Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

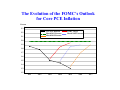

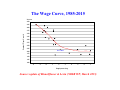

Discussion of “Monetary Policy, Incomplete Information, and the Zero Lower Bound” Andrew Levin Dartmouth College and NBER November 2015 The views expressed herein are solely my own responsibility and should not be attributed to any other person or institution. General Comments ● Important and timely topic: risk management at the ZLB ● Clear analytical framework: stylized New Keynesian model ● Rigorous solution method: parametrized expectations ● Sensible policy implications: uncertainty about the strength of aggregate demand warrants caution in determining the timing of liftoff from the ZLB Items for Discussion ● Intuition for key finding ● Magnitude of practical implications ● Robustness to model extensions The Driving Analogy ● Perfect Foresight: driving a familiar car on a flat rural highway with well-maintained pavement, approaching a stop sign that is clearly visible at a considerable distance. ==> Start applying the brakes well in advance and slow down gradually so that the car comes to a smooth stop. ● Imperfect Information: driving an unfamiliar vehicle up a steep country road that has lots of curves and some muddy conditions, with a stop sign located at the top of the hill that is not yet visible. ==> Be careful to preserve momentum and be mindful that the accelerator will be useless if the car gets stuck in the mud. The Evolution of the FOMC’s Outlook for Real GDP Growth Percent Actual GDP (4-quarter chg.) Nov. 2010 SEP Nov. 2011 SEP Mar. 2014 SEP Mar. 2015 SEP Average Rate (2010-2014) Longer-Run Normal Rate 5.0 4.5 4.0 3.5 3.0 2.5 2.0 1.5 1.0 2010 2011 2012 2013 2014 2015 2016 The Evolution of the FOMC’s Outlook for Core PCE Inflation Percent 2.3 Core PCE Inflation March 2013 Forecast March 2015 Forecast 2.2 2.1 FOMC Target March 2014 Forecast 2.0 1.9 1.8 1.7 1.6 1.5 1.4 1.3 1.2 2011 2012 2013 2014 2015 2016 2017 Professional Forecasters’ Assessments of the Equilibrium Real Interest Rate Percent 3.00 Blue Chip Consensus Interquartile Range 2.75 2.50 2.25 2.00 1.75 1.50 1.25 1.00 0.75 0.50 0.25 0.00 2007 2008 2009 2010 2011 2012 2013 2014 2015 Source: Blue Chip Economic Indicators. Copyright (c) Aspen Publishers Two Approaches for Determining the Appropriate Stance of Monetary Policy ● Forecast Targeting: A specific macroeconomic model (usually with judgmental adjustments) is used to determine the policy path that is expected to generate the most appropriate outcomes for real economic activity and inflation over the forecast horizon. ● Simple Policy Benchmarks: A range of plausible macro models (along with lessons from practical experience) are used to identify simple benchmarks—such as variants of the Taylor Rule—that generate robust outcomes for economic activity and inflation. Each approach has distinct merits and pitfalls, and hence both approaches should inform the actual conduct of monetary policy. Assessing Monetary Policy Implications using Simple Benchmarks CBO Output Gap (2015:Q3) = -3.1 percent Core PCE Inflation (12-mo. chg.) = 1.3 percent Taylor Rule “Balanced Approach” Rule (cf. Taylor 1999) Fixed R* 1.4 -0.2 Time-Varying R* 0.4 -1.2 Average Hourly Earnings of Production & Nonsupervisory Workers Percent 7 3-month Change 12-month Change 6 5 4 3 2 1 0 -1 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 The Wage Curve, 1985-2015 Percent 4.50 4.25 4.00 3.75 Nominal Wage Growth 3.50 3.25 3.00 2.75 2.50 2.25 Nov. 2015 2.00 1.75 1.50 1.25 1.00 -2 -1 0 1 2 3 4 5 6 7 Employment Gap Source: update of Blanchflower & Levin (NBER WP, March 2015)