Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Investor-state dispute settlement wikipedia , lookup

Financialization wikipedia , lookup

International investment agreement wikipedia , lookup

Early history of private equity wikipedia , lookup

Investment management wikipedia , lookup

Balance of payments wikipedia , lookup

History of investment banking in the United States wikipedia , lookup

1998–2002 Argentine great depression wikipedia , lookup

Investment banking wikipedia , lookup

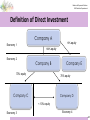

Balance of Payments Division IMF Statistics Department Implementation of BPM6 Recommendations on International Transactions in Services and Foreign Direct Investment Seminar on the Implementation of the International Statistical Standards in the Financial Statistics of Eurasian Economic Union (EAEU) Dilijan, Armenia May 31-June 3, 2016 Reproductions of this material, or any parts of it, should refer to the IMF Statistics Department as the source. Balance of Payments Division IMF Statistics Department Outline What are services? Classification of services and data sources • Manufacturing services on physical inputs owned by others • Maintenance and repair • Transport • Travel • Construction • Insurance • Charge for use of intellectual property • Financial services • Telecommunication, computer, and information services • Other business services • Government goods and services n.i.e. 2 Balance of Payments Division IMF Statistics Department What Are Services? Results of the production process that: • change the condition of the consuming units • • • Changes in the condition of the consumer’s goods: the producer works directly on goods owned by the consumer by transporting, cleaning, repairing or otherwise transforming them Changes in the physical condition of persons: the producer transports the persons, provides them with accommodation, provides them with medical or surgical treatments, improves their appearance, etc. Changes in the mental condition of persons: the producer provides education, information, advice, entertainment or similar services in a face to face manner. facilitate the exchange of products or financial assets not generally separate items over which ownership rights can be established Cannot generally be separated from their production 3 Balance of Payments Division IMF Statistics Department Services Classification Type of Service Manufacturing services on physical inputs owned by others Product-based Maintenance and repair services, n.i.e. Product-based Travel Transactor-based Transport Product-based Construction Transactor-based Insurance and pension services Product-based Financial services Product-based Charges for the use of intellectual property, n.i.e. Product-based Telecommunications, computer, and information services Product-based Other business services Product-based Personal, cultural and educational services Product-based Government goods and services, n.i.e. Transactor-based 4 Balance of Payments Division IMF Statistics Department Manufacturing Services on Physical Inputs Owned by Others In BPM6, Manufacturing services on physical inputs owned by others are recorded in services if the goods do not change ownership (change from BPM5) Significant impact for some countries with specialized manufacturing activities: the value of flows of goods are likely to be significantly reduced, while the flows in services will increase with BPM6 Covers processing, assembly, labeling, packing, etc. undertaken by enterprises that do not own the goods concerned Covers the transaction between the owner and the processor—only the fees for the service are included in this item • Examples: oil refining, clothing and electronic assembly, other assembly, labeling, packing Excludes: assembly of prefabricated construction and packing activities incidental to transportation 5 Balance of Payments Division IMF Statistics Department Manufacturing Services on Physical Inputs Owned by Others – Recording of Related Transactions Export of processing services (inward processing), Resident = processor (contractor) Inward processing (Export of processing services) 1 2 3 4 IMTS Recording (processor’s territory) BOP/NA Recording (processor’s economy Import Export Debit Credit Goods received by resident processor for Import of Export of Service: Processing processing. Transformed goods leave goods for processe fee processor’s economy once processed processing d goods Goods received by resident processor. Goods: Import of Transformed goods are purchased by Purchase of Service: Processing goods for residents of processor’s economy once processed fee processing processed goods Goods purchased by non-resident principal Service: Processing Goods: in the resident processor’s economy fee Purchase of Transformed goods are purchased by Goods: Sales of processed residents of processor’s economy once goods (input) to nongoods processed resident principal Service: Processing Goods purchased by non-resident principal Export of fee in the resident processor’s economy processe Goods: Sales of Transformed goods leave processor’s d goods goods (input) to noneconomy once processed resident principal 6 Balance of Payments Division IMF Statistics Department Example 1: Manufacturing Services on Physical Inputs Owned by Others Merchandise with manufacturing services that change the condition of the goods A resident of A acquires oil from country B for 10. The oil is sent to country C for refining for 15. The oil is sold then to country D for 30. Goods and services entries for country A: general merchandise (with country B): 10 (debit) general merchandise (with country D): 30 (credit) Manufacturing services on physical inputs owned by others (with country C): 15 (debit) Country C may wish to consider providing supplementary items on goods received for processing and goods sent after processing 7 Balance of Payments Division IMF Statistics Department Maintenance and Repair Services n.i.e. Now included under services rather than goods Covers maintenance and repair work undertaken by residents on goods owned by nonresidents. Includes value of repair work (including parts and materials supplied by repairer) Does not include the value of goods for repair Data collection: enterprise survey or ITRS Excludes: • Construction repair and maintenance • Maintenance and repair of computers 