Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

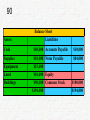

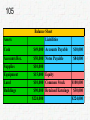

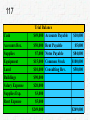

Lesson 1 2 • There are generally three types of businesses: – Manufacturing Businesses – Merchandising Businesses • Wholesale • Retail – Service Businesses • Some services involve products – E.g., restaurants – CD calls them combination businesses 3 • We will focus on corporations – 20% of US businesses • There are other entities (Business forms) – Different financial statements – Examples: • Sole proprietorships – 70% of US businesses • Partnerships – 10% of US businesses • Other entities as well 4 • With Partnerships & Sole Proprietorships – Owner(s) treated as doing business • Business debts are debts of the owners – Unlimited Liability • Corporations – Legal entities separate from their owners. • Business debts are corporation's debts – not the owner's debts. • Shareholders have limited liability • Limited Liability – shareholders can only lose their investment – nothing more 5 • How will corporation be financed? – Funds from You – Funds from Third Parties • Debt vs. Equity – Debt - Advantages » Owner keeps control of corporation – Debt – Disadvantages » Owner has to repay » Owner has to pay interest 6 – Equity – Advantages • Owner doesn’t have to pay interest – Dividends do not have to be paid • Owner doesn’t have to repay – Equity – Disadvantages • Owner dilutes control over corporation 7 • Once the business is created, the owner receives: – Operating profits / losses – Capital gains / losses when business sold 8 • Accounting – information system • provides reports to stakeholders • Information on economic activities and condition of a business 9 • A lot of people interested in how business is doing. – Business Stakeholder • person or entity that has an interest in the economic performance of the business • Stakeholders include – – – – – – owners, managers, employees, customers, creditors, and various government agencies • All stakeholders use accounting data 10 Stakeholder A. Owner Interested In Sales Profit Cash B. Investors/ Profit Stockholders Dividends C. Bankers Debts Reason Is advertising effective? Can I take home more money each week? Can I afford to buy more equipment? Is my investment making money? What dividends are being paid? Can this business repay a loan? 11 Stakeholder Interested In D. IRS Profit E. Managers Expenses Sales F. Employees Profit Reason What taxes does this business owe? Am I keeping expenses within my budget? Will I be eligible for a bonus this year? Can my company afford raises? Is my job secure? 12 Stakeholder G. Customers Interested In Amount spent on warranty Reason How dependable is this product? Is the company going to be in business in the future? H. Competitors • Amount spent on ads How do I compare to my competitor? Competitors get valuable information from financial statements • So, companies disclose as little detail as possible 13 • Accountants have to act ethically. – Not just a case of morals. – Ethical violation can also lead to civil or criminal liability for the violation • Civil – Malpractice – Lose license • Criminal – Go to Jail 14 • Profession of accounting is varied. – Private accounting • Accountants work for their clients – e.g., Controllers – Public accounting • Accountants - independent of clients – e.g., CPAs 15 • Financial accounting - preparation of general purpose financial statements – primarily for outsiders • investors, • government regulators, and • creditors – Done by internal accountants • then certified by the public accountants 16 • Managerial or management accounting – preparation of internal reports • for the management of the company • Tax accounting – Preparation of tax returns • Either private or public accountants 17 • Financial statements prepared using GAAP – Generally Accepted Accounting Principles (GAAP) – Set of rules that all accountants follow • in preparing financial statements 18 • Didn’t always have GAAP. • Basic rules developed during Renaissance • Up to 1933 - free to use whatever rules you want 19 • With the 1929 crash, federal government passed: – The Securities Act of 1933 and – The Securities Exchange Act of 1934 • Most publicly traded corporations now must follow rules set by Securities Exchange Commission (SEC) – In preparing financial statements 20 • SEC allows accounting profession to establish GAAP – Now set by FASB • Financial Accounting Standards Board (FASB) • There were prior organizations – If the SEC isn't happy with GAAP, then • Can require different rules with governmental filings and reports to shareholders 21 • GAAP reflects concepts/assumptions used in preparing financial statements. – Relevance • Information is relevant if it will influence investment decisions – Reliability (Credible) • Information should be materially accurate 22 – Comparability • Information is presented so decision makers can recognize similarities, differences, and trends over different time periods or between different companies. – Follow same general rules – Consistency • accounting procedure, once adopted, should continue to be used. – Rules for changing accounting rules to follow. 