What Causes Herding: Information Cascade or Search Cost ?

... superior returns. As everyone follows his signal, rational herding cannot occur. Note that not trading is never optimal (unless one introduces transaction costs) because subjects always have an informational advantage over the market maker. Alternatively, VW proposed a model with two assets traded i ...

... superior returns. As everyone follows his signal, rational herding cannot occur. Note that not trading is never optimal (unless one introduces transaction costs) because subjects always have an informational advantage over the market maker. Alternatively, VW proposed a model with two assets traded i ...

Liquidity Risk and Asset Pricing

... using short-term price reversals as our measure of the return to supplying liquidity, ...

... using short-term price reversals as our measure of the return to supplying liquidity, ...

Mutual Fund Flows and Fluctuations in Credit and Business Cycles

... We start with investigating whether HYNEIO can predict variables that were found to be indicators for the credit cycle. We focus on Greenwood and Hanson’s (2013) high-yield-share (HYS), which measures the quality of corporate bond issuers, and the degrees of reaching for yield (Baker and Ivashina, 2 ...

... We start with investigating whether HYNEIO can predict variables that were found to be indicators for the credit cycle. We focus on Greenwood and Hanson’s (2013) high-yield-share (HYS), which measures the quality of corporate bond issuers, and the degrees of reaching for yield (Baker and Ivashina, 2 ...

Futurization of Swaps

... neither the CFTC nor the SEC have addressed. First, margins on futures contracts are calculated differently from and are lower than those for swaps. This is a strong reason by itself for the migration from swaps to futures. But as this migration continues and volumes of transactions cleared on futur ...

... neither the CFTC nor the SEC have addressed. First, margins on futures contracts are calculated differently from and are lower than those for swaps. This is a strong reason by itself for the migration from swaps to futures. But as this migration continues and volumes of transactions cleared on futur ...

Gains from Stock Exchange Integration: The

... Users face two types of trading costs: (a) explicit costs, such as, for example, exchange fees, commissions, and the costs of clearing and settlement; and (b) implicit costs, which include the bid-ask spread and the price impact of orders, to the extent that large orders cause an adverse change in s ...

... Users face two types of trading costs: (a) explicit costs, such as, for example, exchange fees, commissions, and the costs of clearing and settlement; and (b) implicit costs, which include the bid-ask spread and the price impact of orders, to the extent that large orders cause an adverse change in s ...

Price Volatility, Trading Activity and Market Depth

... contracts traded on the Taiwan Futures Exchange (TAIFEX) and Singapore Exchange Derivatives Trading Division (SGX-DT). Two different methodologies, the OLS-based and GARCH-based models, are used to test the robustness of the result and to obtain a sensitivity check. The major findings of this invest ...

... contracts traded on the Taiwan Futures Exchange (TAIFEX) and Singapore Exchange Derivatives Trading Division (SGX-DT). Two different methodologies, the OLS-based and GARCH-based models, are used to test the robustness of the result and to obtain a sensitivity check. The major findings of this invest ...

Automated Trading Desk and Price Prediction in High

... This article is a contribution to what has become known as ‘social studies of finance’, the application to financial markets not of economics but of wider social-science disciplines such as anthropology, politics, geography, sociology and science and technology studies (STS). STS-inflected work has ...

... This article is a contribution to what has become known as ‘social studies of finance’, the application to financial markets not of economics but of wider social-science disciplines such as anthropology, politics, geography, sociology and science and technology studies (STS). STS-inflected work has ...

The Causal Effects of Short-Selling Bans

... restrictions. The bubble is accompanied by increased volume and volatility. If short-sale restrictions prevent these bubbles, short-sale bans should reduce volatility and volume. Allen, Morris and Postlewaite (1993) show that overpricing can result from short-sale bans as a result of private inform ...

... restrictions. The bubble is accompanied by increased volume and volatility. If short-sale restrictions prevent these bubbles, short-sale bans should reduce volatility and volume. Allen, Morris and Postlewaite (1993) show that overpricing can result from short-sale bans as a result of private inform ...

Limited partnership

... declared goals. Companies take various forms such as: Voluntary associations which may include nonprofit organization A group of soldiers Business entities with an aim of gaining a profit Financial entities and banks. A company or association of persons can be created at law as legal person ...

... declared goals. Companies take various forms such as: Voluntary associations which may include nonprofit organization A group of soldiers Business entities with an aim of gaining a profit Financial entities and banks. A company or association of persons can be created at law as legal person ...

Longshots, Overconfidence and Efficiency on the Iowa Electronic Market

... underdogs in football betting markets can have positive profits. This could be interpreted as a partial reversal of the longshot bias in these differently structured markets (point-spreads, instead of odds, adjust to guarantee the bookie’s take). Because financial markets differ in structure as well ...

... underdogs in football betting markets can have positive profits. This could be interpreted as a partial reversal of the longshot bias in these differently structured markets (point-spreads, instead of odds, adjust to guarantee the bookie’s take). Because financial markets differ in structure as well ...

