CPA PassMaster Questions–Auditing 4 Export Date: 10/30/08

... the audit client and thus may be unaware of all the financial relationships the bank has with the client. Choice "a" is incorrect. Standard bank confirmations contain a signature from an authorized client employee and are a very commonly used audit procedure. It is unlikely that a bank would refuse ...

... the audit client and thus may be unaware of all the financial relationships the bank has with the client. Choice "a" is incorrect. Standard bank confirmations contain a signature from an authorized client employee and are a very commonly used audit procedure. It is unlikely that a bank would refuse ...

Detecting asset misappropriation: a framework for

... Hogan et al., 2008; Srivastava et al., 2009; Shelton et al., 2001) argued that the standard provides little guidance to external auditors on fraud risk response with respect to asset misappropriation and financial reporting fraud. They also argued that ISA No. 240 did not assign weights for red flag ...

... Hogan et al., 2008; Srivastava et al., 2009; Shelton et al., 2001) argued that the standard provides little guidance to external auditors on fraud risk response with respect to asset misappropriation and financial reporting fraud. They also argued that ISA No. 240 did not assign weights for red flag ...

Revised Guidance Statement GS 009: Auditing SMSFs

... Auditors of APRA regulated superannuation entities, particularly auditors of small APRA funds, may find this Guidance Statement useful in planning, conducting and reporting their audits, but it does not relate specifically to APRA funds. See Division 1, Section 6 of the SISA. Regulated funds, under ...

... Auditors of APRA regulated superannuation entities, particularly auditors of small APRA funds, may find this Guidance Statement useful in planning, conducting and reporting their audits, but it does not relate specifically to APRA funds. See Division 1, Section 6 of the SISA. Regulated funds, under ...

Does the Big-4 Effect Exist when Reputation and

... Khurana and Raman 2004). As such, litigation and reputational concerns may be important drivers of higher audit quality for Big-4 firms compared to non-Big-4 firms. Because private clients are generally considered to be of lower reputation risk to audit firms than public clients (Palmrose 1986; Lys ...

... Khurana and Raman 2004). As such, litigation and reputational concerns may be important drivers of higher audit quality for Big-4 firms compared to non-Big-4 firms. Because private clients are generally considered to be of lower reputation risk to audit firms than public clients (Palmrose 1986; Lys ...

Defence Audit Guidelines_Final 25 March 2010

... Pakistan for use in Field Audit Offices (FAOs) for conducting Certification and Compliance with Authority audits. The Manual is based on the INTOSAI Auditing Standards and the international best practices. It covers the entire Audit Cycle and provides guidance with regard to the methods and approach ...

... Pakistan for use in Field Audit Offices (FAOs) for conducting Certification and Compliance with Authority audits. The Manual is based on the INTOSAI Auditing Standards and the international best practices. It covers the entire Audit Cycle and provides guidance with regard to the methods and approach ...

Substantive Tests of Transactions and Balances

... effective means of auditing the financial report of a small business. It is especially efficient if the auditor designs effective analytical tests for those specific audit objectives, such as statement of financial performance, account classification and those related to the completeness assertion, ...

... effective means of auditing the financial report of a small business. It is especially efficient if the auditor designs effective analytical tests for those specific audit objectives, such as statement of financial performance, account classification and those related to the completeness assertion, ...

Empirical evidence on liability caps and earnings management in

... This paper examines the effect of limiting statutory auditors’ civil liability on financial reporting quality. Auditor liability as a part of audit regulation is of particular current interest, as the European Commission has in 2008 issued a recommendation concerning the limitation of the civil liab ...

... This paper examines the effect of limiting statutory auditors’ civil liability on financial reporting quality. Auditor liability as a part of audit regulation is of particular current interest, as the European Commission has in 2008 issued a recommendation concerning the limitation of the civil liab ...

Yes, there is a big Difference between Audit on Profit Organizations

... In financial accounting, an audit is an independent assessment of the fairness by which a company's financial statements are presented by its management. It is performed by competent, independent and objective person(s) known as auditors, who then issue an auditor's report based on the results of th ...

