C(q). This cost function will take into consideration both the variable and fixed costs. In regards to the cost function, C(q), • C(q) has a positive y-intercept • C(q) is increasing • For an interval 0 < q < q*, C(q) is concave down. • For the interval q* < q < , C(q) is concave up. Marginal Cost of Production • Marginal cost is defined as the increase in total cost that arises from an extra unit of production. • Marginal Cost, MC(q), can be found by calculating the derivative of the cost function, C’(q). MC(q) = C’(q) • C(q) always has a positive slope, therefore Marginal Cost is always positive. • Marginal cost is at a minimum where it’s derivative is 0. MC’(q) = 0 • The graph of the Marginal Cost function first decreases, reaches a minimum, then increases. • The minimum of the Marginal Cost function occurs at the same production quantity, q, as the inflection point of C(q). Average Cost of Production • Average Cost, AC(q), is defined as the total cost divided by total quantity, C(q) / q. AC(q) = C(q) / q • AC(q) will always be positive. • AC(q) approaches infinity as q approaches 0. • AC(q) has a minimum at AC’(q) = 0 which occurs when AC(q) = MC(q). This is the only point at which these lines intersect. Demand and Revenue • There is a given demand function, D(q), which determines the price the firm can charge for it’s goods. • The graph of demand function, D(q), will show the relationship between the price of a good and the quantity demanded. • Revenue, R(q), is determined by multiplying D(q) by the production quantity, q. R(q) = D(q) * q Marginal Revenue and Profit • Marginal revenue is defined as the change in total revenue from an additional unit sold. • Marginal Revenue, MR(q), can be found by taking the derivative of the Revenue function. MR(q) = R’(q) • The quantity, q, at which profit is maximized is found when the Marginal Revenue is equal to the Marginal Cost. MR(q) = MC(q). • Profit is determined by subtracting the total cost from the total revenue. Profit = R(q) – C(q) Model Interpretations • This model is built on the assumptions that our firm is in a economic vacuum. In reality economic factors would be constantly change. • Mathematically, the model provides accurate results given the Cost function, C(q), and Demand function, D(q), are correct. Questions?