Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

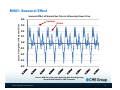

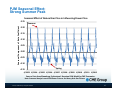

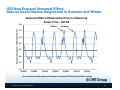

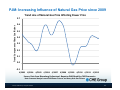

Observing the Changing Relationship Between Natural Gas Prices and Power Prices The research views expressed herein are those of the author and do not necessarily represent the views of the CME Group or its affiliates. All examples in this presentation are hypothetical interpretations of situations and are used for explanation purposes only. This report and the information herein should not be considered investment advice or the results of actual market experience. Samantha Azzarello Economist, CME Group April 2013 Risk Disclosures Futures trading is not suitable for all investors, and involves the risk of loss. Futures are a leveraged investment, and because only a percentage of a contract’s value is required to trade, it is possible to lose more than the amount of money deposited for a futures position. Therefore, traders should only use funds that they can afford to lose without affecting their lifestyles. And only a portion of those funds should be devoted to any one trade because they cannot expect to profit on every trade. The Globe Logo, CME, Chicago Mercantile Exchange, and Globex are trademarks of Chicago Mercantile Exchange Inc. CBOT and the Chicago Board of Trade are trademarks of the Board of Trade of the City of Chicago. NYMEX, New York Mercantile Exchange, and ClearPort are trademarks of New York Mercantile Exchange, Inc. COMEX is a trademark of Commodity Exchange, Inc. CME Group is a trademark of CME Group Inc. All other trademarks are the property of their respective owners. The information within this presentation has been compiled by CME Group for general purposes only. CME Group assumes no responsibility for any errors or omissions. Additionally, all examples in this presentation are hypothetical situations, used for explanation purposes only, and should not be considered investment advice or the results of actual market experience. All matters pertaining to rules and specifications herein are made subject to and are superseded by official CME, CBOT, and NYMEX rules. Current rules should be consulted in all cases concerning contract specifications. © 2011 CME Group. All rights reserved 2 Objective and Scope of Analysis • To better understand the changing relationship between Power and Natural Gas. • Analyzing the seasonal effect and trend of natural gas price on power price. • Completed analysis for multiple ISOs – MISO, PJM, ISO NE and ERCOT. • Used a Bayesian Statistical model to complete analysis. © 2011 CME Group. All rights reserved 3 Why use Bayesian Statistics with this Analysis? • Simply, the relationship between power and natural gas has been changing. • A major strength of this type of Bayesian statistical model is that it captures changing dynamics between variables. © 2011 CME Group. All rights reserved 4 MISO Analysis Dynamic Linear Model Regression Parameter representing the influence of Natural Gas price on Power price is unknown. Estimation Equation Powert= Constant + Natural Gast + errort © 2011 CME Group. All rights reserved 5 Dynamic Linear Model (DLM) • Dynamic models allow time varying coefficient estimates. • Sequential analysis allows for updating of coefficients as new information is observed. • Compare: OLS Regression - One set of coefficient estimates for whole time period. DLM – Relationship of variable X on Y can change and vary over time. DLM estimates capture this change. © 2011 CME Group. All rights reserved 6 Data Natural Gas • ANR Gas Daily Prices (Platts). Power • Cinergy Average LMP data (until Feb-28-2011). • Indiana Hub (Mar-1-2011). • Data from April 2005 to April 2013. • Model uses Daily Price Percent Change series for both Power and Natural Gas. © 2011 CME Group. All rights reserved 7 Seasonal Trend Decomposition (STL) • Breaks a time series into Trend and Seasonal components. • Done by LOESS (Locally Weighted Regression). • Smoothing algorithm which fits a locally weighted polynomial – linear or quadratic. • Decomposed the Total Effect of Natural Gas Price on Power Price (Coefficient – βt) into components. βt = Trendt + Seasonalt + Remaindert © 2011 CME Group. All rights reserved 8 MISO: Seasonal Effect