8 Balance of Payments Division IMF Statistics Department Transport Services: Coverage Transport services includes: services provided by all modes of transport performed by residents of economy for those of another carriage of passengers and the movement of goods (freight) as well as rentals (charters) of carriers with crew supporting and auxiliary services: cargo handling, navigation fees and maintenance and cleaning of carriers postal and courier services cover the pick-up, transport, and delivery of letters, newspapers etc., including post office counter and mailbox rental services 9 Balance of Payments Division IMF Statistics Department Transport Services: Classification By what is carried Passenger Freight Other By mode of transport Sea Transport Air Transport Other Transport Postal and Courier Services Other transport: • Additional modes such as Space Rail Road Inland waterway Pipeline transport and electricity transmission 10 Balance of Payments Division IMF Statistics Department Passenger Services All services provided, between the compiling economy and abroad or between two foreign economies, in the international transport of: • • Nonresidents by residents carriers (credit); and Residents by nonresident carriers (debit) Fares and other expenditure related to the carriage of passengers: • • • • • • On-board food, gifts, souvenirs Excess baggage charges Accompanying personal effects, including autos Any taxes levied on passenger services e.g., sales taxes or value added taxes For practical reasons fares that are part of package tours are included, but exclude cruise fares which are included in travel Covers rentals or operational leases of vessels, aircraft, freight cars, or other commercial vehicles with crews for limited periods for the carriage of passengers 11 Balance of Payments Division IMF Statistics Department Freight Services The treatment of freight services is a consequence of adopting FOB as the uniform valuation principle for goods as discussed in previous lecture on goods Since the FOB valuation is as at the customs frontier of the exporting economy, so: • • all freight costs up to the customs frontier are shown as incurred by the exporter; all freight costs beyond the customs frontier are shown as incurred by the importer However, the arrangements for paying freight costs may differ from the FOB terms of delivery -> rerouting is needed Rerouting of freight services may mean that a transaction that is actually between two residents is treated as a transaction between a resident and a nonresident and vice versa 12 Balance of Payments Division IMF Statistics Department Other Transport “Other” subheading under sea and air includes: Cargo handling charged billed separately from freight Storage and warehousing Packing and repackaging Towing not included in freight services Pilotage and other navigational aid for carriers Air traffic control Cleaning in ports and airports on transport equipment Salvage operations Agent fees associated with passenger and freight transport (freight forwarding, handling and brokerage services) 13 Balance of Payments Division IMF Statistics Department Transport: Data Sources Data sources for transport services are presented in Table 12.1 of BPM6 CG For exports • • • Enterprise surveys ITRS A data model could be developed base don available information (e.g., number of passengers transported, number of tickets sold, etc.) For imports • ITRS if provides breakdown of import costs • Survey of branches of nonresident transport operators • A data model based on related information could be used Survey of companies that provide postal and courier services 14 Balance of Payments Division IMF Statistics Department Travel Travel credits cover goods and services for own use or to give away, acquired from an economy by nonresidents during visits to that economy Travel debits cover goods and services for own use or to give away acquired from other economies by residents during visits to other economies The standard component breakdown of travel is between business and personal travel Supplementary data for groups of special interest e.g. border, seasonal, and other short-term workers within business travel, health-related and education-related under personal travel 15 Balance of Payments Division IMF Statistics Department Travel A demand oriented activity; travelers moves to the location of the provider (residents of the economy visited) for the goods and services desired Travel covers an assortment of services, consumed by travelers It is a transactor-based classification • Goods and services provided to visitors while on their trips that would otherwise be classified under another item (such as telecommunications or local transport) are included under travel Travel covers goods and services acquired in an economy by travelers during visits of less than ONE year in the economy 16 Balance of Payments Division IMF Statistics Department Personal Travel Business travel - travelers going abroad for business Carrier crews stopping over (but in-flight, or shipboard expenses incurred by resident crew on resident carrier not included) Government employees on official travel Employees of international organizations on official business Employees travelling on behalf of their employer (except for diplomatic staff, etc.) Self- employed nonresidents travelling for business purposes Seasonal, border, and other short term workers Personal travel - travelers going abroad for purposes other than business 17 Balance of Payments Division IMF Statistics Department Travel: Data Sources Data sources for travel services and estimations for travel component are presented in Table 12.3 of BPM6 CG Types of approaches for estimations Instruments used to measure expenditures by residents traveling abroad Expenditures by type of goods and services acquired by residents traveling abroad Partner economy data Data model Data sources ITRS Surveys of travelers Surveys of tourism companies, hotels, domestic airlines, etc. 18 Balance of Payments Division IMF Statistics Department Construction Covers goods and services related to construction • work done on buildings, land improvement, engineering, as as well as construction installation and assembly Work provided outside the country of residence of the enterprise performing the work • However, if the operations are