... In financial accounting, an audit is an independent assessment of the fairness by which a company's financial statements are presented by its management. It is performed by competent, independent and objective person(s) known as auditors, who then issue an auditor's report based on the results of th ...

The Effect of Audit Firm Specialization on Earnings Management

... (2008) expected that the industry's attractiveness for specialization will be directly related to the amount of industry-specific knowledge requirements needed to complete the audit, and that these requirements are likely to vary widely across industries. Developing an industry specialization is cos ...

... (2008) expected that the industry's attractiveness for specialization will be directly related to the amount of industry-specific knowledge requirements needed to complete the audit, and that these requirements are likely to vary widely across industries. Developing an industry specialization is cos ...

Notification 297/2015 dated 28th December, 2015 - Regarding the Internal Audit Manual (672 KB)

... Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization’s operations. It helps the organization to accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk man ...

... Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization’s operations. It helps the organization to accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk man ...

ISA 520 Analytical procedures

... analytical procedures in response to assessed risks. When such controls are effective, the auditor generally has greater confidence in the reliability of the information and, therefore, in the results of analytical procedures. The operating effectiveness of controls over non-financial information ma ...

... analytical procedures in response to assessed risks. When such controls are effective, the auditor generally has greater confidence in the reliability of the information and, therefore, in the results of analytical procedures. The operating effectiveness of controls over non-financial information ma ...

6. Compliance audit of a real estate agent`s trust

... b) the name and number of each trust account audited; c) the name of the financial institution, the office or branch of the institution where each trust account was kept and the identifying number of the office or branch; d) the licensee’s name and: i. if the licensee is a corporation—the name o ...

... b) the name and number of each trust account audited; c) the name of the financial institution, the office or branch of the institution where each trust account was kept and the identifying number of the office or branch; d) the licensee’s name and: i. if the licensee is a corporation—the name o ...

MANDATORY EMPHASIS PARAGRAPHS, CLARIFYING

... would require their use in all public company audit reports to highlight critical audit matters (e.g., significant management judgments and estimates, areas with significant measurement uncertainty, etc.). The PCAOB’s proposal, therefore, reflects the notion that disclosure of the most significant ...

... would require their use in all public company audit reports to highlight critical audit matters (e.g., significant management judgments and estimates, areas with significant measurement uncertainty, etc.). The PCAOB’s proposal, therefore, reflects the notion that disclosure of the most significant ...

Comprehensive Case A.1 – Enron

... At Andersen, the compensation of partners depended on their ability to cross-sell other services to its audit clients. More than half of the fees for Enron were charged for non-audit services. By 2001, Duncan was earning more than $1 million a year. The size of the fees would likely have made it har ...

... At Andersen, the compensation of partners depended on their ability to cross-sell other services to its audit clients. More than half of the fees for Enron were charged for non-audit services. By 2001, Duncan was earning more than $1 million a year. The size of the fees would likely have made it har ...

Competency area - Chartered Institute of Internal Auditors

... with senior management and confirming the level of assurance that particular audit work attracts (recognising, for example, that a light touch audit with little testing may provide a lower level of assurance than an audit that encompasses both compliance and substantive testing), and is able to prov ...

... with senior management and confirming the level of assurance that particular audit work attracts (recognising, for example, that a light touch audit with little testing may provide a lower level of assurance than an audit that encompasses both compliance and substantive testing), and is able to prov ...

Leading Practice Examples of Audit Committee Reporting

... Internal Audit should also be prepared to attend the Executive Session, where outside Board members can question internal and external audit without the presence of Senior Management. ...

... Internal Audit should also be prepared to attend the Executive Session, where outside Board members can question internal and external audit without the presence of Senior Management. ...

Auditor Liability and Professional Skepticism: A Look at Lehman

... independent sales and later re-acquisitions. U.S. accounting standards have long recognized the need to report the substance, not simply the form, of such two-part coordinated transactions. It is thought that most, perhaps almost all, parties engaging in repos – a market of almost $3 trillion before ...

