Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Modern Monetary Theory wikipedia , lookup

Full employment wikipedia , lookup

Economic bubble wikipedia , lookup

Production for use wikipedia , lookup

Edmund Phelps wikipedia , lookup

Balance of payments wikipedia , lookup

Economic democracy wikipedia , lookup

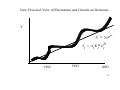

Fiscal multiplier wikipedia , lookup

Monetary policy wikipedia , lookup

Nominal rigidity wikipedia , lookup

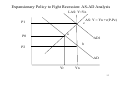

Non-monetary economy wikipedia , lookup

Ragnar Nurkse's balanced growth theory wikipedia , lookup

Long Depression wikipedia , lookup

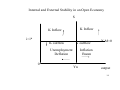

Money supply wikipedia , lookup

Economic calculation problem wikipedia , lookup

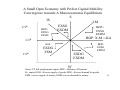

Stagflation wikipedia , lookup

Post-war displacement of Keynesianism wikipedia , lookup

Macroeconomic Theory and Policy Lecture 7 Macroeconomic Equilibrium: IS-LM and AD-AS Analysis 1 What is macroeconomic equilibrium? Is an Economy always in equilibrium? Macroeconomic general equilibrium is characterised by • prices that clear goods markets • wage rates that clear labour markets • interest rates that clear the capital markets • exchange rates that clear the foreign exchange markets • Disequilibrium may result when these prices are not free to change because of institutional or policy reasons. • IS-LM model explains how such disequilibrium (Gaps between Demand and supply) may exist and could be mitigated using deliberate policy actions. 2 Micro-Foundation to Macro: General Equilibrium with a representative household and firm Market p and w such that Y=C Wage payment, wL LD = LS LS +L = Lbar KD =KS Labour supply, L Trade Px X-PmM= CA CA+KA =0 Government Households Max U(C,L) Economy ROW Payments for goods Max U = c φ l 1−φ l + h =1 s pc = wh s + π c ≥ 0; l ≥ 0; h s ≥ 0 Supply of Goods G =T = t*Y +tw*wL+tr+rk Firms Max π(LS) Max π = py − wh d ( ) y≤ h d α y ≥ 0; h ≥ 0 d 3 Classical view • Ideas of Adam Smith (1776), Ricardo (1817), J. B. Say, Malthus (182) Mill (1873), Marshall (1925) • Invisible hand sets prices to equate demand and supply. • No excess demand or no excess supply can persist. No glut or shortages in goods market. • No unemployment or labour pressure in the labour market. • Money is neutral (quantity theory of money). • Prices proportional to money supply. • It is long run view. • Balance budget recommended. • Laisser faire: minimum government is the best government. • Downward sloping aggregate demand and vertical supply curve 4 Classical economy: How perfectly flexible prices guarantee macroeconomic equilibrium in IS-LM Framework AS M(D) IS LD i i=i* W LM LS L IS-LM: goods and money Labor market Money market (M/P) F(Y) Y P Y Output L Output to output , Y Price level and money supply 5 Keynesian Revolution (Short run analysis) • Gaps between supply and demand may persist for a log time. • Markets (prices) may not work automatically itself because of deficiency in demand: massive unemployment labour and under utilisation of capital is possible. • Cost of waiting to return to the natural level; irresponsible to do so. • Balancing budget is stupid and dangerous policy. • Active role by government can mitigate deficiency in private demand (consumption and investment). • Positive role of fiscal policy and monetary policy. • Multiplier effect of demand on output • Aggregate supply is horizontal in the short run. • Animal spirits – importance of expectations. 6 Keynesian economy: flexed prices and possibility of underemployment equilibrium IS LD S i i=i* W M(D) LM LM LS L IS-LM: goods and money Labor market Money market (M/P) F(Y) P Y Y Output L Output to output , Y Price level and money supply 7 Open Economy Model: Equilibrium in Six Different Markets Balance of Payment analysis: Graphical approach Labour Market LD LS Goods and Money Money market IS AS LM MD MS Wage i Domestic bonds BS BD i Foreign Bonds i* Foreign Exchange i Interest rt L Y M/P DB FB exchange rate Output Y Employment Output P Price Real money balance Portfolio allocation e 8 Keynesian Economist’s view on Economic Policy • Automatic equilibrium is not guaranteed. Animal spirits not the rational choices dominate the economy. • Unemployment may persist for a long period if the deficiency in demand continues. • Active policy can play a very positive role, because of rigidity in the markets, particularly in the labour market (minimum wage laws, unions, and efficiency wages). • Also because of the monopolistic powers of the firms. • Active policy can fine tune the economy and correct the market failure. 