substantial, may constitute a resident branch in country Comprises work performed on construction projects by an enterprise or site office that is nonresident in the host country Generally the work is of a short-term nature (note the one year guideline for residence) The value of the construction service should equal the full value of the construction project (output) Gross value of output: value of all goods and services used as inputs to the work, other costs of production, and the operating surplus that accrues to the owners of the construction enterprise 19 Balance of Payments Division IMF Statistics Department Construction • Disaggregated and recorded on a gross basis Allows for recording of both construction work in host and goods and services acquired Construction abroad Credit—construction work abroad by enterprises resident in compiling economy Debit—goods and services acquired from host economy by resident construction enterprises Construction in compiling economy Credit—goods and services acquired from compiling economy by nonresident construction enterprises Debit—construction work in compiling economy by nonresident construction enterprises 20 Balance of Payments Division IMF Statistics Department Nonlife Insurance: Measurement of Output /Insurance Services Insurance company sets level of actual premiums, so that • Premiums earned + investment income earned on them – expected • claims = margin that insurance company can retain -> to cover costs and provide operating surplus In order to “mimic” the premium setting policy of insurance companies we have to identify five separate items: • premiums earned • premium supplements • expected claims claims payable (adjusted for claims volatility, if needed) • insurance technical reserves 21 Balance of Payments Division IMF Statistics Department Nonlife Insurance: Measurement of Output /Insurance Services Gross premiums earned: • proportion of actual premiums, relating to the accounting period • cover the risks incurred during the accounting period • differ from premiums received, as they are usually paid in advance • (credit extended by the policyholder to insurance company, i.e. unearned premiums) Claims payable/incurred: • claims for events that occurred during the accounting period • claims that have not been reported have been reported but not yet settled have been reported and settled but not yet paid … recognized as due on an accrual basis, whether or not paid, settled or reported. 22 Balance of Payments Division IMF Statistics Department Nonlife Insurance: Measurement of Output /Insurance Services Adjustments for claims volatility: • In case of a significant unforeseeable event during the accounting period, the derived insurance services rendered by the insurance company to the policyholders should not turn into a negative figure • i.e., neither the volume nor the price of insurance services should be affected by the volatility of claims to reflect a longer term view of claims behavior The adjustment would be negative in periods when large values of claims are incurred • thus increasing the value of the service by reducing the difference between actual claims in a particular period and a normally expected level of claims 23 Balance of Payments Division IMF Statistics Department Nonlife Insurance: Measurement of Output /Insurance Services Reserves in insurance: • Unearned premium reserves are that part of premiums written that apply to the unexpired part of the policy period plus • Estimated loss reserves and reserves for claims incurred but not reported are provisions set aside to meet the estimated costs of settling claims Premium supplements: • as part of the business of insurance companies, these reserves are • • managed on the financial markets the income generated by these investments have a considerable influence on the level of premiums that these companies have to charge consequently, the income earned is treated as being receivable by the policyholders who are then treated as paying it back to the insurance companies as premium supplements (=imputation) 24 Balance of Payments Division IMF Statistics Department Example 2: Calculation of Nonlife Insurance Services Resident insurers: Premiums earned from abroad 100 (premiums received 105) Claims payable abroad 140 (claims paid 130) Net increase in technical reserves relating to insurance with nonresidents due to prepayment 5 Net increase in technical reserves relating to insurance with nonresidents due to claims incurred but not yet paid 10 Income attributable to policyholders 5 (premium supplements) Adjustment for volatility in claims payable:- 40 25 Balance of Payments Division IMF Statistics Department Example 2: Calculation of Nonlife Insurance Services Derived items for the BOP Goods and services account: • insurance services= gross premiums earned + premium supplements - expected claims (actual claims payable plus adjustment for claim volatility) • expected long-term claims: claims payable – adjustment: 140 – 40 = 100 • 100 + 5 – 100 = 5 Primary income account: • • investment income attributable to policyholder (premium supplements) =5 26 Balance of Payments Division IMF Statistics Department Insurance Services: Data Collection Data requests from resident insurers with separate data on policyholders abroad: • • • • • premiums earned (pre-payments) and premiums received/written in a period claims payable/due and claims paid in a period level of technical reserves due to nonresident policyholders at the start of the period level of technical reserves due to nonresident policyholders at the end of the period income from technical reserves due to non-resident policyholders in the period If precise data on transactions and positions with nonresidents are not available, to request the estimated ratio of nonresidents in total transactions and positions For import of insurance services (except reinsurance) data sources could be: • • ITRS Enterprise surveys See BPM6 CG: Appendix 3 and Model form 11 in Appendix 8 27 Balance of Payments Division IMF Statistics Department Charges for the Use of Intellectual Property n.i.e. Intellectual property products are largely the results of research and development, computer software and databases, and entertainment, literary or artistic originals BPM5: transactions included under “royalties and license fees” BPM6 includes: Charges for the use of franchise and trademarks, like in BPM5 Charges for the use of outcomes of R&D Licenses to reproduce, or distribute intellectual property embodied in Produced originals and prototypes (copyrights on books, manuscripts) Computer software Audiovisual and related services (cinematographic works, and sound recordings) Related rights (for live performances) 28 Balance of Payments Division IMF Statistics Department Charges for the Use of Intellectual Property n.i.e. Data collection: • • • Business surveys (payments recorded as license fees, royalties, other fees under license agreements, etc.) Other surveys (special surveys, within globalization survey) ITRS Recording should follow accrual principle and charges should be spread over period of use • In practice: may only be able to record when payments are made 29 Balance of Payments Division IMF Statistics Department Financial Services Services provided by financial intermediaries and auxiliaries (except those of insurance and pension funds). Charged through: i) Explicit charges • Charges associated with deposits and lending, commissions and brokerage fees, fees related to letters of credit, financial leasing, money transfer, foreign exchange transactions, etc. • Early/late repayment fees But excludes increase in interest rates as a result of late payment (considered with other interest – FISIM) • Financial market regulatory services • Service charges on purchases of IMF resources Charges payable for arranging the provision of financial resources are to be distinguished from amounts payable to the suppliers for the use of these financial resources (=primary income) 30 Balance of Payments Division IMF Statistics Department Financial Services ii) Margins on buying and selling transactions • • • Dealers in foreign exchange, bonds, notes, financial derivatives, etc. (BPM5 only included dealers in foreign exchange) Not distinguishable from underlying financial transactions Estimated charge to • • Seller—difference between reference price and dealer’s buying price Buyer—difference between reference price and dealer’s selling price Reference price—usually mid-point between buying and selling prices Some dealers may have their own internal price The service can also be measured by applying the dealer’s average margin as a percentage to the value of transactions through dealers Forex dealers often transact with one another In this case, there is no service charge 31 Balance of Payments Division IMF Statistics Department Financial Services iii) Asset management costs deducted from property income receivable (as in the case of asset-holding entities) • • • • Some entities have the sole or predominant function of holding financial assets on behalf of others (e.g., mutual funds, investment funds, holding companies, trusts, SPEs) Their expenses can be charge explicitly or implicitly paid out of investment income Without recognizing these costs, the asset management enterprises would have a negative operating surplus (=bankrupt) The counter-entry is to increase the net investment income receivable to the gross income, before deduction of the expenses Data sources: • ITRS or bank statements; surveys on external stocks of assets and liabilities may also collect the explicit fees on financial transactions 32 Balance of Payments Division IMF Statistics Department Financial Services iv) Margins between interest and the reference rate on loans and deposits: Financial Intermediation Services Indirectly Measured (FISIM) • • Change from BPM5 Actual “interest” includes element of income as well as charge for service • • Units not charged explicitly for service—hence need to be “indirectly measured” Interest margin used to defray cost of service and provide operating surplus Need to distinguish between pure interest charge (Primary income) and the service Actual interest (loans) =pure interest plus FISIM Important for debt sustainability analysis (recorded as memo item) 33 Balance of Payments Division IMF Statistics Department Telecommunications, Computer, and Information Services BPM6: New grouping of various items previously classified separately • • defined in terms of the nature of the service, not the method of delivery communications was a standard component in BPM5 Telecommunications services • Includes: transmission of sound, images, etc., by telephone, telex, cable, broadcasting, satellite, electronic mail, facsimile, teleconferencing, cellular telephone services 34 Balance of Payments Division IMF Statistics Department Telecommunications, Computer, and Information Services Computer Services Includes: hardware and software related services and data processing services (see list - para 10.143) Excludes: • • • • Charges for licenses to reproduce or distribute software Leasing of computers without an operator Computer training courses not designed for a specific user Noncustomized packaged software Information services • • • • News agency services such as the provision of news, photographs, and articles to the media Database services—database conception, data storage, and data dissemination Nonbulk subscriptions to newspapers, periodicals, etc. Library and archive services 35 Balance of Payments Division IMF Statistics Department Other Business Services Includes: • • • R&D Services Professional and management consultancy services Technical, trade-related, and other business services Research and development services (R&D) • In BPM5, considered nonproduced asset and these transactions were • included in the capital account BPM6: The results of R & D treated as produced assets (unlike BPM5) and so outright sale transactions in them (e.g., patents, copyrights, trademarks, industrial processes, and) included under this item 36 Balance of Payments Division IMF Statistics Department Other Business Services: Research and Development Covers services associated with research and experimental development of new products and processes (e.g.,in physical science, humanitarian, commercial research, etc) In practice, it may be difficult to differentiate the amounts payable for the sale of proprietary rights (R&D) from the use of proprietary rights (licenses to reproduce and licenses to use outcomes of R&D) • → charges for the use of intellectual property) Valuation at cost unless market value is observable 37 Balance of Payments Division