Chapter 10

... dividend. The shareholder owns exactly the same proportion of the company before and offer the stock dividend, but the ownership is divided into a larger number of shares. KNOWLEDGE CHECK 10.3 What is leverage? ...

... dividend. The shareholder owns exactly the same proportion of the company before and offer the stock dividend, but the ownership is divided into a larger number of shares. KNOWLEDGE CHECK 10.3 What is leverage? ...

Netherlands Tax Alert

... acquired a Dutch target though a loan. Through a complex multi-step refinancing transaction, the borrower then contributed the Dutch target in return for the common shares of a Dutch special purpose vehicle (SPV) and the banking syndicate acquired cumulative preference shares (CPS) in the SPV to rep ...

... acquired a Dutch target though a loan. Through a complex multi-step refinancing transaction, the borrower then contributed the Dutch target in return for the common shares of a Dutch special purpose vehicle (SPV) and the banking syndicate acquired cumulative preference shares (CPS) in the SPV to rep ...

Utilizing Capital Loss Carry-Forwards - Twenty

... cannot be carried back. A $3,000 annual deduction against ordinary income is allowed, but after that losses not used to offset gains are carried forward. For many investors today, losses realized easily can exceed the amount of gains expected in the foreseeable future. Investors can tilt investments ...

... cannot be carried back. A $3,000 annual deduction against ordinary income is allowed, but after that losses not used to offset gains are carried forward. For many investors today, losses realized easily can exceed the amount of gains expected in the foreseeable future. Investors can tilt investments ...

Corporate Class: Tax-efficient Investing

... strategies available as of the date indicated and is not intended to be comprehensive investment advice applicable to the circumstances of the individual and should not be considered as personal investment advice or an offer or solicitation to buy or sell securities. This should not be construed to ...

... strategies available as of the date indicated and is not intended to be comprehensive investment advice applicable to the circumstances of the individual and should not be considered as personal investment advice or an offer or solicitation to buy or sell securities. This should not be construed to ...

TAXATION - PBworks

... A good tax system should adhere to certain principles which become its characteristics. A good tax system is therefore based on some principles. Adam Smith has formulated four important principles of taxation. A few more have been suggested by various other economists. These principles which a good ...

... A good tax system should adhere to certain principles which become its characteristics. A good tax system is therefore based on some principles. Adam Smith has formulated four important principles of taxation. A few more have been suggested by various other economists. These principles which a good ...

POLICY CHANGES AT A GLANCE 20 th March 2013

... Limited extension of the capital gains tax holiday to continue to encourage investors to take up the Seed Enterprise Investment Scheme. Any investors making capital gains in 2013/14 will receive a 50 per cent capital gains tax relief when they reinvest those gains into seed companies in either 2013/ ...

... Limited extension of the capital gains tax holiday to continue to encourage investors to take up the Seed Enterprise Investment Scheme. Any investors making capital gains in 2013/14 will receive a 50 per cent capital gains tax relief when they reinvest those gains into seed companies in either 2013/ ...

Legal Forms of Organization

... Limited liability of shareholders Issue different classes of stock Raise capital by selling stock More status Benefit from retirement funds, ...

... Limited liability of shareholders Issue different classes of stock Raise capital by selling stock More status Benefit from retirement funds, ...

Summary of Tax Provisions in the Emergency Economic

... otherwise allowable section 901 foreign tax credit for combined foreign oil and gas extraction income (“FOGEI”), which relates to upstream production to the point the oil leaves the wellhead, and foreign oil related income (“FORI”), which is defined as all downstream processes once the oil leaves th ...

... otherwise allowable section 901 foreign tax credit for combined foreign oil and gas extraction income (“FOGEI”), which relates to upstream production to the point the oil leaves the wellhead, and foreign oil related income (“FORI”), which is defined as all downstream processes once the oil leaves th ...

Here

... finance ministers to get moving on it – EU seems very ready to do something – Danish Left promise to introduce one if successful in upcoming elections – … and there’s more good news everyday ...

... finance ministers to get moving on it – EU seems very ready to do something – Danish Left promise to introduce one if successful in upcoming elections – … and there’s more good news everyday ...

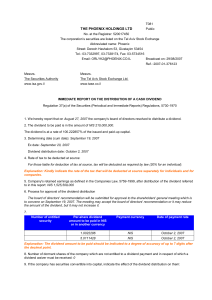

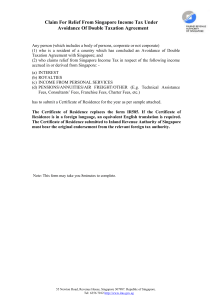

Certificate of Residence from Non-Residents

... The Certificate of Residence submitted to Inland Revenue Authority of Singapore must bear the original endorsement from the relevant foreign tax authority. ...

... The Certificate of Residence submitted to Inland Revenue Authority of Singapore must bear the original endorsement from the relevant foreign tax authority. ...

Finding Just the Right Tax Rate

... parent company. The foreign parent no longer pays taxes on the foreign profits it repatriates to the United States, whether they are invested in plant and equipment or paid out in dividends to shareholders. The foreign parent also escapes rules that limit the ability of U.S.-based firms to shift rep ...

... parent company. The foreign parent no longer pays taxes on the foreign profits it repatriates to the United States, whether they are invested in plant and equipment or paid out in dividends to shareholders. The foreign parent also escapes rules that limit the ability of U.S.-based firms to shift rep ...