Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

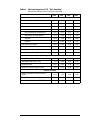

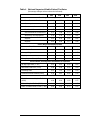

The Sources of the Recession in Canada: 1989-1992 Thomas Wilson Peter Dungan Steve Murphy* University of Toronto Introduction restructuring related to the increased competition in the world economy. The Canadian economy entered a recession in the second quarter of 1990, following a period of slowing real growth over the previous year. The recession technically lasted four quarters,1 about average length for postWorld War II recessions in Canada. However, the recovery, which began with a one-quarter growth spurt in the second quarter of 1991, has been anaemic. Real growth over the first seven quarters of recovery averaged 1.3 per cent (annual rate), well below the historical norms for previous early recovery periods, and well below the growth of potential output. Key aggregate indicators for the 1989-92 period are presented in Table 1. The purpose of this article is to assess the contributions of macro-economic policies and macro-economic developments abroad in explaining the cyclical behaviour of the Canadian economy over the 1989-92 period. The approach taken is similar to that of the analysis of the 1981-82 recession and 1982-84 recovery previously carried out by Wilson (1985) who found that most of that cycle could be explained by such developments. Opponents of the Canada-U.S. Free Trade Agreement (FTA), which took effect at the beginning of 1989, have argued that the FTA was a major factor undermining Canada’s economic performance in recent years. Others have emphasized the negative effects of the central bank’s tough anti-inflationary monetary policy.2 And many commentators in the financial press have focused on the need for The remainder of our article is organized as follows. The second section discusses the methodology of the analysis. The third section describes how each macro-economic ‘event’ is modelled. The fourth section presents the results, and the final section draws some conclusions. Methodology The method of analysis we use to appraise the impact of domestic policies and external developments involves counter-factual historical simulations with a macro-econometric Table 1 Selected Economic Indicators, 1989-1992 GDP Real (% change) Unemployment Rate (%) CPI Inflation Rate (%) Real Disposable Income (% change) 1989 2.4 7.5 5.0 4.4 1990 -0.2 8.1 4.8 0.2 1991 -1.7 10.3 5.6 -2.7 1992 0.7 11.3 1.5 0.8 3 Canadian Business Economics Winter 1994 model of the Canadian economy. The model used—the FOCUS model—is a medium-scale macro-model which has been used for projections and policy analysis since 1977.3 Basically, the procedure used is to construct an historical base case for the model which fits actual data exactly.4 Policy or external developments are then analyzed by changing exogenous variables and/or parameters in the model and solving the model to derive the counter-factual result for the particular policy change or development. For example, in the analysis of the impact of the U.S. recession, all exogenous variables from the U.S. economy were adjusted to represent a ‘soft-landing’ for the U.S. economy, and another solution of the FOCUS model was calculated. The differences between this solution and the historical base case represent the estimated effects of the U.S. recession. It is important, in doing this type of analysis with a macro-model that the monetary policy regime be specified appropriately. This is particularly important for the FOCUS model, because it is highly sensitive to monetary policy changes. With the exception of the simulation which examines the consequences of a monetary policy ‘overshoot’, all simulations were run with monetary policy targeting the base case inflation rate (adjusted for indirect taxes). We felt that this was appropriate given the Bank of Canada’s commitment to reducing inflation and given the announcement of formal inflation targets early in 1991 (Crow, 1988; Bank of Canada, 1991a). The exchange rate is, of course, allowed to float in all simulations. In the following section, we briefly describe the modelling of each simulation analysis. Description of Modelling of Each ‘Event’ External developments: A U.S. ‘Soft Landing’ The U.S. economy entered a recession in the third quarter of 1990 which lasted for three quarters. The U.S. recovery was also sluggish in its early stages, though more robust growth was achieved in