IMF Statistics Department Other Business Services Professional and management services • Legal services, accounting, management consulting, managerial services, • • and public relations services; and Advertising, market research, and public opinion polling services Also: services for the general management of a branch, subsidiary, or associate provided by a parent enterprise or other affiliated enterprise Technical, trade related, and other business services • Includes agricultural, engineering, waste treatment and de-pollution, • operational leasing Trade-related services cover commissions on goods and service transactions payable to merchants, commodity brokers, dealers, auctioneers, and commission agents. Does not include merchanting (now included under goods) 38 Balance of Payments Division IMF Statistics Department Other Business Services: Operating Leasing Operating leasing (previously operational leasing in BPM5) • • • Renting of produced assets (buildings, machinery, equipment, etc.) but does not involve transfer of bulk of risks and benefits of ownership Leasing and charter of ships, aircraft, and transportation equipment (such as railway cars, containers), without operator or crew. Leases for other types of goods (e.g., dwellings and other buildings). are included in this item, if not included in travel 39 Balance of Payments Division IMF Statistics Department Government Goods and Services n.i.e. Residual category Goods and services supplied by and to enclaves, such as embassies, military bases, and international organizations • e.g., office supplies, vehicles, repairs, rental of premises, electricity Goods and services acquired from the host economy by diplomats, consular staff, and military personnel located abroad and their dependents • e.g., also when embassy staff sells his car at the end of his stay abroad (debit of local economy) Services supplied by and to governments and not included in other categories of services • • • Technical assistance to government and public administration, and when not classified to a specific service Payments for police-type services (such as keeping order) Issue of licenses to exercise some proper regulatory function (if not taxes) Excludes: Transactions of public enterprises 40 Balance of Payments Division IMF Statistics Department Direct Investment: Outline Introduction Definition of direct investment • • • Fellow enterprises Reverse investment Indirect direct investment Framework of direct investment relationship Valuation of direct investment Components of Direct Investment • Reinvested earnings Data collection • Surveys • Financial statements • Approval of foreign investment • Mirror data Assets/Liabilities vs Directional Principle 41 Balance of Payments Division IMF Statistics Department Introduction Direct investment is the first of the five functional categories of the financial account of the balance of payments and the corresponding international investment position statement Direct investment statistics embody 3 distinct statistical accounts: • • • Investment positions Financial transactions Associated income flows between enterprises which are related through a direct investment relationship International standards in DI are set out in IMF Balance of Payments Manual, 2009 (BPM6) and 4th Edition of the OECD Benchmark Definition of Foreign Direct Investment, 2008 (BD4) 42 Balance of Payments Division IMF Statistics Department Definition of Direct Investment Components Direct Investment in IIP Assets/Liabilities • Equity and investment fund shares • Direct investor in direct investment enterprises Direct investment enterprises in direct investor (reverse investment) Between fellow enterprises if ultimate controlling parent is resident if ultimate controlling parent is nonresident if ultimate controlling parent is unknown Debt instruments Direct investor in direct investment enterprises Direct investment enterprises in direct investor (reverse investment) Between fellow enterprises if ultimate controlling parent is resident if ultimate controlling parent is nonresident if ultimate controlling parent is unknown 43 Balance of Payments Division IMF Statistics Department Definition of Direct Investment Direct investment arises when an investor resident in one economy (direct investor) makes an investment that gives control or a significant degree of influence on the management of an enterprise (direct investment enterprise) that is resident in another economy • • Control is determined to exist if the investor owns more than 50% of the voting power in the enterprise that is resident in another economy A significant degree of influence is determined to exist if the investor owns from 10 to 50% of the voting power in the enterprise that is resident in another economy 10 percent rule 44 Balance of Payments Division IMF Statistics Department Definition of Direct Investment Direct Investor Direct Investment Enterprise (DIENT) • Is the entity or group of related entities that is able to exercise control or influence over another entity resident in another economy • Is the entity subject to control or influence •In some cases, an entity may be both a direct investor and a DIENT DIENTs can be either directly or indirectly owned by the direct investor, and comprise: Branches Subsidiaries (100 % ownership) (Over 50% ownership) the direct investor is able to exercise control the direct investor is able to exercise control Associates (10-50% ownership) the direct investor is able to exercise a significant degree of influence, but not control 45 Balance of Payments Division IMF Statistics Department Fellow Enterprises Fellow enterprises are: • enterprises under the control of the same direct investor (Company B and Company C share a common parent Company A) • neither fellow enterprise controls or influences the other fellow enterprise (that is neither holds 10% or more voting power in the other) - not enough or any voting power between Company B and Company C • residents in different economies Company A will be the ultimate controlling parent (UCP) Economy A 80% Economy B 70% Lend $250 m Economy C Liabilities- Direct investment – Debt Instruments – Between fellows – if UCP is nonresident (economy C) = outstanding loan $250mn provided by Company B to Company C 46 Balance of Payments Division IMF Statistics Department Definition of Direct Investment Company A 15% equity Economy 1 100% equity Economy 2 Company B 70% equity Company E 70% equity Company C Company D < 10% equity Economy 3 Economy 4 47 Balance of Payments Division IMF Statistics Department Definition of Direct Investment As well as the initial equity transaction that gives rise to control or influence, direct investment also includes all subsequent financial transactions and positions associated with this relationship, including: • • • • • transactions and positions between fellow enterprises, incorporated or unincorporated inter company debt (except debt of selected financial intermediaries) reverse investment reinvested earnings investment in indirectly influenced or controlled enterprises Enterprises in a direct investment relationship with each other are called affiliates or affiliated enterprises. 