Basic Cost Management Concepts

... Another term for product cost is inventoriable cost, since a product cost is stored as the cost of inventory until the goods are sold. In addition to retailers, wholesalers, and manufacturers, the concept of product cost is relevant to other producers of inventoriable goods. Agricultural firms, lumb ...

... Another term for product cost is inventoriable cost, since a product cost is stored as the cost of inventory until the goods are sold. In addition to retailers, wholesalers, and manufacturers, the concept of product cost is relevant to other producers of inventoriable goods. Agricultural firms, lumb ...

IAS 2 - Inventories

... bringing the inventories to their present location and condition. For example, it may be appropriate to include non-production overheads or the costs of designing products for specific customers in the cost of inventories. 16. Examples of costs excluded from the cost of inventories and recognised as ...

... bringing the inventories to their present location and condition. For example, it may be appropriate to include non-production overheads or the costs of designing products for specific customers in the cost of inventories. 16. Examples of costs excluded from the cost of inventories and recognised as ...

fixed cost

... Note: The discretionary fixed costs have no obvious relationship to levels of output activity. The amount spent can be changed at the discretion of management. The planned amounts of discretionary costs are negotiated between the manager and his superior during the budget process. ...

... Note: The discretionary fixed costs have no obvious relationship to levels of output activity. The amount spent can be changed at the discretion of management. The planned amounts of discretionary costs are negotiated between the manager and his superior during the budget process. ...

Lecture 7_Management accounting in SMEs

... alternative decisions, or of a change in output levels. The concept is used when there are multiple possible options to pursue, and a choice must be made to select one option and drop the others. Within this category: a) Sunk Costs - Costs incurred in the past, not modifiable in the short term - Not ...

... alternative decisions, or of a change in output levels. The concept is used when there are multiple possible options to pursue, and a choice must be made to select one option and drop the others. Within this category: a) Sunk Costs - Costs incurred in the past, not modifiable in the short term - Not ...

Chapter 7 - Kennisbanksu

... Ù Using allocation bases that are not cost drivers needs to be handled with extreme caution continued Copyright 2003 McGraw-Hill Australia Pty Ltd, PPTs t/a Management Accounting: An Australian Perspective 3/e by Langfield-Smith, Thorne & Hilton Slides prepared by Kim Langfield-Smith ...

... Ù Using allocation bases that are not cost drivers needs to be handled with extreme caution continued Copyright 2003 McGraw-Hill Australia Pty Ltd, PPTs t/a Management Accounting: An Australian Perspective 3/e by Langfield-Smith, Thorne & Hilton Slides prepared by Kim Langfield-Smith ...

continued 7-3 What are overhead costs?

... assist in planning and control activities To form part of the predetermined overhead rates used to cost products Allocation methods include – Direct: support departments costs are allocated directly to production departments – Step-down: partially recognises the services provided by one support depa ...

... assist in planning and control activities To form part of the predetermined overhead rates used to cost products Allocation methods include – Direct: support departments costs are allocated directly to production departments – Step-down: partially recognises the services provided by one support depa ...

Analysis and Interpretation of Financial Statements

... Marginal costing is not a distinct method of costing like job costing, process costing, operating costing, etc. but a special technique used for marginal decision making. Marginal costing is used to provide a basis for the interpretation of cost data to measure the profitability of different product ...

... Marginal costing is not a distinct method of costing like job costing, process costing, operating costing, etc. but a special technique used for marginal decision making. Marginal costing is used to provide a basis for the interpretation of cost data to measure the profitability of different product ...

PRICING SCHEDULE A

... Other 1 ____________________________________ Other 2 ____________________________________ Other 3 ____________________________________ ...

... Other 1 ____________________________________ Other 2 ____________________________________ Other 3 ____________________________________ ...

null

... Multiproduct Analysis Management expects to sell 9 prints at $.60 each for every enlargement it sells at $1.00. ...

... Multiproduct Analysis Management expects to sell 9 prints at $.60 each for every enlargement it sells at $1.00. ...

Costs

... Material Y left from last year’s Lunar New Year Fair was purchased at $22,000. It is a popular material. If used up, it has to be replaced at ...

... Material Y left from last year’s Lunar New Year Fair was purchased at $22,000. It is a popular material. If used up, it has to be replaced at ...

Marginal Costing vs. Absorption Costing Revision

... • Product costs are built up using absorption costing by a process of allocation apportionment and absorption. ...

... • Product costs are built up using absorption costing by a process of allocation apportionment and absorption. ...

Capitalization and Depreciation of Property, Plant, and Equipment

... should notify ITS of their computer purchases to ensure that departmentally purchased equipment is added to the Computer Replacement Program for inclusion in the four year replacement cycle. If ITS does not receive departmental computer purchasing information, stand alone computer purchases will no ...

... should notify ITS of their computer purchases to ensure that departmentally purchased equipment is added to the Computer Replacement Program for inclusion in the four year replacement cycle. If ITS does not receive departmental computer purchasing information, stand alone computer purchases will no ...

learning objectives

... Top management caught the fraud when they realized that recorded inventory had outgrown the freezer where it was stored. ...

