Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

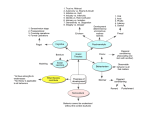

Chapter - 1 ACCOUNTING THEORY AND STANDARDS Dr. BALAMURUGAN MUTHURAMAN A THEORY: DEFINITION A theory: ‘a set of interrelated constructs (concepts), definitions, and propositions that present a systematic view of the phenomenon by specifying relationships among variables with the purpose of explaining and predicting the phenomenon’ A theory includes propositions linking concepts in the form of hypotheses to be tested. A THEORY: DEFINITION Elements of a theory include: ◦ Concepts: the main units of a theory and it is devised to refer to identifiable characteristics or phenomena. : The better the concept, the better the theory. : A formation of concept starts from the idea or percept generating a concept designated by terms. A THEORY: DEFINITION Elements of a theory include: ◦ Propositions: Establish relation between the concepts of a theory. : Designated by a sentence. : Characterized by 1) The number and degree predicates; and 2) The degree of generality. of A THEORY: DEFINITION Elements of a theory include: ◦ Hypotheses: a proposition about a relationship whose truth or falsity is yet to be determined by an empirical test. : Confirmation of a theory is the extent to which a hypothesis is capable of being shown to be empirically true, that is, of describing the real world accurately : Falsification?? ACCOUNTING THEORY MEANING “. . . a set of basic concepts and assumptions and related principles that explain and guide the accountant’s actions in identifying, measuring, and communicating economic information.” WHY ACCOUNTING THEORY IS IMPORTANT Many individuals have to make decisions about external accounting reports. ◦ ◦ ◦ ◦ ◦ Corporate managers Public accountants Officers of lending institutions Investors and financial analysts Individuals in accounting standard-setting bodies STRUCTURE OF ACCOUNTING THEORY FORMAL APPROACH RULES PRINCIPLES ASSUMPTIONS Accounting theory provides a logical framework for accounting practice. FUNCTIONS OF A THEORY Descriptive function: using the constructs or concepts and their relationships so as to provide the best explanation of a given phenomenon and the forces underlying it. Delimiting function: selecting the favorite set of events to be explained and assigning a meaning to the formulated abstractions of the descriptive stage. FUNCTIONS OF A THEORY Generative Function: the ability to generate testable hypotheses or to provide hunches, notions, and ideas from which hypotheses could be developed. Integrative Function: the ability to present a coherent and consistent integration of the various concepts and relations of a theory. ACCOUNTING THEORY: DEFINITION Accounting theory: principles that: A set of broad 1) provides a general frame of reference by which accounting practice can be evaluated; and 2) guides the development of new practices and procedures. ACCOUNTING THEORY: DEFINITION Accounting theory should explain and predict accounting phenomena. The primary objective of accounting theory is to provide a basis for the prediction and explanation of accounting behaviour and events. ACCOUNTING THEORY: DEFINITION Accounting theory should have Three elements: 1) Encoding of phenomena to symbolic representation; 2) Manipulation or combination according to rules; and 3) Translation phenomena. back to real-world A ROLE OF ACCOUNTING THEORIES Accounting Theories A Conceptual Framework Accounting Principles, Concepts and Postulates Accounting Techniques GAAP Accounting Standards Accounting Policies GAAP GAAP (Generally Accepted Accounting Principles): a guide to the accounting profession in the choice of accounting techniques and the preparation of financial statements in a way considered to be good accounting practice. GAAP Conditions under which an accounting method will be deemed as generally accepted: ◦ The method will be in actual use; ◦ The method would have support in the pronouncement of the professional accounting societies; ◦ The method would have support in the writing of a number of respected accounting teachers and thinkers. ACCOUNTING STANDARDS What are the differences between GAAP and accounting standards??? ACCOUNTING STANDARDS Accounting standards consist of Three parts: ◦ A description of the problem to be tackled. ◦ A reasoned discussion or ways of solving the problems. ◦ In line with discussion or theory, the prescribed solution. ACCOUNTING STANDARDS Reasons to establish standards are: ◦ To ensure quality of financial information ◦ To be guidelines and rules ◦ To be database for a government ◦ To generate interests in principles and theories. ACCOUNTING STANDARDS Who should standards? set accounting ◦ Theories of regulation: Public-interest theories Interest-group or capture theories The political regulation ruling-elite theory The economic theory of regulation of ACCOUNTING POLICIES The specific accounting principles and the methods of applying those principles that are judged by the management of the entity to be the most appropriate in the circumstances to present fairly financial position, changes in financial position, and results of operations in accordance with generally accepted accounting principles.