23 – Business Entity Concept (Separate Entity Concept) • Each business accounted for as an individual organization. – Even though you are a sole proprietorship » (Not a separate legal entity), » Financial statements only cover the business operations. » Do not include your personal assets and income. 24 – Cost Concept • Most transactions recorded at historical cost. • building recorded using purchase price, not FMV – Objectivity Concept • Accounting reports should be based upon objective evidence. – Conservatism • Accountants should value items conservatively. 25 – Unit of Measure Concept • Financial statements prepared using domestic currency of corporation – Continuity Assumption (Going Concern Assumption) • Assume company will not be going out of business. • Example – Inventory valued at price paid » Not liquidation value 26 • CD says Three General Purpose Financial Statements: – Balance Sheet – Income Statement – Statement of Cash Flows • There is a fourth Corporate Statement – Statement of Retained Earnings 27 • Balance Sheet – prepared as of a given date – usually the end of reporting period. • Corporations can use calendar year or fiscal year – Fiscal year is 12-month period other than a calendar year – reports the financial position of the company as of a given date. 28 • Balance Sheet reports: – Assets, – Liabilities, and – Net worth of the company. • Balance Sheet usually uses original cost – Not FMV – Doesn’t show current value of the company. 29 • Income Statement – reports results of company’s operations for the reporting period. – Dated "For [Period] Ended [Date].“ • Example - "For the Year Ended December 31, 1998." 30 • The Income Statement reports: – revenues, – expenses and – net income • This information given for the period in question 31 • Equity section of a corporate balance sheet – Divided into two parts. • Paid In Capital – Also called “Contributed Capital” – Shows equity contributed by shareholders • Retained Earnings – Shows earnings that corporation earns and keeps » Not paid as dividends • Statement of Retained Earnings – explains how Retained Earnings changed from last year to this year. 32 Statement of Retained Earnings For the Year Ended __________________ Beginning Balance of Retained Earnings XXXXX Plus Net Income for the Year XXXXX Less Dividends for the Year (XXXXX) Ending Balance of Retained Earnings XXXXX 33 • Accrual Method – Used by most publicly traded corporations. – Revenue - when you earn it • Not when you receive it – Expenses when you owe them • Not when you pay them • Accountants prefer accrual method – Match revenues with expenses that generated them. 34 • Cash method – Revenue - reported when received – Expenses - reported when paid • Accounts don’t like Cash method – Companies can manipulate their income. 35 • Statement of Cash Flows – Introduced around 1986 – Reports cash inflows and outflows • From operations – what it does for a living, • From investing – purchases and sales of equipment, real estate and other assets • From financing – stock and debt transactions • Statement of Cash Flows explains how cash changed during the year. 36 Statement of Cash Flows For the Year Ended _____________ Cash Flows From Operations (Details given line by line like an Income Statement): Cash Flows From Investing (Details given line by line like an Income Statement): Cash Flows From Financing (Details given line by line like an Income Statement): Cash Flows For the Year: Plus Balance of Cash at Beginning of Year: Balance of Cash at End of Year XXXXX XXXXX (XXXXX) XXXXX XXXXX XXXXX 37 • Notes to the Financial Statements – At end of financial statements – Notes convey great deal of important information on: • What accounting rules were followed. • Additional details about figures appearing in statements. • Additional information not appearing in statements – E.g., lines of credit, bank covenants & contingent liabilities 38 • Financial statements accompanied by letter from the CPAs preparing the statements. – Describes how the audit was conducted, – States CPA's opinion on whether financial reports were prepared in accordance with GAAP 39 • BALANCE SHEET – Imagine that you want to report your wealth (net worth). • Maybe you want to borrow money • Creditor wants to know you can pay loan back loan. – If you own a house you bought for $250,000. • You could report that – You have this house, and – You have net worth of $250,000. 