Seasonal Effect of Natural Gas Price in Influencing Power Price Seasonal Component of Beta Coefficient 0.4 0.3 Summer Winter 0.2 0.1 0.0 ‐0.1 ‐0.2 ‐0.3 ‐0.4 Source: ANR Gas prices and Indiana Hub data from NrgStream. Bayesian DLM Model by CME Economics. © 2011 CME Group. All rights reserved 9 MISO: Varying Effect of Natural Gas Price Trend Line of Natural Gas Price Affecting Power Price Trend Component of Beta Coefficient 1.4 1.2 1.0 0.8 0.6 0.4 0.2 0.0 Source: ANR Gas prices and Indiana Hub data from NrgStream. Bayesian DLM Model by CME Economics. © 2011 CME Group. All rights reserved 10 MISO: Remainder Remainder Effect Remainder Component of Beta Coefficient 1.0 0.8 0.6 0.4 0.2 0.0 ‐0.2 ‐0.4 ‐0.6 ‐0.8 ‐1.0 Source: ANR Gas prices and Indiana Hub data from NrgStream. Bayesian DLM Model by CME Economics. © 2011 CME Group. All rights reserved 11 Results Seasonal • Seasonal pattern shows strong summer peak and weaker winter peak. Trend • Shows varying but overall increasing influence of Natural Gas price on Power price. • Trend is disturbed due to financial crisis turmoil (many correlations fell to zero in that period). Remainder • Appears to be white noise - implying seasonal and trend breakdown fit data. • Any large spike in remainder implies influence of different factor than Gas price in greatly affecting Power price. © 2011 CME Group. All rights reserved 12 Comparisons to other ISOs ERCOT • ERCOT Power Houston Hun (NrgStream) • Houston Ship Channel Gas (Platts) • Data from Nov 2008 – Dec 2012 PJM • PJM Monthly Peak Futures Contract (DM1 Bloomberg) • Henry Hub Gas Futures (NG1 Bloomberg) • Data from May 2003 – Aug 2012 ISO NE • ISO NE Internal Hub Daily Average Peak Day Ahead Price (NrgStream) • Algonquin Daily Next Day Natural Gas Prices (Platts) • Data from Jan 2004 – Aug 2012 © 2011 CME Group. All rights reserved 13 ERCOT Seasonal Effect: Strong Summer Peak Seasonal Effect of Natural Gas Price in Influencing Power Price Seasonal Component of Beta Coefficient 1 Summer 0.8 0.6 0.4 0.2 0 ‐0.2 ‐0.4 ‐0.6 ‐0.8 Source: Houston Ship Channel Gas prices from Platts and ERCOT Power Houston Hub from NrgStream. Bayesian DLM Model by CME Economics. © 2011 CME Group. All rights reserved 14 PJM Seasonal Effect: Strong Summer Peak Seasonal Effect of Natural Gas Price in Influencing Power Price Seasonal Component of Beta Coefficient 0.25 Summer 0.20 0.15 0.10 0.05 0.00 ‐0.05 ‐0.10 Spring ‐0.15 4/2003 4/2004 4/2005 4/2006 4/2007 4/2008 4/2009 4/2010 4/2011 4/2012 Source: Data from Bloomberg Professional. Bayesian DLM Model by CME Economics. Note: Seasonal Analysis used PJM Power Futures and Henry Hub Gas Futures © 2011 CME Group. All rights reserved 15 ISO New England Seasonal Effect: Natural Gas Influence Heightened in Summer and Winter 2.0 Seasonal Effect of Natural Gas Price in Influencing Power Price ‐ ISO NE Seasonal Component of Beta Coefficient Winter Summer 1.5 1.0 0.5 0.0 ‐0.5 ‐1.0 ‐1.5 3/2009 9/2009 3/2010 9/2010 3/2011 9/2011 3/2012 Source: Data from Bloomberg Professional. Bayesian DLM Model by CME Economics. © 2011 CME Group. All rights reserved 16 ERCOT: Increasing Influence of Natural Gas Price since 2008 Trend Line of Natural Gas Price Affecting Power Price Trend Component of Beta Coefficient 2.0 1.5 1.0 0.5 0.0 ‐0.5 ‐1.0 Source: Data from Platts and NrgStream. Bayesian DLM Model by CME Economics. © 2011 CME Group. All rights reserved 17 PJM: Increasing Influence of Natural Gas Price since 2009 Trend Line of Natural Gas Price Affecting Power Price Trend Component of Beta Coefficient 0.7 0.6 0.5 0.4 0.3 0.2 0.1 0.0 ‐0.1 4/2003 4/2004 4/2005 4/2006 4/2007 4/2008 4/2009 4/2010 4/2011 4/2012 Source: Data from Bloomberg Professional. Bayesian DLM Model by CME Economics. Note: Seasonal Analysis used PJM Power Futures and Henry Hub Gas Futures © 2011 CME Group. All rights reserved 18 ISO NE: Increasing Influence of Natural Gas Price since 2005 Trend Line of Natural Gas Price Affecting Power Price Trend Component of Beta Coefficient 0.45 0.35 0.25 0.15 0.05 ‐0.05 ‐0.15 Source: Data from Platts and NRG Stream. Bayesian DLM Model by CME Economics. © 2011 CME Group. All rights reserved 19 ERCOT Remainder Component: Remainder Component of Beta Coefficient 2.0 Remainder Effect 1.0 0.0 ‐1.0 ‐2.0 Source: Data from Platts and NrgStream. Bayesian DLM Model by CME Economics. © 2011 CME Group. All rights