Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

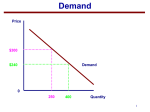

Intermediate Microeconomic Theory Market Demand 1 Market Demand Given an individual i’s endowment and preferences, we’ve seen how to calculate an individual’s demand curve for each good, q1i(p1) We want to use our individual consumer theory as basis for analyzing consumer behavior in the market (which is what we really care about). Market Demand - sum of all of the individual consumer’s n demand at each price, or Q1 ( p1 ) q1i ( p1 , p2 , mi ) i 1 2 Market Demand (Graphically) Consider a market with two individuals. p1 p1 p1 10 10 10 7 7 7 4 4 4 20 40 q1i 10 30 q1j 20 20+10=30 70 Q1d 3 Market Demand (cont.) Two margins for changes in demand: *Intensive margin – the change in demand due to each individual consumer already in the market at one price buying more/less as price changes (due to the downward slope of each individual demand curve). *Extensive margin – the change in demand arising from the change in quantity bought due to changes in the number of individuals who buy a good changes as price changes. So even if each consumer only demands one unit at most of given good (e.g., a washing machine), extensive margin will still mean that market demand will be smooth and downward sloping. 4 Market Demand (Graphically) Individual and Market demands for Washing Machines Suppose there are 100 individuals of each “type” (i.e. willingness to pay for a washing machine) Consider what happens if we allow for many different types. pw 1000 800 600 1 qw,1 1 qw,2 1 qw,3 100 200 300 Qw 5 Market Demand (Graphically) Consider again the market with two individuals. Increase in demand from fall in price from $9 to $7, how much happens at intensive margin vs. extensive margin? How about for fall in price form $7 to $5? p1 p1 p1 10 10 10 9 9 9 7 7 7 5 5 5 10 20 30 40 q1i 10 20 30 q1j 10 20 30 50 Q1d 6 Market Demand (cont.) Market Demand curve for good 1 tells us how the demand for good 1 changes as its price changes -- holding all other prices and incomes constant! However, we developed market demand curve from our micro foundations of behavior. Therefore, we can understand how market demand curve for one good will change given changes in prices of other goods or changes in the income distribution. 7 Market Demand (cont.) Examples: What would happen to the market demand curve for ski lift tickets if the price of skis increased? If organic food is a normal good for most people, how will an increase in incomes affect the market demand curve for organic food? 8 Measuring the responsiveness of demand Why are we interested in deriving and analyzing demand curves? One key reason is that we want to know the responsiveness of demand to a change in its price. This will relate to what characteristic of a demand curve? What might I mean by the units problem? 9 Elasticity of Demand Economists generally describe responsiveness of demand via Elasticities Price elasticity of demand – percentage change in quantity demanded divided by the percentage change in price. Q1d p1 Q1d ( p1 ) Q1d 1 ( p1 ) d p1 p1 Q1 ( p1 ) p1 “What is the percentage change in quantity demanded due to a percentage change in price?” So if we consider marginal or very small changes in price, Q1d p1 1 ( p1 ) p1 Q1d ( p1 ) slope of the demand curve ratio of price to quantity demanded 10 Calculating Market Demand and Price Elasticity of Demand Suppose everyone has endowment of $m and Cobb-Douglas preferences of form: U = q1 a q 2 b If each individual has $m, what is each individual’s demand curve for good 1? Market demand curve? * with 3 people? * with N people? * For N people, what is Demand Elasticity for good 1 at any given p1? 11 Elasticities So implicit in Cobb-Douglas utility functions is the assumption of a constant demand elasticity of -1 How do we interpret this in words? Do all demand curves have constant elasticity of demand? Consider a very simple linear demand curve QD1(p1) = 100 – p1. What does demand curve look like? What is demand elasticity? 12 Elasticity (cont.) Since demand curves have negative slope (∂Qd/ ∂p < 0), price elasticities are negative. However, we talk about elasticities in absolute magnitudes (e.g. good with elasticity of -3 more elastic than good with elasticity of -2) When ε(p) < -1 (i.e. further from zero than -1) at a given price, we say at good has an elastic demand at that price. Increase in price by 1% , demand decreases by more than 1%. When ε(p) = -1 at a given price, we say good has a unitary elasticity of demand at that price. Increase in price by 1% , demand decreases by 1%. When -1 < ε(p) < 0 (i.e. closer to zero than -1) at a given price, we say good has an inelastic demand at that price. Increase in price by 1% , demand decreases by less than 1%. 13 Taxes and Demand Elasticity One reason we care about elasticity of demand is with respect to tax policy. Suppose we want to raise some funds by taxing a certain good. 14 Taxes and Demand Elasticity Consider a percentage tax t on each unit sold (e.g. a sales tax of 10%). So consumers pay p(1+t) for each unit of good. Will an increase in the tax necessarily lead to more revenue? Show analytically? Show graphically? 15 Taxes and Demand Elasticity Relatively elastic demand $ Relatively inelastic demand $ p(1+t) p(1+t) Tax Revenue (TR) w/ rate t p Tax Revenue (TR) w/ rate t p Q(p(1+t)) Q(p(1+t)) 16 Taxes and Demand Elasticity Now consider an increase in the tax rate from t to t’ Relatively elastic demand $ Relatively inelastic demand $ p(1+t’) p(1+t’) increase p(1+t) in TR decrease in TR p(1+t) increase in TR decrease in TR p Q(p(1+t’)) Q(p(1+t)) Q(p(1+t’)) Q(p(1+t)) 17