the last three quarters of 1992. Since the U.S. recession began two quarters later than the Canadian recession, it is unlikely to have been a ‘trigger’ for the latter. However, given the strength of trade and investment linkages between the two economics, weak U.S. economic performance could have contributed to the depth of the recession and the sluggish recovery in Canada. In order to examine the impact of the U.S. recession, we constructed an alternative model solution which incorporated a ‘soft landing’ for the U.S. economy. We assume that the U.S. experienced 2.5 per cent growth in real GNP and industrial production in 1989, 2.1 per cent growth in 1990 and 1991, and 2.5 per cent growth in 1992. The demand for motor vehicles is assumed to grow by 2 per cent in 1989, 1990 and 1991 and Table 2 Impacts on U.S. Prices and Interest Rates of U.S. Soft Landing Assumptions Percentage change in 1990 1991 1992 GNP Deflator 0.06 0.38 0.88 Consumer Price Index 0.02 0.20 0.50 Wholesale Price Index 0.15 0.66 0.70 Wage Rate 0.02 0.20 0.50 Consumer Durables Price 0.02 0.20 0.50 Short Term Interest Rate* 0.11 0.69 0.70 Long Term Interest Rate* -0.04 0.12 0.15 Winter 1994 Canadian Business Economics 4 by 2.5 per cent in 1992.5 The impact of these U.S. soft landing scenario assumptions on U.S. prices and interest rates was based on Project LINK macroeconometric model results for the U.S. economy6 (Table 2). These in turn were fed into the FOCUS model along with the assumed changes in U.S. GNP, industrial production and motor vehicle demand. The impact of these developments on the Canadian economy is analyzed by adjusting the various U.S. exogenous variables in FOCUS and solving the model to generate the U.S. ‘soft landing’ scenario. As noted above, monetary policy is assumed to neutralize the price level effects of any changes in the external variables. Monetary Policy Overshoot In February 1991, the Bank of Canada and the Department of Finance announced formal price inflation targets, making explicit the quantitative objectives of the Bank’s anti-inflation policy. These targets7 are presented in Table 3 below: In the event, the ‘core’ inflation rate observed over the 12 month period ending December 1992 was 1.7 per cent, well below the Bank of Canada’s 3 per cent target. In order to explore the role of monetary policy in the recession, we have modelled the impact of the Bank of Canada having adjusted monetary policy so as to hit exactly the 3 per cent inflation target.8 In this simulation the money supply was adjusted upward gradually over the interval in order to achieve the 3 per cent inflation target by the end of 1992.9 Federal Tax Increases The federal government instituted several tax increases over the 1989-91 period. Most of these increases involved sales, excise, and payroll taxes. At the beginning of 1991, a major reform of the federal sales tax system was implemented, which is treated in a separate simulation described below. To explore the role of the other tax measures, two model simulations were constructed. In the first, all federal tax rates were simply held constant at their 1989Q1 levels.10 This simulation would approximate the effects of a ‘neutral’ contra-cyclical fiscal policy, since cyclically adjusted program spending did not 5 Table 3 Inflation Targets Period Year Over Year ‘Core’ Inflation Target End 1992 3.0 Mid 1994 2.5 End 1995 2.0 increase relative to potential output over the four year period.11 However, the consequences of this policy would involve larger deficits and a higher debt/GDP ratio at the end of the period. Since containment of the growth of the debt was an explicit objective of federal fiscal policy,12 we also constructed an alternative scenario in which stable tax rates are accompanied by gradual expenditure restraints, such that the debt/GDP ratio at the end of the period is the same as in the base case. When indirect (sales, excise, and payroll) tax rates are held constant, direct upward pressures on prices and unit costs are lower. In both of these simulations, monetary policy therefore targets the base case Consumer Price Index (CPI) less the direct (‘first round’) price effects attributable to the indirect tax increases. Transitional Effects of Sales Tax Reform On January 1, 1991 a new broad-based value added tax—the Goods and Services Tax (GST)—replaced the Federal Manufacturers’ Sales Tax. Although the sales tax reform was designed to be approximately revenue neutral, it