Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

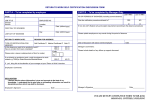

COST - BENEFITS ANALYSIS OF OCCUPATIONAL HEALTH AND SAFETY MANAGEMENT IN THE ENTERPRISES Jan Rzepecki, Ph. D. Central Institute for Labour Protection 00-701 Warsaw, Czerniakowska 16, Poland e-mail: [email protected] phone (+4822) 623-46-69 Introduction Economic studies on OHS at company level should include both, current as well as projected cost - benefit analyses because they facilitate the planning of prevention activities in such a way as to ensure the highest possible efficiency at the lowest cost. Method Supported by information technology software, a CBA model has been developed at Central Institute for Labour Protection in Warsaw. It takes into account the following of the OHS cost items: (Fig. 1). Accident insurance premiums Costs of accidents and occupational diseases Costs of absenteeism Costs of overtimes Decreased productivity Benefits due to work in harmful and noxious conditions Costs of prevention Figure 1. The main sources of OHS costs OHS costs Working environment The CBA model facilitates the entering and calculating of specific OHS items listed in Fig. 1 Thanks to the software, it is possible to calculate the cost of two major types of accidents, those involving injuries and near – accidents, which is based on the form on work accident cost items. (Fig. 2). ....................................................................................................... Company Subsequent number of accident THE FORM ON WORK ACCIDENT COST ITEMS Date of accident: Time: Division / Unit: Type of accident consequence: Division code: - injury (-ies) of a worker without property loss - injury (-ies) of a worker with property loss - accident leading only to property loss Brief description of the accident and incurred or potential property loss First and family name of the injured person: I. Control No: WORKING TIME LOST FOLLOWING THE ACCIDENT No. Persons A. On the day of the accident: 1. Injured person 2. Person organising first aid 3. Person providing first aid at the accident site 4. Person in charge of re-arranging work 5. Number of persons Time (hours) Wage cost (hourly rate) Cost Other persons Cost of time lost on the day of accident B. Injured person’s absence period C. Time spent on accident investigation: 1. Supervision personnel 2. Accident witness(-es) 3. Other persons Cost of time spent on accident investigation D. Planning and time spent on the implementation of preventive measures and prophylaxis 1. Manager 2. Supervision personnel 3. Technical construction or technology engineer 4. Other Time spent on planning and research-development activities E. Other (for e.g. time to re-train the replacement worker or the injured person upon return to work etc.) 1. 2. 3. Other costs - Subtotal COST OF TIME LOST DUE TO ACCIDENT II. MEDICAL AID AND TRANSPORT COST OF TRANSPORTING THE INJURED PERSON HOME / TO THE DOCTORS Working time of medical personnel at the in-house medical unit Dressing materials and medication used at the in-house medical unit Cost of external medical care Other items Cost of medical transport and aid III OVERTIME No. Worker Working time (hours) Wage cost (hourly rate) Cost Wage cost (hourly rate) Cost Overtime on the day of accident 1. 2. Overtime during the absence of the injured person 1. 2. COST OF OVERTIME: IV. REPLACEMENTS No. Replacement Working time (hours) Replacement on the day of accident 1. 2. Replacement during the absence of the injured person 1. 2. COST OF REPLACEMENT: V. PRODUCTION DISTRUBANCES No 1. 2. 3. 4. 5. 6. 7. Type of disturbance Duration of disturbance Cost of disturbance Cost Production stopped at the division Production stopped at other divisions Revenue losses due to reduced productivity revenue losses due to lower production output quality Production assigned to sub-contractor Machine rent Other COST OF PRODUCTION DISTRUBANCES VI. PROPERTY LOSSES Type of losses 1. Consumed raw materials 2. Destroyed intermediate products 3. Destroyed finished products 4. Lost value of machines and equipment 5. Lost value of vehicles 6. Purchase of new machines and equipment 7. Purchase of new vehicles 8. Other losses COST OF PROPERTY LOSSES Cost VII. . REPAIRS Repairs made in house No Type of repair Number of workers Working time (hours) Wage cost (hourly rate) Cost 1. 2. Repairs done by sub-contractors: No. Type of repair Cost 1. 2. COST OF REPAIRS VIII. COMPENSATIONS No Type of benefit Cost 1. Single compensations 2. Compensation benefits 3. Compensation allowances due to transfer to other work place 4. Compensation allowances due to vocational rehabilitation 5. Compensation due to the loss of personal property items 6. Funeral allowance 7. Fatality payment 8. Death compensation payment 9. Others COST OF COMPENSATIONS IX. OTHER COST ITEMS No 1. Cost item description Cost Contractual fines 2. Other cost - total COST OF ACCIDENT X. No INDEMNITIES RECEIVED BY THE COMPANY FROM INSURANCE INSTITTUTIONS Indemnities due to property losses (specified as items in section 4) Amount 1. 