40 • Owning the house does not mean that you are worth $250,000. – If you borrowed the $250,000 purchase price from your parents. • You are not worth $250,000. – You have an asset worth $250,000 and – You have a liability for $250,000. – You have zero net worth. 41 • What if you have no assets or liabilities. – You have a zero net worth. • But, you have a credit card & get a cash advance of $10,000. – Are you richer than before cash advance? • You have $10,000 in cash • You have a $10,000 debt • You still have a zero net worth. 42 • In order to give full disclosure - report your – Assets, – Liabilities and – Net Worth • Equity 43 • Balance Sheet provide this disclosure – Gives information regarding a firm's assets, liabilities and equity. • Firm's assets are paid for with either – Liabilities or – Equity. • Because of this relationship: – Firm's assets = Firm’s liabilities + Firm’s equity. – This relationship is called “Balance Sheet Equation” 44 The Balance Sheet Equation is reflected in the Balance Sheet: Balance Sheet Assets Liabilities Owner's Equity Balance Sheets different formats Left-Right Top-Bottom 45 • Accounts – Each asset, liability and equity item is represented by an account – Flexibility in the names given to accounts. – Each account has two sides • just like the Balance Sheet • Left-hand side is the debit side • Right-hand side is the credit side – Example – firm has one asset account for Cash 46 • Example – firm has one asset account for Cash Cash Debits Credits • Debits and credits are netted to give the balance in the account. • Accounts are kept in the General Ledger of Accounts 47 • Balance Sheet – Summarizes the assets, liabilities and equity accounts • If account is on the left-hand side of the Balance Sheet – Asset – Account will normally (not always) have debit balance. • If an account is on the right-hand side of the Balance Sheet – Liabilities and equity – Account will normally have credit balance. 48 • When account has debit balance – E.g., asset – Increase - debit it some more • Add to the debit balance. – Decrease - credit it • Adding to the opposite side • Two sides netted • Thereby decreasing that balance. Cash 1000 100 1100 49 • When account has a credit balance – E.g., a liability or equity account – Increase - credit it some more – Decrease - debit it Accounts Payable 1000 100 1100 50 • Order of accounts on Balance Sheet follows convention. – Assets listed by how soon they will be converted into cash. • Current Assets listed first – Cash is the first line – Assets that will be used, consumed or collected within one year or business cycle, whichever is longer • Non-current Assets listed second – Used, consumed or collected after one year or business cycle 51 – Liabilities listed by how soon they will be paid. • Current Liabilities listed first – Will be paid within one year or business cycle • Non-current Liabilities listed second – Will be paid after one year or business cycle – Equity accounts are listed by their priority of payment upon liquidation. – Business cycle • Time it takes to start and complete a business transaction 52 • Business transactions are recorded in accounts. • Changes to accounts summarized in the General Journal. – General Journal notes • which accounts are credited and • which accounts are debited. These General Journal entries take the following form: 53 • General Journal entries take the following form: D. Name of the Account Debited Cr. Name of the Account Credited $ XXX $XXX 54 • ILLUSTRATIONS 55 • Our firm is a corporation. • Equity in the corporation represented by capital stock. • There are different types of stock. – Common Stock • Residual Owners of Corporations • Get what’s left when creditors are paid 56 • When corporation sells stock – it increases its equity. – Cash (or other property) is given to the corporation • assets (e.g., cash) have increased – Cash did not come from debt. • Equity is thereby increased. – The equity account here is Common Stock. 