did increase the sales tax burden on consumer goods and services. As a result the CPI would increase by 1 per cent as a direct consequence of the new sales tax system (Department of Finance, 1989). In previous work (Dungan and Wilson, 1989), we have explored the possible transitional effects of the implementation of the GST under alternative monetary policy responses. In the current analysis, we constructed a counter-factual simulation without the GST. In this simulation, monetary policy targets the CPI after adjustment to remove the impact effect of sales tax reform, i.e. since prices would have been 1.25 per cent lower as a direct re- Canadian Business Economics Winter 1994 sult of reversing the sales tax changes, the money supply is reduced sufficiently to be consistent with this lower price level. Chart 1 Sources of the Recession GDP Path—Canada Aggregate Supply: Potential Output Assumptions For simplicity we assume that actual output in 1989Q1 equalled potential output.13 Over the 1989-92 interval we assume that potential output growth was 3 per cent per year,14 plus an adjustment for the impact of the CanadaU.S. Free Trade Agreement (FTA) on total factor productivity (TFP). The FTA adjustments to TFP are those used by Dungan and Wilson (1991), which were based on the work of Harris (1991). These FTA adjustments are relatively small over the four years; the cumulative effect is an addition of 0.4 per cent to potential output in 1992. The reader should note that the estimated level of potential GDP does not affect the simulation results. Rather it is used as a reference point to measure the extent to which deviations of actual from potential output are accounted for by the four factors which we analyze. economic performance of its leading trading partner, the U.S. recession alone cannot explain the severity of the 1990-91 recession in Canada, nor the slow growth achieved in 1992. Monetary Policy Overshoot Results We shall first present the results for each of the simulations described above, and then consider their joint effects. The results for the individual simulations are presented in Tables 4 through 8 at the end of the article. Their joint effects are presented in Charts 1, 2, and 3. U.S. Soft Landing Had the U.S. economy achieved the much hoped for ‘soft landing’ at the end of the boom of the late 1980s, the real growth performance of the Canadian economy would have been better, as shown in Table 4. However, the soft landing of the U.S. economy would not have had much impact in Canada until 1991. Hence it is unlikely that the Canadian economy could have avoided a recession during 1990 under this scenario. Viewing the results over the four year period, the U.S. soft landing would have been sufficient to keep the Canadian economy in a ‘holding pattern’ with real GDP roughly stable over the period. Although the U.S. recession obviously was therefore an important factor worsening the Winter 1994 The severity of the Bank of Canada’s anti-inflation policy may be gauged by money supply statistics—M1 declined for the first three quarters of 1990—and in short-term interest rates—which moved to levels 5-6 percentage points above corresponding U.S. rates early in 1990. As earlier noted, monetary policy was sufficiently restrictive to cause an overshoot of the Bank’s inflation reduction targets: the ‘core’ inflation rate achieved at the end of 1992 was 1.3 per cent below the target. In the alternative simulation, money supply growth is gradually augmented over the interval so as to achieve the target inflation rate of 3.0 per cent for the end of 1992. The results, presented in Table 5, indicate that ‘excessive’ monetary restraint significantly reduced real growth in 1990 and 1991, and slowed growth somewhat in 1992. Clearly, monetary restraint was an important factor contributing to the recession and slow growth realized over the period. The model results also imply that restrictive monetary policy gradually reduced inflation, Canadian Business Economics 6 Chart 2 Sources of the Recession It is noteworthy that the two alternative simulations do not differ by a large amount. Of course, eliminating the tax increases has a stronger positive effect on real output than the combination of stable taxes and expenditure restraints, but the differences between them are much smaller than what would be expected from conventional analysis. What accounts for this? GDP Path—Canada Recall that all simulations (except the