reserved 20 Comparison among ISOs Seasonal • Seasonal pattern is distinct to each ISO: • ERCOT exhibits a strong seasonal peak for summer. • MISO and ISO NE exhibits seasonal peaks for Winter AND Summer. • PJM exhibits slight seasonal summer peak. Trend • ISO NE and PJM show an increasing influence of Natural Gas price on Power price starting in 2005. • MISO and PJM shows the effect of the financial panic in 2008, causing correlations to move temporarily to zero – ISO NE and ERCOT do not. Remainder • ISO NE: Remainder is generally white noise, but with large spikes. • PJM: Remainder is purely white noise. © 2011 CME Group. All rights reserved 21 Next Steps ISO • Analyze additional ISOs. Addressing Other Fuel Sources • Coal • Method to capture impact of Wind? (Relevant to MISO) Level of Review • Analysis addressed most visible price relationship in ISO • Potential sub-regions within ISOs • Most relevant sub-regions? © 2011 CME Group. All rights reserved 22 Appendix Bayesian Statistics and Model Equations Frequentist vs. Bayesian Statistics Key Difference: The way “Uncertainty” is treated Frequentist: Uncertainty about quantities or parameters estimated is captured by looking at how estimates would change in repeated sampling from the same population (or data set). Bayesian: Uncertainty is addressed by updating prior opinions about quantities and parameters estimated as NEW data is observed. © 2011 CME Group. All rights reserved 24 Bayesian Statistics Bayes’ Theorem © 2011 CME Group. All rights reserved 25 Bayesian Analysis PRIOR x LIKELIHOOD POSTERIOR • Prior – Initial probability distribution of parameters • Likelihood – Joint probability of observing the data given the parameters estimated • Posterior - Probability of parameters given the data • The process of moving from Prior to Posterior is called Bayesian Learning © 2011 CME Group. All rights reserved 26 Model General The DLM is a two equation system estimated as: Estimation Equation Yt=(Ft)’ βt + vt • vt ~ N[0,Vt] Where F are the explanatory factors and β are the Beta parameter estimates State Equation βt =Gt βt-1 + wt • wt ~N[0,Wt] Governs the path of Beta Estimates changing over time © 2011 CME Group. All rights reserved 27 Model – MISO Analysis Estimation Equation 1. Powert= β0t * Constant + β1t * Natural_Gast + et • β is a vector of the estimated Beta coefficients et is the error term • State Equation 2. βt =Gt βt-1 + gt • Estimated beta coefficients may change over time as allowed by the State Equation • gt is the error term © 2011 CME Group. All rights reserved 28 DLM Code Part I – Initial Information • Set mean and variance of the Prior Distribution for Period 0, this information acts as starting values for model. Part II – Create Placeholders • Create “placeholder” vectors and matrices for all the components of the function. The placeholders are filled in as the function runs and repeats the steps for each time period. © 2011 CME Group. All rights reserved 29 DLM Code II Part III –Loop • Loop repeats the steps of the function for every time period Steps 1. Posterior at t-1 (βt-1|Dt-1)~N[mt-1,Ct-1] 2. Prior at t (βt|Dt-1)~N[at,Rt] 3. Next-step ahead forecast (Yt|Dt-1)~N[ft,Qt] 4. Posterior at t (βt|Dt)~N[mt,Ct] © 2011 CME Group. All rights reserved 30 DLM Code III • Steps 1 - 4 of the loop update the Distribution of parameters, hence the 2 moments which characterize each Normal distribution are calculated and updated. • The Mean and Standard Deviation estimate from the Posterior distribution at time t are used as the final output of Beta coefficients and Standard Errors of the model. © 2011 CME Group. All rights reserved 31 Other Applications • Federal Reserve Policy • Dynamic Volatility Estimation • Natural Gas Price and Power Price • Brazilian GDP Forecasting • FX Models © 2011 CME Group. All rights reserved 32 Observing the Changing Relationship Between Natural Gas Prices and Power Prices The research views expressed herein are those of the author and do not necessarily represent the views of the CME Group or its affiliates. All examples in this presentation are hypothetical interpretations of situations and are used for explanation purposes only. This report and the information herein should not be considered investment advice or the results of actual market experience. Samantha Azzarello Economist, CME Group April 2013