57 • $100,000 of common stock is sold. – Two things happen with each transaction. – Here: • Cash went up, and • Equity went up. Cash Balance Sheet UP Common Stock $100,000 UP $100,000 58 • Cash – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Cash? (Debit or Credit) • Common Stock. – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Common Stock? (Debit or Credit) 59 • Cash – – – – Is an asset Assets are on left side of Balance Sheet Left Side means left (debit) balance To increase a debit balance account – DEBIT IT • Common Stock – – – – Is an equity account Equity is on the right side of Balance Sheet Right Side means right (credit) balance To increase a credit balance account – CREDIT IT 60 D. Cash $100,000 Cr. Common Stock Cash $100,000 $100,000 Common Stock $100,000 61 Balance Sheet Assets Cash Liabilities $100,000 Equity Common Stock $100,000 $100,000 $100,000 62 • Purchase of Equipment for $5,000 cash – Two things happen with each transaction. – Here: • Equipment went up, and • Cash went down. Cash Equipment Balance Sheet Down $5,000 Up $5,000 63 • Equipment – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Equipment? (Debit or Credit) • Cash – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you decrease Cash? (Debit or Credit) 64 • Equipment – – – – Is an asset Assets are on left side of Balance Sheet Left Side means left (debit) balance To increase a debit balance account – DEBIT IT • Cash – – – – Is an asset Assets are on the left side of Balance Sheet Left Side means left (debit) balance To decrease a debit balance account – CREDIT IT 65 D. Equipment $5,000 Cr. Cash Equipment $5,000 $5,000 Cash $100,000 $5,000 66 Balance Sheet Assets Cash Equipment Liabilities $95,000 $5,000 Equity Common Stock $100,000 $100,000 $100,000 67 • Purchase of Equipment in exchange for a promissory note for $10,000 – Two things happen with each transaction. – Here: • Equipment went up, and • Notes Payable went up. Equipment Balance Sheet Up Notes Payable $10,000 UP $10,000 68 • Equipment – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Equipment? (Debit or Credit) • Notes Payable – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Notes Payable? (Debit or Credit) 69 • Equipment – – – – Is an asset Assets are on left side of Balance Sheet Left Side means left (debit) balance To increase a debit balance account – DEBIT IT • Notes Payable – – – – Is a liability Liabilities are on the right side of Balance Sheet Right Side means right (credit) balance To increase a debit balance account – CREDIT IT 70 D. Equipment Cr. Notes Payable Equipment $5,000 $10,000 $10,000 $10,000 Notes Payable $10,000 71 Balance Sheet Assets Cash Equipment Liabilities $95,000 Notes Payable $10,000 $15,000 Equity Common Stock $110,000 $100,000 $110,000 72 • Purchase of Supplies for $10,000 on credit (no formal promissory note is given) – Two things happen with each transaction. – Here: • Supplies went up, and • Accounts Payable went up. Supplies Balance Sheet Up Accounts Payable $10,000 UP $10,000 73 • Supplies – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Supplies? (Debit or Credit) • Accounts Payable – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Accounts Payable? (Debit or Credit) 74 • Supplies – – – – Is an asset Assets are on left side of Balance Sheet Left Side means left (debit) balance To increase a debit balance account – DEBIT IT • Accounts Payable – – – – Is a liability Liabilities are on the right side of Balance Sheet Right Side means right (credit) balance To increase a crebit balance account – CREDIT IT 75 D. Supplies Cr. Accounts Payable Supplies $10,000 $10,000 $10,000 Accounts Payable $10,000 76 Balance Sheet Assets Liabilities Cash $95,000 Accounts Payable Supplies Equipment $10,000 Notes Payable $15,000 Equity Common Stock $120,000 $10,000 $10,000 $100,000 $120,000 77 • Purchase of Land and Building for $100,000. – When you pay one price for a bundle of assets • Allocate the purchase price according to FMV. – Assume: • Land is worth $10,000 • Building is worth $90,000 • Price $100,000 is paid: – Cash ($20,000) and – Promissory note ($80,000). 78 • Purchase of Land and Buildings for $100,000 – Two things happen with each transaction. – Here: • Land & Buildings went up, and • Cash went down & Notes Payable went up. Cash Balance Sheet Down Notes Payable $20,000 Land Buildings Up $10,000 Up $90,000 UP $80,000 79 • Cash – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you decrease Cash? (Debit or Credit) • Land – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Land? (Debit or Credit) 80 • Buildings – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Buildings? (Debit or Credit) • Notes Payable – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Notes Payable? (Debit or Credit) 81 • Cash – – – – Is an asset Assets are on left side of Balance Sheet Left Side means left (debit) balance To decrease a debit balance account – CREDIT IT • Land – – – – Is an asset Assets are on left side of Balance Sheet Left Side means left (debit) balance To increase a debit balance account – DEBIT IT 82 • Buildings – – – – Is an asset Assets are on left side of Balance Sheet Left Side means left (debit) balance To increase a debit balance account – DEBIT IT • Notes Payable – – – – Is a liability Liabilities are on the right side of Balance Sheet Right Side means right (credit) balance To increase a debit balance account – CREDIT IT 83 D. Land Buildings $10,000 $90,000 Cr. Cash Notes Payable Land $10,000 $20,000 $80,000 Buildings $90,000 84 D. Land Buildings $10,000 $90,000 Cr. Cash Notes Payable $20,000 $80,000 Cash $100,000 Notes Payable $5,000 $10,000 $20,000 $80,000 85 Balance Sheet Assets Liabilities Cash $75,000 Accounts Payable Supplies Equipment Land Buildings $10,000 Notes Payable $15,000 $10,000 Equity $90,000 Common Stock $200,000 $10,000 $90,000 $100,000 $200,000 86 • Pay the principal of $6,000 on a promissory note – Two things happen with each transaction. – Here: • Cash went down, and • Notes Payable went down. Cash Balance Sheet Down Notes Payable Down $6,000 $6,000 87 • Cash – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you decrease Cash? (Debit or Credit) • Notes Payable – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you decrease Notes Payable? (Debit or Credit) 88 • Cash – – – – Is an asset Assets are on left side of Balance Sheet Left Side means left (debit) balance To decrease a debit balance account – CREDIT IT • Notes Payable – – – – Is a liability Liabilities are on the right side of Balance Sheet Right Side means right (credit) balance To decrease a credit balance account – DEBIT IT 89 D. Notes Payable Cr. Cash $6,000 $6,000 Cash $100,000 Notes Payable $5,000 $20,000 $6,000 $6,000 $10,000 $80,000 90 Balance Sheet Assets Liabilities Cash $69,000 Accounts Payable Supplies Equipment Land Buildings $10,000 Notes Payable $15,000 $10,000 Equity $90,000 Common Stock $194,000 $10,000 $84,000 $100,000 $194,000 91 • Income Statement – Equity increased by: • Contributions from its owners (e.g., the sale of stock) – Contributed Capital. • Firm generating profits from its operations – If the firm distributes those profits to stockholders – dividends – If firm keeps profits - Retained Earnings. 92 • Profits reflected in accounts – Inflows reflected in revenue accounts – Outflows reflected in expense accounts. • Revenues less expenses give you the firm's Net Income. • Income Statement summarizes these revenue & expense accounts 93 • Revenues – CD defines as “the amount of inflowing assets from the sale or providing of goods or services to customers. 94 • Revenues – Increase a firm's equity or net worth. • Equity appears on the right-hand side of the Balance Sheet – It normally has a credit (right) balance – Increased with a credit – Decreased with a debit • Because revenues increase equity – Revenues will normally have a credit (right) balance. • Because expenses decrease equity – Expenses will normally have a debit (left) balance. 95 • Illustration Continued 96 • Our firm earns consulting commissions of $50,000. The client has not yet paid these commissions – Two things happen with each transaction. – Here: • Consulting Revenue went up (Retained Earnings Up), and • Accounts Receivable went up. Accounts Receivable Balance Sheet Up Retained Earnings $50,000 Up $50,000 97 • Accounts Receivable – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Accounts Receivable? (Debit or Credit) • Consulting Revenue – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Consulting Revenue? (Debit or Credit) 98 • Accounts Receivable – – – – Is an asset Assets are on left side of Balance Sheet Left Side means left (debit) balance To increase a debit balance account – DEBIT IT • Consulting Revenue – Is a Revenue Account – Revenues increase Equity – Equity accounts are on the right side of Balance Sheet – Right Side means right (credit) balance – To increase a credit balance account – CREDIT IT 99 D. Accounts Receivable Cr. Consulting Revenue $50,000 Accounts Receivable Consulting Revenue $50,000 $50,000 $50,000 100 Balance Sheet Assets Liabilities Cash $69,000 Accounts Payable Accounts Rec. Supplies Equipment Land Buildings $50,000 $10,000 $15,000 $10,000 $90,000 $244,000 Notes Payable Equity Common Stock $10,000 $84,000 $100,000 Retained Earnings $50,000 $244,000 101 • The firm pays salaries of $20,000 – Two things happen with each transaction. – Here: • Salary Expense went up (Retained Earnings Down), and • Cash went down Cash Balance Sheet Down Retained Earnings $20,000 Down $20,000 102 • Cash – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you decrease Cash? (Debit or Credit) • Salary Expense – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Salary Expense? (Debit or Credit) 103 • Cash – – – – Is an asset Assets are on left side of Balance Sheet Left Side means left (debit) balance To decrease a debit