monetary policy overshoot) are run with monetary policy targeting the inflation rate (adjusted for indirect taxes). Since indirect tax increases generate secondary wage and price pressures in the FOCUS model, a more restrictive monetary response must accompany this type of fiscal restraint than under the alternative of expenditure restraints. Sales Tax Reform Chart 3 Sources of the Recession The fourth factor we examine is the transitional impact of Sales Tax Reform. As shown in Table 8, the launching of the GST at the beginning of 1991 had a negative effect on real output in 1991 and 1992. Once again this negative effect is attributable to the need for monetary restraint to offset the secondary wage and price pressures generated by the new tax system.15 Unemployment Rate Path—Canada As we allow for no anticipatory effects of the new regime, the negative effects on real growth are concentrated in 1991, with a small additional negative effect in 1992. Our previous analysis (Dungan and Wilson, 1989; Dungan, Mintz and Wilson, 1990) would indicate that the transitional impact should attenuate as the economy adjusted to the new system.16 although its impact on prices was masked by the effects of demand pressure in 1989 and by indirect tax increases, particularly in 1991. Tax Increases The results of the two alternative simulations which examine the effects of federal tax increases are presented in Tables 6 and 7. The results indicate that these tax increases were about as important as monetary policy in contributing to reduced output over the period. 7 Although the GST was perhaps the most visible feature of federal tax policies over the period, its net effect was considerably smaller than the combined impact of the other federal tax measures, reducing real GDP by 0.8-0.9 per cent over 1991-92. Joint Effects of the Four Developments Combined effects of the four factors are presented in Charts 1 and 2. The most striking feature of the results is highlighted in these charts: the four factors we have examined ex- Canadian Business Economics Winter 1994 plain most of the shortfall between actual and potential output over the period.17 As is clear from the charts, domestic monetary and tax policies were the main factors accounting for the recession of 1990. By 1991, these two factors were reinforced by the impact of the U.S. recession and the transitional effects of implementing the GST. The slow growth puzzle of 1992 is also explained by these factors. Although the negative impact of the U.S. recession attenuated as the U.S. economy recovered, the restraining effects of the other three factors increased, so that real growth was held to a moderate pace in the first year of recovery. Implications for Unemployment Chart 3 summarizes the effects of the four events on the unemployment rate. As is clear, in the absence of the U.S. recession, the monetary policy overshoot, and the various tax increases, the rise in the unemployment rate would have been quite moderate. The analyses indicate a peak unemployment rate just below 8.0 per cent, consistent with a ‘soft landing’ for the Canadian economy. Conclusions The results of this article indicate that conventional macro-economic factors—the business cycle in the U.S., monetary policy restraints, and indirect tax increases—largely explain both the depth of the recession in Canada and the sluggish recovery of the Canadian economy of 1991-92. zation and the restructuring of Canadian industry should be at its peak. The associated productivity gains are stretched out, with the largest increase in total factor productivity growth achieved in the late 1990s. A Look Ahead Although this is not an article about forecasting, we venture a comment on the future strength of the recovery in Canada. At this point it appears reasonably clear that each of the four negative factors, which have acted to restrain real growth in the recent past, has been reversed. The U.S. economy continues to recover; monetary growth has resumed at a pace consistent with positive real income growth at current inflation rates; federal tax rates have been reduced slightly; and the transitional effects of the GST have been digested.19 In the absence of other adverse economic shocks, the reversal of the four factors which we have examined would therefore be consistent with a vigorous recovery this year. Unfortunately, several provinces increased taxes in their 1992 and 1993 budgets.20 While the 1994 federal budget included