9 New Classical View of Fluctuation and Growth an Dconomy Y yt = y0 e gt β Y = A Kα L t t t t 1982 1992 2003 10 LAS RE i3 i2 i1 LM(P2) LM1(P1) LM (P0) IV Price Feedback: Monetarists III II: LM curve: Hicksian Crowding out i0 I: IS curve IS1 IS0 o y0 y1 y2 y3 A Simple Overview of Keynesian, Monetarist and New Classical and New Keynesian Approaches to Analysis of short run fluctuations 11 Summary of Four Macro Models in the above Figure • Government expenditure rises IS1 shifts to IS2. Impact on output and interest rates differ across macroeconomic models. • Models I and II are Keynesian and new Keynesian models. • Model IIIA is monetarists includes a price feedback. AD drops as real balances decline. • Model IV monetarist proposition in the long run and New Classical model with rational expectation. 12 Expansionary Policy to Fight Recession: AS-AD Analysis LAS: Y=Yn P1 c a P0 AS: Y = Yn +v(P-Pe) AD1 b P2 AD Yr Yn 13 How does output responds to positive demand and supply shocks in the long run? Dynamic adjustment process of expansionary monetary and fiscal policy AD2 LAS AD1 D SAS P c b a M Y = F ( , G, T ) P Yn Y Aggregate demand and aggregate supply Dynamic adjustment process after a positive supply shocks P = (1 + μ ) P e N s ( 1 − Y ; z) L a P b C AS1 AS2 AD AS3 Yn Y Aggregate demand and aggregate supply in the short and the medium run 14 How does output and prices respond to a negative demand and supply shocks in the long run? Dynamic adjustment process of contractionary monetary and fiscal policy SAS AD a Dynamic adjustment process after a negative supply shocks (increase in oil prices) P c b P B a c Yn Y Aggregate demand and aggregate supply Yn Y Aggregate demand and aggregate supply in th short and the medium run 15 Internal and External Stability in an Open Economy S K Inflow K Inflow i=i* K outflow K outflow Unemployment Deflation 0 X-M=0 Inflation Boom Yn output 16 Macroeconomic Equilibrium in a Small Open Economy with Perfect Capital Mobility S IS LM i>i* BOP+ K inflow BOP+ Boom K-inflow Deflation BOP: X-M =-KA i=i* BOP- Outflow Boom/inflation Over full employment BOPK-outflow Deflation i<i* Under full employment. Yf 17 A Small Open Economy with Perfect Capital Mobility: Convergence towards A Macroeconomic Equilibrium S IS LM EXSG i>i* BOP+ BOP+ EXDM EXSG EXDG EXSM EXDM BOP: X-M =-KA i=i* BOP- i<i* EXDG ESM EXDG EXDM BOPEXSG EXDM Yf Notes: YF full employment output, BOP = Balance of Payment, K= capital, ESG =Excess supply of goods, EDG =Excess demand for goods, ESM =excess supply of money, EDM=excess demand for money 18 Macroeconomic Equilibrium in a Small Open Economy with Imperfect Capital Mobility S IS LM i>i* BOP+ K inflow BOP+ K-inflow Deflation Boom BOP: NX(e(r,y)) i=i* BOP- Outflow Boom/inflation Over full employment BOPK-outflow Deflation i<i* Under full employment. Yf 19 Numerical Exercises • Fixed Price Model IS-LM model • Flexible Price IS-LM Model • Multiplier Analysis in Keynesian Model • Open Economy Macro Economic Model – With perfect capital mobility – Imperfect capital mobility 20 References • • • • • • • • • • • • • • • • • • • • • • Bhattarai (2002) Interest Rate Determination in the UK: Test of the Taylor Rule University of Hull. Fleming J. Marcus (1962) Domestic financial policies under fixed and under floating exchange rates, IMF staff paper 9, November , 369-379. Friedman, M. (1968), "The Role of Monetary Policy," American Economic Review, No.1 vol. LVIII March Hicks, J. R.(1937): Mr. Keynes and the "Classics"; A Suggested Interpretation, Econometrica 5: pp 147-159. Krugman P. and L. Taylor (1978) “Contractionary Effects of Devaluation” Journal of International Economics, 44556. Lucas, Robert Jr. and Sargent, After Keynesian Macroeconomics, Spring 1979, Federal Reserve Bank of Monneapolis Quarterly Review. Mankiw N.G. (1989) Real Business cycle: A New Keynesian Perspective, Journal of Economic Perspectives, vol. 3, no. 3 pp. 79-90. Miller, Marcus; Salmon, Mark When Does Coordination Pay? Journal of Economic Dynamics and Control, July-Oct. 1990, v. 14, iss. 3-4, pp. 553-69 Mundell R. A (1962) Capital mobility and stabilisation policy under fixed and flexible exchange rates, Canadian Journal of Economic and Political Science, 29, 475-85. Nordhaus WD (1994) Policy Games: Co-ordination and Independence in Monetary and Fiscal Policies, Brookings Papers in Economic Activities, pp. 139-216. Phillips A W. (1958) The relation between unemployment and the rate of change of money wage rates in the United Kingdom, 1861-1957. Phelps E. S. (1968) Money wage dynamics and labour market equilibrium, Journal of Political Economy, 76 , 678-711. Sebastian E (1986) Are Devaluations Contractionary? Review of Economics and Statistics, vol. 68, 3, 501-508. G.K.Shaw, M. J. McCrostie and D. Greenaway (2001) Macroeconomics: Theory and Policy in the UK, Blackwell. Shaw, McCrostie and Greeenaway (2001) Macroeconomics Theory and Policy in the UK, Blackwell. Taylor Mark (1995) The Economics of Exchange Rates, Journal of Economic Literature, March, vol 33, No. 1, pp. 13-47. 21