balance account – CREDIT IT • Salary Expense – Is an Expense – Expenses decrease Equity – Equity accounts are on the right side of Balance Sheet – Right Side means right (credit) balance – To decrease a credit balance account – DEBIT IT 104 D. Salary Expense Cr. Cash $20,000 $20,000 Cash $100,000 Salary Expense $5,000 $20,000 $6,000 $20,000 $20,000 105 Balance Sheet Assets Liabilities Cash $49,000 Accounts Payable Accounts Rec. Supplies Equipment Land Buildings $50,000 $10,000 $15,000 $10,000 $90,000 $224,000 Notes Payable Equity Common Stock $10,000 $84,000 $100,000 Retained Earnings $30,000 $224,000 106 • The firm uses $3,000 of its supplies – Two things happen with each transaction. – Here: • Supplies Expense went up (Retained Earnings Down), and • Supplies went down Supplies Balance Sheet Down Retained Earnings Down $3,000 $3,000 107 • Supplies – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you decrease Supplies? (Debit or Credit) • Supplies Expense – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Supplies Expense? (Debit or Credit) 108 • Supplies – – – – Is an asset Assets are on left side of Balance Sheet Left Side means left (debit) balance To decrease a debit balance account – CREDIT IT • Supplies Expense – Is an Expense – Expenses decrease Equity – Equity accounts are on the right side of Balance Sheet – Right Side means right (credit) balance – To decrease a credit balance account – DEBIT IT 109 D. Supplies Expense Cr. Supplies $3,000 $3,000 Supplies $10,000 Salary Expense $3,000 $3,000 110 Balance Sheet Assets Liabilities Cash $49,000 Accounts Payable Accounts Rec. Supplies Equipment Land Buildings $50,000 $7,000 $15,000 $10,000 $90,000 $221,000 Notes Payable Equity Common Stock $10,000 $84,000 $100,000 Retained Earnings $27,000 $221,000 111 • The firm owes one month’s rent – Two things happen with each transaction. – Here: • Rent Expense went up (Retained Earnings Down), and • Rent Payable went up Balance Sheet Rent Payable Up $10,000 Retained Earnings Down $3,000 112 • Rent Payable – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Rent Payable? (Debit or Credit) • Rent Expense – What kind of account is it? – On what side of Balance Sheet is it located? – What kind of balance does this account normally have? – How do you increase Rent Expense? (Debit or Credit) 113 • Rent Payable – – – – Is a liability Liabilities are on right side of Balance Sheet Right Side means right (credit) balance To increase a credit balance account – CREDIT IT • Rent Expense – Is an Expense – Expenses decrease Equity – Equity accounts are on the right side of Balance Sheet – Right Side means right (credit) balance – To decrease a credit balance account – DEBIT IT 114 D. Rent Expense Cr. Rent Payable $5,000 $5,000 Rent Payable Rent Expense $5,000 $5,000 115 Balance Sheet Assets Liabilities Cash $49,000 Accounts Payable Accounts Rec. Supplies Equipment Land Buildings $50,000 $7,000 $15,000 $10,000 $90,000 $221,000 $10,000 Rent Payable $5,000 Notes Payable $84,000 Equity Common Stock $100,000 Retained Earnings $22,000 $221,000 116 • Trial Balance – At the end of the accounting period – Done to help in locating errors – Total all accounts with debit balances – Total all accounts with credit balances – The totals should equal – A number of trial balances are conducted during the accounting cycle. 117 Cash Trial Balance $49,000 Accounts Payable Accounts Rec. Supplies Equipment $50,000 Rent Payable $7,000 Notes Payable $15,000 Common Stock $5,000 $84,000 $100,000 Land Buildings Salary Expense Supplies Exp. $10,000 Consulting Rev. $90,000 $20,000 $3,000 $50,000 Rent Expense $5,000 $249,000 $10,000 $249,000 118 • Closing Entries – Have to reflect the revenues and expenses in Retained Earnings – Close revenue and expense accounts to the Income Summary account. – Then close Income Summary to Retained Earnings 119 • Close Consulting Revenue to Income Summary D. Consulting Revenue Cr. Income Summary Consulting Revenue $50,000 $50,000 $50,000 $5,000 Income Summary $50,000 120 • Close Salary Expense to Income Summary D. Income Summary Cr. Salary Expense Salary Expense $20,000 $20,000 $20,000 $20,000 Income Summary $20,000 $50,000 121 • Close Supplies Expense to Income Summary D. Income Summary Cr. Supplies Expense Salary Expense $3,000 $3,000 $3,000 Income Summary $3,000 $20,000 $3,000 $50,000 122 • Close Rent Expense to Income Summary D. Income Summary Cr. Rent Expense $5,000 $5,000 Rent Expense $5,000 Income Summary $5,000 $20,000 $3,000 $5,000 $50,000 123 • Close Income Summary to Retained Earnings D. Income Summary Cr. Retained Earnings Retained Earnings $22,000 $22,000 $22,000 Income Summary $20,000 $50,000 $3,000 $5,000 $22,000 $22,000