some effective tax increases through base-broadening measures, it also included a small future reduction in federal payroll taxes. The federal budget plan also incorporated the major reductions in tobacco excise taxes which were put into effect two weeks before the budget. Whether on balance these tax measures will exert a drag on the recovery is a topic for future research. While the restructuring of industry in response to the FTA and to other international competitive pressures may well affect the regional and industrial composition of economic activity,18 and may explain the resurgence of productivity growth despite continued weakness of final demand, there is no need to enlist these factors to explain the current business cycle. Our previous analysis of the FTA (Dungan and Wilson, 1991) indicated that it should have favourable effects on aggregate demand as well as aggregate supply in the middle years of this decade. This is the period when the investment associated with the rationaliWinter 1994 Canadian Business Economics 8 were somewhat higher (10.2 per cent and 10.4 per cent, respectively) in 1990 and 1991. Notes * 1. Earlier versions of this paper were presented to the Canadian Economics Association annual meeting in Ottawa (June 1992), and to the European meetings of the Econometric Society in Uppsala, Sweden (August 1993). The research support of the University of Toronto and PEAP members is gratefully acknowledged. Aggregate output declined for four quarters. However, Statistics Canada did not formally declare the recession over until the fall of 1992 (Statistics Canada, 1992). 2. See for example Stokes (1992) and Fortin (1993). 3. For a description of the current version of FOCUS see Dungan and Jump (1992). An earlier version of FOCUS was used in Wilson’s (1985) work on the previous business cycle. 4. The historical base case was constructed using actual values for all endogenous and exogenous variables. Each equation in the model was adjusted using add-factors (constant adjustments) so that the base case solution exactly replicated the historical data. 5. The U.S. National Accounts have subsequently been revised with GNP growth stronger than previously estimated. However, the key linkages to the U.S. economy in the FOCUS model use industrial production and auto demands, which did not change significantly. The impacts of the revisions are therefore negligible. 6. We are indebted to our associate, Hung-Yi Li, for providing the LINK model results. 7. The targets are for the Consumer Price Index excluding food and energy, and are net of indirect tax effects. For a discussion of these issues, see Bank of Canada (1991b). 8. Although the Bank of Canada targets are defined for the ‘core’ inflation rate, this rate is not generated within the FOCUS model. We therefore targetted the aggregate CPI inflation rate. The two rates were very close over the 12 month period ending in December 1992. 9. Since we model the impact of the overshoot of the disinflation target, we make no allowance for any adverse effects of the setting (and achieving) of the targets themselves. Previous work by one of the authors (Dungan, 1990) indicates that the adverse real output effect of achieving disinflation targets depends critically on the credibility of the announced policy targets. 10. Unemployment Insurance contribution rates were treated as a payroll tax and hence were held constant at their 1989Q1 levels. Since CPP and QPP contributions are not federal taxes, their rates were set at historical values. 11. Government spending excluding unemployment insurance payments and interest payments on the public debt was 10.0 per cent of potential output in 1989 and 10.1 per cent in 1992. However, the ratios 9 12. See the Federal Budget Papers of 1989, 1990 and 1991. 13. The unemployment rate in 1989 was 7.5 per cent, which lay within the range of estimates of the NAIRU for Canada. 14. The 3 per cent growth of potential output is consistent with the trend growth of output over the 197989 period. 15. The results presented in Table 8 are based on a direct price level impact of 1.2 per cent for the GST, which is close to the estimate published by the federal government in 1991. However, the revised national accounts data indicate a revenue gain from sales tax reform which is lower than that implied by the 1.2 per cent price increase. A simulation based on the revenue impacts would show smaller real output effects—real GDP would be 0.4-0.5 per cent lower in 1991-92, roughly half of the impact shown in Table 8. 