2. TOTAL INDEMINITIES COST OF ACCIDENT NAME OF PERSON FILLING THE FORM: First and family name ........................................ Date ......................................................... Position ....................................................................... Signature................................................... Figure 2. The Form on Work Accident Costs After the user has entered relevant prevention data, the software calculates the following cost items: OHS staff employment; Purchase and maintenance of collective protective equipment; Purchase and maintenance of personal protective equipment; Purchase and maintenance of protective clothing; Cleaning materials; Audits; Medical examination; OHS training; Working environment measurements; Rescue teams and fire fighting services; Promotion and information; Fines and penalties. CBA Model enables the development of projection studies as well as the calculation of estimated benefits by the way of deducting certain cost items that have been as calculated before and after taking the prevention measures in question to improve working conditions in the company or selected department. Moreover, it enables the verification of projections that have been made. Return on investment provides the basis for comparison between various options of projected investment. The return on investment is calculated in the following way: prevention (increase of inputs) Period of return (months) = ------------------------------------------ x 12 profits (savings) Results In a pilot project, the CBA model was checked in four companies, where, on the average, total inputs on prevention measures (including the cost of OHS staff employment) accounted for 0.48% of the total cost. The share of such inputs in specific companies varied from 0.18% to 0.84% of total cost. If compared to the total prevention expenses, the share of working clothes was considerable (47%), and so was that of the item comprising personal protection devices (28%). The aim of pilot project was the verification of a function related to making projections on the expected benefits of investment projects to improve working conditions. In two companies tested to verify the CBA model, the basic investment projects included inputs to provide collective protection i.e. improved system of ventilation in a ship building company (enterprise A) and noise reducing measures in a production hall in a chemical company (enterprise B). The investment projects in question were limited to departments, where the share of employment was below 5% of the total. In the two other enterprises, the investment projects affected the whole of a company. They comprised construction of a new building (enterprise C) and replacement of old window frames in a SME (enterprise D) unit employing 11 workers. (Table ). When analysing cost and benefits according to the CBA in question, it was assumed that the basic benefits resulting from investment projects would include a reduced number of days on sick leaves and enhanced work efficiency. Results of Cost-Benefit Analysis according to CBA model. Enterprise Number of employees Total cost (in PLN’000) Cost of investment project (in PLN’000) 36,0 Investment project as percentage of total cost 0,008% Benefits thanks to investment project in one year 232,0 Period of return on investment (in moths) 2 A 2 502 454 168,0 B 2 907 535 375,3 60,0 0,011% 11,4 63 C 1 059 63 733,2 8 000,0 12,552% 4 165,9 23 D 11 1 097,0 22,0 2,005% 1,3 205 Conclusions CBA Model enables the monitoring of OHS costs and benefits. Thus, it provides the basis for assessing both, the effectiveness of OHS management system implementation as well as that of specific activities to improve work conditions. The results of research work indicate that there are considerable differences amongst expected benefits and return on investment envisaged in the companies included in the pilot project. In large companies, the analysis of benefits as a result of a single investment project can be particularly useful at a department level because it seldom occurs that investment projects are implemented to improve working conditions in the whole company . The most notable benefits from investment projects improving work conditions have been obtained in companies with high concentration of working stations and a large number of manual operations. References 1. 2. 3. Oxenbourgh M. S., Marlow P. S.: Economic models for Ergonomists. International encyclopaedia of ergonomics and human factor. Edited by W. Karwowski. London, Taylor & Francis 2000. Pawłowska Z., Rzepecki J. : The proposed method of calculating the cost of occupational accidents in the company. European Conference on Costs and Benefits of Occupational Safety and Health 1997. The Hague, 28-30 May 1997 Pawłowska Z., Rzepecki J.: Impact of Economic incentives on costs and benefits of occupational health and safety. International Journal of Safety and Ergonomics. Special Issue 2000, 71-83.