... Top management caught the fraud when they realized that recorded inventory had outgrown the freezer where it was stored. ...

Idle Capacity Costs: It Isn`t Just the Expense

... consistently operates at 75% CU. If each of these firms had a down year and operated at 5% less, Ewer, Keller, and Olson would suggest that the companies each record a period expense of the 5% of fixed costs that they did not use that year. While this would be a step in the right direction, we belie ...

... consistently operates at 75% CU. If each of these firms had a down year and operated at 5% less, Ewer, Keller, and Olson would suggest that the companies each record a period expense of the 5% of fixed costs that they did not use that year. While this would be a step in the right direction, we belie ...

Unit 7: Management Accounting

... in groups and carry out the necessary research to calculate the actual costs of materials for a product of their own choice. This research will include use of the internet. Learners will also work in groups to establish a reasonable price for the product based on direct costs, estimated overheads an ...

... in groups and carry out the necessary research to calculate the actual costs of materials for a product of their own choice. This research will include use of the internet. Learners will also work in groups to establish a reasonable price for the product based on direct costs, estimated overheads an ...

Example - McGraw Hill Higher Education

... Opportunity Cost The potential benefit that is given up when one alternative is selected over another. Example: If you were not attending college, you could be earning $15,000 per year. Your opportunity cost of attending college for one year is $15,000. ...

... Opportunity Cost The potential benefit that is given up when one alternative is selected over another. Example: If you were not attending college, you could be earning $15,000 per year. Your opportunity cost of attending college for one year is $15,000. ...

Break-even point

... Since the fixed costs will be incurred in any case, they are not relevant to this decision. All we need to do is to see whether the price offered will yield a contribution. It if will, then they should accept the contract as they will be better off. We know that variable costs per basket total $24 ( ...

... Since the fixed costs will be incurred in any case, they are not relevant to this decision. All we need to do is to see whether the price offered will yield a contribution. It if will, then they should accept the contract as they will be better off. We know that variable costs per basket total $24 ( ...

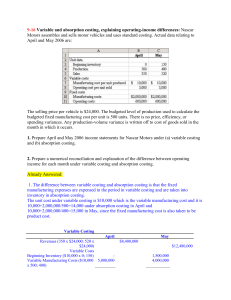

9-16 Variable and absorption costing, explaining

... 1. Prepare income statements for Nascar Motors in April and May of 2006 under throughput costing. 2. Contrast the results in requirement 1 with those in requirement 1 of Exercise 9-16. 3. Give one motivation for Nascar Motors to adopt throughput costing. ...

... 1. Prepare income statements for Nascar Motors in April and May of 2006 under throughput costing. 2. Contrast the results in requirement 1 with those in requirement 1 of Exercise 9-16. 3. Give one motivation for Nascar Motors to adopt throughput costing. ...

Document

... Sales volume variance is the difference in profit caused by the difference in budgeted and actual sales volume ...

... Sales volume variance is the difference in profit caused by the difference in budgeted and actual sales volume ...

Accounting Learning Objectives: Learning Objectives:

... labour) often not relevant – direct correlation between activity and overhead no longer exists – Total overhead costs increasing (e.g. depreciation on expensive equipment, power) – complex manufacturing processes may require multiple allocation bases ...

... labour) often not relevant – direct correlation between activity and overhead no longer exists – Total overhead costs increasing (e.g. depreciation on expensive equipment, power) – complex manufacturing processes may require multiple allocation bases ...

Breakeven Analysis - The American University in Cairo

... fluctuations in business activity, they are “variable.” Otherwise, they are “fixed.” A widely used cost model is: Total Costs = Fixed Costs + Variable Costs • Price is the amount of money, goods or services that must be given up to acquire ownership or use of a product. • Recurring/Nonrecurring Cost ...

... fluctuations in business activity, they are “variable.” Otherwise, they are “fixed.” A widely used cost model is: Total Costs = Fixed Costs + Variable Costs • Price is the amount of money, goods or services that must be given up to acquire ownership or use of a product. • Recurring/Nonrecurring Cost ...

chapter 8 revision notes

... The indirect costs of service departments may be allocated both to other service departments and to production departments. Allocation of overheads is the charging to a cost centre those overheads that result solely from the existence of that cost centre. Cost assignment defines the process of traci ...

... The indirect costs of service departments may be allocated both to other service departments and to production departments. Allocation of overheads is the charging to a cost centre those overheads that result solely from the existence of that cost centre. Cost assignment defines the process of traci ...

Product Cost Concept - MDC Faculty Web Pages

... Example 9: Assume that a business produces kerosene in batches of 4,000 Gallons. Standard quantities of 4,000 gallons of direct materials are processed which cost $0.60 per gallon. Kerosene can be sold without further processing for $0.80 per gallon. It can be processed further to yield gasoline, wh ...

... Example 9: Assume that a business produces kerosene in batches of 4,000 Gallons. Standard quantities of 4,000 gallons of direct materials are processed which cost $0.60 per gallon. Kerosene can be sold without further processing for $0.80 per gallon. It can be processed further to yield gasoline, wh ...