16. The quarterly pattern of effects within 1992 suggests that this attenuation had already started. 17. If potential output were not adjusted for the effects of the FTA, virtually all of the shortfall would be explained. 18. In particular, central Canada has been hit relatively harder by the recession. 19. Our previous analysis (Dungan and Wilson, 1989) indicated that the adverse effect of the GST lasted for two years. However, the Liberal government is committed to a major review of the GST. Of the available alternatives, we believe the most likely replacements will be broad-based indirect taxes with the same net effect on the CPI, and hence will have little transitional effect on real output. Some other alternatives would involve reduction in the indirect tax component of the CPI. For a discussion of alternatives see Dungan, Mintz and Wilson (1990). 20. Moreover, some of these tax increases involved sales taxes—for example, British Columbia increased its sales tax rate by one percentage point in its 1993 budget, and Ontario broadened its sales tax base to include insurance in its 1993 budget. References Bank of Canada (1991a) Press Release on “Targets for Reducing Inflation and Reaching Price Stability in Canada,” February 26. Bank of Canada (1991b) “Targets for Reducing Inflation: Further Operational and Measurement Considerations,” Bank of Canada Review, September. Crow, John W. (1988) “The Work of Canadian Monetary Policy,” Bank of Canada Review, February. Department of Finance (1989) Goods and Services Tax. Canadian Business Economics Winter 1994 Dungan, Peter (1990) “Getting to Zero Inflat i o n : S i m u l at i o n s w i t h t he FO C U S Model,” PEAP Policy Study 90-10, University of Toronto. Dungan, Peter and Gregory V. Jump (1992) FOCUS: Forecasting and User Simulation Model, Version 92A, Institute for Policy Analysis, University of Toronto. Dungan, Peter, Jack Mintz and Thomas Wilson (1990) “Alternatives to the GST,” Canadian Tax Journal, May-June. Dungan, D.P. and T.A. Wilson (1989) “The Proposed Federal Goods and Services Tax: Its Economic Effect Under Alternative Labour Market and Monetary Policy Conditions,” Canadian Tax Journal, March-April. Dungan, D.P. and T.A. Wilson (1991) “The Canada-U.S. FTA: Macroeconomic Effects and Sensitivity Analysis,” Journal of Winter 1994 Policy Modelling, Vol. 13, No. 3, pp. 43557. Fortin, Pierre (1993) “The Unbearable Lightness of Zero-inflation Optimism,” Canadian Business Economics, Vol. 1, No. 3, pp. 3-18. Harris, R.G. (1991) “The Canada-U.S. FTA: Economic Impact and Transition Effects,” Journal of Policy Modelling, Vol. 13, No. 3, pp. 421-34. Statistics Canada (1992) Canadian Economic Observer, Catalogue No. 11-010, November. Stokes, Ernie (1992) “Has Monetary Policy Been Too Tight?” Canadian Business Economics, Vol. 1, No. 1, pp. 3-15. Wilson, Thomas A. (1985) “Lessons of the Recession,” Canadian Journal of Economics, XVIII, No. 4, pp. 693-722. Canadian Business Economics 10 Table 4 National Impacts of U.S. “Soft Landing” (Percentage changes unless otherwise indicated) 1989 1990 1991 1992 Real Output and Components Real Gross Domestic Product -0.02 0.63 2.18 1.06 Consumption 0.00 0.23 1.27 2.19 Government Current & Capital 0.00 0.00 0.00 0.00 Residential Construction -0.10 0.99 3.56 0.06 Non-Residential Construction -0.03 0.77 2.78 1.12 Machinery and Equipment -0.04 0.62 3.33 3.86 Exports 0.04 1.84 7.37 6.26 Imports -0.01 0.69 4.79 8.04 Consumer Price Index 0.00 0.00 0.00 0.00 Average Wage 0.00 0.18 0.72 0.81 -0.01 0.20 0.92 0.94 0.01 -0.13 -0.60 -0.58 Employment Unemployment Rate (% Pts) Interest Rates, Exchange Rate and Balance of Payments 90-day Paper Rate (% Pts) 0.01 0.20 0.02 0.69 Industrial Bond Rate (% Pts) 0.01 0.24 0.02 0.81 Exchange Rate 0.07 0.40 2.86 5.33 Current Account Balance ($ Bill) 0.04 2.23 6.66 2.03 Deficits and Debt Total Government Surplus/Deficit ($ Bill) -0.08 1.79 7.20 4.98 Federal Surplus/Deficit ($ Bill) -0.06 1.22 4.44 2.13 0.02 -0.33 -1.65 -1.99 Ratio of Federal Debt to GDP (% Pts) 11 Canadian Business Economics Winter 1994 Table 5 National Impacts of Monetary Policy Achieving 1992 Inflation Target (Percentage changes unless otherwise indicated) 1989 1990 1991 1992 Real Output and Components Real Gross Domestic Product 0.52 1.48 2.88 4.02 Consumption 0.06 0.29 0.80 1.67 Government Current & Capital 0.00 0.00 0.00 0.00 Residential Construction 0.85 