48 Balance of Payments Division IMF Statistics Department Reverse Investment Reverse Investment arises when a DIENT lends funds to or acquires equity in its immediate or indirect direct investor, provided it does not own equity of 10 per cent or more of the voting power in that direct investment Economy A Loan=US$200 5% equity (75 % equity) Example: Economy A’s IIP Liabilities Direct Investment, Debt Instruments, DIENT in direct investor (Reverse investment) = US$200 In contrast if two enterprises each have Economy B 10 per cent or more of the voting power in the other, there is no reverse investment, rather there are two mutual direct investment relationships 49 Balance of Payments Division IMF Statistics Department Mutual Direct Investment • Mutual direct investment: If Enterprise B has 10 percent or more of the voting power in an Enterprise A (which holds 10 percent or more of the voting power in Enterprise B), each is a DI in the other. That is, Enterprise B is both a DIENT of Enterprise A, and a DI in Enterprise A (Para 4.8 CDIS Guide). Company A Loan = US$100 Economy A $50 equity (50%) $70 equity (70%) Economy B Company B 50 Balance of Payments Division IMF Statistics Department Example 3: Mutual Direct Investment IIP: Direct Investment (Economy A) Assets Liabilities Equity and investment fund shares Direct investor in direct investment enterprises 70 50 DIE in direct investor (reverse investment) Between fellow enterprises Debt instruments Direct investor in direct investment enterprises 100 DIE in direct investor (reverse investment) Between fellow enterprises IIP: Direct Investment (Economy B) Assets Liabilities Equity and investment fund shares Direct investor in direct investment enterprises 50 70 DIE in direct investor (reverse investment) Between fellow enterprises Debt instruments Direct investor in direct investment enterprises 100 DIE in direct investor (reverse investment) Between fellow enterprises 51 Balance of Payments Division IMF Statistics Department Indirect Direct Investment Control or significant influence may be achieved: • directly by owning equity that gives voting power in the enterprise, • or indirectly by having voting power in another enterprise that has voting power in the enterprise Direct investment relationship extends indirectly through chains of ownership to the DIENT’s subsidiaries, subsidiaries and associates of subsidiaries, associates and subsidiaries of associates The Framework of Direct Investment Relationship (FDIR) is a generalized methodology for identifying and determining the extent and type of direct investment relationships 52 Balance of Payments Division IMF Statistics Department Framework for Direct Investment Relationships (FDIR) The principles for indirect transmission of control and influence through a chain of ownership are as follows: • • • Control can be passed down a chain of ownership as long as control exists at each stage. Influence can be generated at any point down a chain of control. Influence can be passed only through a chain of control but not beyond. 53 Balance of Payments Division IMF Statistics Department Framework for Direct Investment Relationships (FDIR) A Direct Investor 100% 40% G G Immediate associate B Immediate subsidiary 70% 30% C Subsidiary of A D Associate of A 80% E Associate of A 100% 25% × FF Not Affiliated with A H Associate of A 80% J Associate of A 20% × × II Not Affiliated with A 35% KK Not Affiliated with A 54 Balance of Payments Division IMF Statistics Department Valuation of Direct Investment Transactions and Positions BPM6 recommends that market values be used to value direct investment financial flows, income transactions and positions Why? • • If inconsistent valuation is used, comparison between DI in the BOP and IIP as well as with other financial investment will be difficult. Market valuation provides the most meaningful measure of the economic value of resources available to, or transferred between, economies. 55 Balance of Payments Division IMF Statistics Department Valuation of Direct Investment Transactions and Positions BPM6 proposes 6 alternative methods to value DI positions, when the market value is not readily available. The CDIS Guide 2015 favors the Own Funds at Book Value (OFBV) method for valuing unlisted (or unquoted) equity and other equity: OFBV = (a) paid-up capital + (b) all types of reserves in the balance sheet identified as equity + (c) cumulated reinvested earnings + (d) holding gains/losses 56 Balance of Payments Division IMF Statistics Department Components of Direct investment in Financial Account Direct investment position comprise two types of financing: (i) equity and investment fund shares, of which reinvestment of earnings and (ii) inter-company debt Equity Listed Equity: shares traded on an exchange Unlisted Equity: shares that are privately held Other Equity: not in the form of securities, can include equity in quasi-corporations such as branches, trusts, notional units Investment fund shares Debt instruments Collective investment undertakings through which investors pool funds for investment in financial or non financial assets or both Debt instruments are those instruments that require payment of principal and interest at some points in the future 57 Balance of Payments Division IMF Statistics Department Classification Structure: Components of Direct Investment (BOP and IIP) Direct investment NAFA (BOP) Assets (IIP) NIL (BOP) Liabilities (IIP) Equity and investment fund shares: Equity other than reinvestment