... independent sales and later re-acquisitions. U.S. accounting standards have long recognized the need to report the substance, not simply the form, of such two-part coordinated transactions. It is thought that most, perhaps almost all, parties engaging in repos – a market of almost $3 trillion before ...

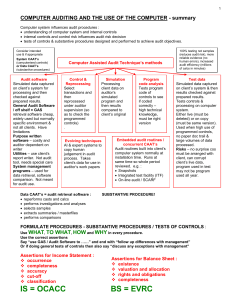

Assignment 1 is compulsory and due

... multi-level passwords (2 or more) for senior staff to authorise transfers bank must identify the terminal as authorised when EFT’s are processed (dial back etc) terminal should switch off after 3 unsuccessful attempts to do EFT should use 1-time passwords (e.g. if exceeds certain limit) se ...

... multi-level passwords (2 or more) for senior staff to authorise transfers bank must identify the terminal as authorised when EFT’s are processed (dial back etc) terminal should switch off after 3 unsuccessful attempts to do EFT should use 1-time passwords (e.g. if exceeds certain limit) se ...

Sample September / December 2015 answers

... the point when the payment is received as the conditions for recognition of revenue are unlikely to have been met at this point in time. There is additional audit risk created if a customer were to cancel a contract part way through its completion, the bespoke work in progress may be worthless and w ...

... the point when the payment is received as the conditions for recognition of revenue are unlikely to have been met at this point in time. There is additional audit risk created if a customer were to cancel a contract part way through its completion, the bespoke work in progress may be worthless and w ...

working program - Almaty Management University

... The working program has been developed on the basis of the Sample Program of the course (for mandatory component): “Basis audit” for students of the specialty: 5B050900 - “Finance” The working curriculum was reviewed at the meeting of the Department of “Valuation, accounting and audit” Protocol №1 f ...

... The working program has been developed on the basis of the Sample Program of the course (for mandatory component): “Basis audit” for students of the specialty: 5B050900 - “Finance” The working curriculum was reviewed at the meeting of the Department of “Valuation, accounting and audit” Protocol №1 f ...

internal-auditing-instructional-material

... d. A statement of positive assurance on those items of compliance tested and negative assurance on those items not tested. This should include significant instances of noncompliance and instances of or indicating of fraud, abuse or illegal acts found during or in connection with the audit. However, ...

... d. A statement of positive assurance on those items of compliance tested and negative assurance on those items not tested. This should include significant instances of noncompliance and instances of or indicating of fraud, abuse or illegal acts found during or in connection with the audit. However, ...

Answers

... include controls testing over cash receipts and cash counts. As a retailer the stores will have a significant amount of cash at each premise and will have tight controls over the cash receipts process. These controls should be tested at each location as well as performance of a cash count to reduce ...

... include controls testing over cash receipts and cash counts. As a retailer the stores will have a significant amount of cash at each premise and will have tight controls over the cash receipts process. These controls should be tested at each location as well as performance of a cash count to reduce ...

The Auditor - Whose Agent Is He Anyway

... auditors will find themselves being ‘friends’ with management (familiarity threat), and perhaps entering into providing management advice (advocacy threat). In rare occasions a dominance threat may arise where management know the auditor fears losing their contract, and can play this to their advant ...

... auditors will find themselves being ‘friends’ with management (familiarity threat), and perhaps entering into providing management advice (advocacy threat). In rare occasions a dominance threat may arise where management know the auditor fears losing their contract, and can play this to their advant ...

Defense Contract Audit Agency

The Defense Contract Audit Agency (DCAA), is an agency of the United States Department of Defense under the direction of the Under Secretary of Defense (Comptroller). It was established in 1965 to perform all contract audits for the Department of Defense. Previously, the various branches of military service were responsible for their own contract audits.The DCAA's duties include financial and accounting advisory services for the Department of Defense in connection with negotiation, administration and settlement of contracts and subcontracts. To a lesser extent, it also performs audits for other federal agencies.