2.66 5.06 5.98 Non-Residential Construction 0.71 2.13 4.14 6.61 Machinery and Equipment 0.58 2.46 4.48 6.78 Exports 0.46 1.42 2.91 4.13 Imports -0.64 -1.13 -1.58 -0.83 Prices, Wages and Unemployment Consumer Price Index 0.15 0.66 1.77 3.17 CPI Inflation Rate 0.16 0.53 1.16 1.40 Average Wage 0.25 1.01 2.47 4.42 Employment 0.15 0.54 1.18 1.82 -0.10 -0.35 -0.74 -1.10 Unemployment Rate (% Pts) Interest Rates, Exchange Rate and Balance of Payments 90-day Paper Rate (% Pts) -0.17 -0.28 -0.15 -0.01 Industrial Bond Rate (% Pts) -0.19 -0.33 -0.17 -0.01 Exchange Rate -1.16 -3.32 -6.48 -8.90 1.26 3.18 5.76 8.13 Current Account Balance ($ Bill) Deficits and Debt Total Government Surplus/Deficit ($ Bill) 1.44 4.96 10.29 15.11 Federal Surplus/Deficit ($ Bill) 0.99 3.33 6.69 9.47 -0.31 -1.24 -3.21 -5.90 Ratio of Federal Debt to GDP (% Pts) Winter 1994 Canadian Business Economics 12 Table 6 National Impacts of Stable Federal Tax Rates (Percentage changes unless otherwise indicated) 1989 1990 1991 1992 Real Output and Components Real Gross Domestic Product 0.49 1.60 2.38 5.08 Consumption 0.45 1.87 3.27 5.18 Government Current & Capital 0.00 0.00 0.00 0.00 Residential Construction 0.47 1.11 1.07 5.40 Non-Residential Construction 0.37 1.26 1.33 4.40 Machinery and Equipment 0.39 2.36 3.34 4.27 Exports 0.23 0.72 1.08 2.67 Imports 0.21 0.42 1.17 0.22 Prices, Wages and Unemployment Consumer Price Index 0.32 0.66 1.23 1.81 CPI Inflation Rate 0.34 0.36 0.60 0.60 Average Wage 0.04 0.13 0.12 0.75 Employment 0.18 0.80 1.39 2.50 Unemployment Rate (% Pts) 0.13 0.54 0.90 1.59 Interest Rates, Exchange Rate and Balance of Payments 90-day Paper Rate (% Pts) 0.03 0.23 0.48 0.03 Industrial Bond Rate (% Pts) 0.04 0.26 0.56 0.04 Exchange Rate 0.51 1.23 1.54 4.38 Current Account Balance ($ Bill) 0.34 0.67 2.48 0.18 Deficits and Debt 13 Total Government Surplus/Deficit ($ Bill) 0.99 2.01 3.52 2.77 Federal Surplus/Deficit ($ Bill) 1.49 4.06 6.69 4.25 Ratio of Federal Debt to GDP (% Pts) 0.05 0.16 0.78 0.83 Canadian Business Economics Winter 1994 Table 7 National Impacts of Stable Federal Tax Rates with Expenditure Restraints (Percentage changes unless otherwise indicated) 1989 1990 1991 1992 Real Output and Components Real Gross Domestic Product 0.32 1.29 1.83 4.31 0.38 1.63 2.82 4.52 -0.69 -1.35 -1.95 -2.49 Residential Construction 0.45 1.21 1.05 5.03 Non-Residential Construction 0.32 1.22 1.23 4.22 Machinery and Equipment 0.34 2.33 3.38 4.36 Exports 0.24 0.77 1.12 2.68 Imports -0.33 0.03 0.63 -0.94 Consumption Government Current & Capital Prices, Wages and Unemployment Consumer Price Index -0.32 -0.66 -1.23 -1.81 CPI Inflation Rate -0.34 -0.36 -0.60 -0.60 Average Wage -0.07 0.03 -0.08 0.43 0.12 0.64 1.11 2.11 -0.08 -0.43 -0.72 -1.35 Employment (% Change) Unemployment Rate (% Pts) Interest Rates, Exchange Rate and Balance of Payments 90-day Paper Rate (% Pts) -0.08 0.08 0.32 -0.14 Industrial Bond Rate (% Pts) -0.10 0.09 0.37 -0.17 Exchange Rate -0.51 -1.30 -1.53 -4.32 0.60 0.24 -1.01 2.45 Current Account Balance ($ Bill) Deficits and Debt Total Government Surplus/Deficit ($ Bill) -0.35 -0.53 -1.48 5.43 Federal Surplus/Deficit ($ Bill) -0.65 -2.05 -3.65 -0.21 Ratio of Federal Debt to GDP (% Pts) -0.03 0.03 0.37 0.00 Winter 1994 Canadian Business Economics 14 Table 8 National Impacts of Reversal of Sales Tax Reform (Impacts are percentage changes unless otherwise indicated) 1991 1992 Real Output and Components Real Gross Domestic Product 0.76 0.94 Consumption 1.69 1.74 Government Curr & Capital 0.00 0.00 Residential Construction 0.49 1.18 Non-Residential Construction -0.68 -0.06 Machinery and Equipment -1.65 -3.10 Exports 0.08 0.34 Imports 0.38 0.08 Consumer Price Index -1.15 -1.10 CPI Inflation Rate -1.21 0.05 Average Wage 0.01 0.43 Employment (% Change) 0.51 0.74 -0.34 -0.47 Prices, Wages and Unemployment Unemployment Rate (% Pts) Interest Rates, Exchange Rate and Balance of Payments 90-day Paper Rate (% Pts) 0.12 0.01 Industrial Bond Rate (% Pts) 0.14 0.01 Exchange Rate -0.19 -0.74 Current Account Balance ($ Bill) -0.79 -0.20 Revenues and Deficits 1990* * 15 1991 1992 Total Government Surplus/Deficit ($ Bill) 1.34 -1.75 -1.05 Fed. Sales and Oth. Excise Taxes ($ Bill) 0.00 -2.66 -2.90 Federal Surplus/Deficit ($ Bill) 1.56 -1.82 -1.27 This simulation begins in 1990:4 when the federal government is deemed not to have paid credits intended to offset MST already paid on goods in inventories at the end of 1990. Canadian Business Economics Winter 1994