of earnings (BOP)/ Equity and investment fund shares (IIP) Direct investor in direct investment enterprises (DIENT) DIENTs in direct investor (reverse investment) Between fellow enterprises if ultimate controlling parent is resident If ultimate controlling parent is nonresident If ultimate controlling parent is unknown Reinvestment of earnings (only in BOP) Debt instruments Direct investor in DIENT DIENTs in direct investor (reverse investment) Between fellow enterprises if ultimate controlling parent is resident If ultimate controlling parent is nonresident If ultimate controlling parent is unknown 58 Balance of Payments Division IMF Statistics Department Direct Investment Earnings Direct investment earnings measure earnings from current operations Direct investment earnings must be calculated before holding gains or losses Earnings of DIENTs reported using the Current Operating Performance Concept should exclude: • • • • • • • Gains or losses arising from valuation changes, disposal of assets or liabilities Gains or losses on assets from closure of all or part of business Write off of intangible assets Extraordinary gains or losses due to catastrophic event Write-off of research and development Exchange rate gains and losses Unrealized gains or losses from revaluation of assets 59 Example 4: Reinvested Earnings Balance of Payments Division IMF Statistics Department Profit and Loss Statement of Enterprise A. Nonresidents DI own 50 percent of the equity of A 1. Sales of finished goods + increase in inventories of finished goods 20.000 500 2. Transport services provided 3.000 3. Repair services 6.000 4. Dividends 3.000 5. Interest on bonds 1.000 6. Profit on sale of property 1.000 7. Total revenue (1 through 6) 34.500 8. Raw materials purchased 12.000 – increase in inventories of materials 2.000 9. Salaries and wages 5.000 10. Office rental 11. Travel of employees 12. Fuel, electricity, other costs 500 2.000 500 13. Depreciation 1.000 14. Interest on loans 1.000 15. Bad debt provisions 2.000 16. Total expenses (8 through 15) 22.000 17. Net income (before taxes) 12.500 18. Taxes on income 4.000 19. Net income (after taxes) 8.500 20. Dividends payable 5.000 60 Balance of Payments Division IMF Statistics Department Example 3: Reinvested Earnings - Enterprise A Net income after taxes (line 19) +8.500 – dividends (line 20) -5.000 3.500 – revenue not part of output, primary income or secondary income: holding gains (line 6) -1.000 + expenses not being a transaction bad debt provisions (line 15) +2.000 Reinvested earnings 4.500 Reinvested earnings of the direct investor: 4,500 * 0.5 2.250 Current Account Credit Primary Income- Investment Income. Direct Investment Income on equity. Reinvested earnings Financial Account Direct Investment. Equity Reinvestment of earnings Debit 2.250 NAFA NIL 2.250 61 Balance of Payments Division IMF Statistics Department Where and How to Collect Direct Investment Data? Major Data Sources Surveys •Direct investment specific surveys is the most efficient approach, collecting data from respondents consistent to international statistical standards Financial Statements •Data on position can be sourced from balance sheets and income transactions from income and expenditure account ITRS •Many countries are relying on an international transactions reporting system that become available from banking records Foreign Investment Approvals •National Agencies responsible for approving or regulating inward direct investment activities •They may also facilitate residents’ direct investment abroad Mirror/Derived Data •The IMF Coordinated Direct Investment Survey (CDIS) provides direct investment position by counterpart economies for participant countries 62 Balance of Payments Division IMF Statistics Department Direct Investment Specific Surveys The BPM6 Compilation Guide presents two different forms, which may serve as starting point for designing the direct investment questionnaire Model Form 17 of the BPM6 Compilation Guide, pp. 554-563 Form 17 collects financial cross-border assets and liabilities, of which direct investment, in a reconciliation statement • Data are requested separately for positions, both opening and closing and reasons for change between the two positions – transactions and other changes • In addition, the form includes investment income linked to the corresponding position data, withholding taxes and explicit fees and charges on the transactions 63 Balance of Payments Division IMF Statistics Department Direct Investment Specific Surveys Model Form 18 of the BPM6 Compilation Guide, pp. 564-578 Its tailor made to collect data on direct investment only • This survey form collects other direct investment-related information that can be used for analytical purposes and for quality control In both model forms 17 and 18, direct investment assets and liabilities are separately identified, in line with BPM6, to show the relationship of: • • • Direct investors in direct investment enterprises Direct investment enterprises in direct investors (reverse investment) Between fellow enterprises 64 Balance of Payments Division IMF Statistics Department Steps After the Surveys Drawing data from surveys: the compiler is likely to be concerned with non-response There are several ways to deal with non response, of which Approaches to deal with nonresponse • company financial statements • use of ITRS for large transactions to add to previous stock For economies that have conducted surveys before •carry forward techniques using earlier surveys For economies where surveys have not been previously conducted • Raising factor (crude method) = multiplying survey data by volume of companies surveyed divided by number of respondents 65 Balance of Payments Division IMF Statistics Department Grossing Up the Survey Results Expanding results from a selection of respondents to measure the population as a whole How does the compiler expand the sample or gross-up the survey results to the population? • • Weighing techniques – applying expansion factors to the sample response More advanced technique – stratified expansion, where the raising factor used take into consideration the characteristics of the number of units surveyed in the sample vis-à-vis units of same characteristics in the population 66 Balance of Payments Division IMF Statistics Department Example of Grossing Up: Using Survey of Large Entities Country X conducts a sample survey of large entities (LEs) (which are DIENTs of foreign owned companies) A sample representing 80% of the population of LEs are targeted in the survey. The common characteristic for this sample is they are all managing assets let’s say US$100 million However, at submission deadline and after several follow-ups, out of the 20 entities surveyed, only 15 responded. The consolidated assets of the 15 entities equal US$1,200 million out of which direct investment assets amounted to US$600 million Now how does the compiler go about to use the survey results to incorporate in the IIP? 67 Balance of Payments Division IMF Statistics Department Example of Grossing Up: Using Survey of LEs First, the compiler has to account for non-response: To gross up to the sample, the compiler can use a simple raising factor RF = Number of units reported = 15 Total number of units in sample = 20 = 0.75 In this case , direct investment assets for the sample will be grossed up to 600 x 1 RF = 600 x 1 0.75 = 800 Second, the compiler has to expand the sample to the population Given that the sample represents 80% of the population: Direct Investment Assets = 800 x 1/0.8 = 1,000 The compiler will therefore after the two steps include US$1,000 in the IIP 68 Balance of Payments Division IMF Statistics Department Financial Statements Financial statements can provide useful data for deriving/estimating direct investment transactions and obtaining positions Income statements may provide direct investment income data but may not give out a residency-based split (resident/nonresident) to allow ready identification In that case notes to the financial statement can provide a cue to the compilers for both direct investment transactions and position data In some countries, data on direct investment debt instruments can be sourced from a registry of external loans used to track private sector external debt 69 Balance of Payments Division IMF Statistics Department How to Read Direct Investment Liability Position from a Balance Sheet? Balance Sheet of XYZ Company as on 31st December 2014 (DIE of XYZ International) Liabilities Reserves Eq. Share Capital Pr. Share Capital Reserves and Surplus Capital Reserve General Reserve Share Premium Retained Earnings (P/L Appr) Other Reserves Long Term Loans Fixed Deposits Collected Debentures Provisions for Taxation Provisions for Dividends Outstanding Expenses Pre received Incomes Unclaimed Dividends Sundry Creditors Bills Payable Bank Overdraft Amount 35,000,000 12,000,000 6,000,000 12,000,000 3,500,000 43,500,000 4,000,000 54,000,000 16,000,000 24,000,000 3,000,000 4,000,000 5,000,000 2,000,000 200,000 13,000,000 12,000,000 5,000,000 Reinvested earnings Assets Goodwill Land Buildings Plant and Machinery Furniture and Fittings Motor Vehicles Patents, Trade Marks, Copyrights Investments Stock of Raw Material Work in Progress Finished Goods Stock Prepaid Expenses Incomes Receivable Paid-up Capital Sundry Debtors Cash Bank Balance Loans and Advances Bills Receivable Deferred Revenue Expenditure Miscellaneous Expenses Discounts to be written off Accumulated Loss (P/L Appr a/c debit balance) 254,200,000 Amount 8,000,000 35,000,000 27,000,000 15,000,000 25,000,000 35,000,000 18,000,000 24,000,000 2,500,000 2,400,000 3,000,000 4,000,000 3,000,000 26,000,000 1,160,000 6,000,000 15,000,000 54,000,000 1,200,000 2,400,000 254,200,000 70 Balance of Payments Division IMF Statistics Department How to Use the Financial Statements: an Illustration for Equity Investment The compiler may be able to estimate the direct investment position from the shareholders’ equity portion of the balance sheet which may include: XYZ International Corporations Balance Sheet As at December 31, 2014 (US$) Shareholders’ Equity 12,600,000 (1) Paid up capital 4,700,000 (2) All types of reserves identified as equity in the B/Sheet 2,550,000 (3) Cumulated reinvested earnings 4,350,000 (4) Holding gains/ losses - 100 percent direct investor shareholding = US$ 12.6 million 50 percent direct investment shareholding = US$ 6.3 billion (50%*12.6) 71 Balance of Payments Division IMF Statistics Department Approval/Licensing of Foreign Investment Advantages: •In some economies, these regulatory bodies may ask for the provision of all required financial information on an ongoing basis •Can always help to update business register •Useful for identifying nonresidents who invest in real estate The serviceability of such data for direct investment is limited: •Regulation not set up with statistical requirements in mind •Intended investment recorded, actual investment may not take place. •Significant lags between intent and actual •May capture only new direct investment relationship, ignore non equity transactions like inter company lending •Approving of certain key sectors like petroleum, banks may not lie with the promotion agency 72 Balance of Payments Division IMF Statistics Department Mirror/Derived Data CDIS Table 3 – presents mirror direct investment position Data on inward direct investment positions reported by an economy are shown side-by-side against data on outward direct investment positions reported by the counterpart economy (i.e., mirror data for inward data reported) Similarly, data on outward positions reported by an economy are shown side-by-side against data on inward positions reported by the counterpart economy 73 Balance of Payments Division IMF Statistics Department Mirror/Derived Data Usefulness of mirror data: • For countries that do not participate in CDIS, mirror data as reported by their counterparts can provide insights on their total inward and outward direct investment positions (directional principle) Direct use of these data for partner economies could need some adjustments • because the absence of data from some counterpart economies: • they are not reporting economies or they do not provide data with some partners to preserve confidentiality Compiler must re-arrange from inward/outward to assets/liabilities presentation 74 Balance of Payments Division IMF Statistics Department Mirror/Derived Data Usefulness of mirror data: • For economies that participate in the CDIS, mirror data could be used: to cross check and verify their own estimates and may also be very useful in highlighting data gaps or errors at counterpart economy level 75