Trading and Electronic Markets

... that stood when the trades were first ordered. The VWAP (volume-weighted average price) method, which managers commonly use, has many problems. Keeping track of the opportunity costs associated with trades ordered but not executed is very important because this information can help traders know when ...

... that stood when the trades were first ordered. The VWAP (volume-weighted average price) method, which managers commonly use, has many problems. Keeping track of the opportunity costs associated with trades ordered but not executed is very important because this information can help traders know when ...

Bubbles

... if investors hold the asset because they believe that they can sell it at a higher price than some other investor even though the asset’s price exceeds its fundamental value. Famous historical examples are the Dutch tulip mania (1634–7), the Mississippi Bubble (1719– 20), the South Sea Bubble (1720) ...

... if investors hold the asset because they believe that they can sell it at a higher price than some other investor even though the asset’s price exceeds its fundamental value. Famous historical examples are the Dutch tulip mania (1634–7), the Mississippi Bubble (1719– 20), the South Sea Bubble (1720) ...

Smoking or trading ? On cigarette money in post WW2

... Everyone familiar with search models can easily understand the difference between direct barter goods and all the other goods. A good is used only in direct barter if nobody has interest to used it as an intermediary of exchange. Hence, partial intermediary of exchange and commodity money shared the ...

... Everyone familiar with search models can easily understand the difference between direct barter goods and all the other goods. A good is used only in direct barter if nobody has interest to used it as an intermediary of exchange. Hence, partial intermediary of exchange and commodity money shared the ...

Sample pages 1 PDF

... corresponding net returns. Since returns are smaller in magnitude over shorter periods, we can expect returns and log returns to be similar for daily returns, less similar for yearly returns, and not necessarily similar for longer periods ...

... corresponding net returns. Since returns are smaller in magnitude over shorter periods, we can expect returns and log returns to be similar for daily returns, less similar for yearly returns, and not necessarily similar for longer periods ...

Corporate Bond Trading on a Limit Order Book Exchange by

... This paper investigates the case of the Tel Aviv Stock Exchange (hereafter TASE), where c-bonds (and government bonds) have been traded for many years by the same open limit order book system as stocks and with no competing exchanges, dark pools, etc. The Israeli c-bond market is quite small (~$76 b ...

... This paper investigates the case of the Tel Aviv Stock Exchange (hereafter TASE), where c-bonds (and government bonds) have been traded for many years by the same open limit order book system as stocks and with no competing exchanges, dark pools, etc. The Israeli c-bond market is quite small (~$76 b ...

The Market Abuse Regulation

... In practice, where there is a query as to whether an AIM company should make a disclosure, we will continue to liaise with the AIM company’s nominated adviser regarding its AIM Rules obligations and will provide the FCA with information about these discussions, where relevant to MAR. It is open to t ...

... In practice, where there is a query as to whether an AIM company should make a disclosure, we will continue to liaise with the AIM company’s nominated adviser regarding its AIM Rules obligations and will provide the FCA with information about these discussions, where relevant to MAR. It is open to t ...

Longshots, Overconfidence and Efficiency on the Iowa Electronic Market

... if traders over-react to small changes in the perceived probabilities of crashes, then the expected values of stocks will react more than they should to such changes in probabilities without correspondingly large changes in actual future outcomes (e.g., dividends). This may help explain the excess v ...

... if traders over-react to small changes in the perceived probabilities of crashes, then the expected values of stocks will react more than they should to such changes in probabilities without correspondingly large changes in actual future outcomes (e.g., dividends). This may help explain the excess v ...

The Term Structure of the Risk-Return Tradeoff

... simplicity, we show unconditional average portfolio allocations rather than the full range of allocations that would be optimal under different market conditions. The concept of a term structure of the risk-return tradeoff is conceptually appealing but, strictly speaking, is only valid for buy-and- ...

... simplicity, we show unconditional average portfolio allocations rather than the full range of allocations that would be optimal under different market conditions. The concept of a term structure of the risk-return tradeoff is conceptually appealing but, strictly speaking, is only valid for buy-and- ...

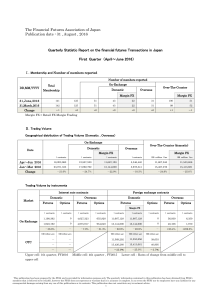

The Financial Futures Association of Japan Publication date : 31

... This publication has been prepared by the FFAJ and is provided for information purpose only. The quarterly information contained in this publication has been obtained from FFAJ's members that is believed to be reliable, however the FFAJ does not represent or warrant that it is accurate or complete. ...

... This publication has been prepared by the FFAJ and is provided for information purpose only. The quarterly information contained in this publication has been obtained from FFAJ's members that is believed to be reliable, however the FFAJ does not represent or warrant that it is accurate or complete. ...

NBER WORKING PAPER SERIES Kristin J. Forbes Working Paper 13908

... The empirical results suggest that a primary factor driving both equity and bond flows into the United States is a country’s level of financial development. Countries with less developed financial markets tend to hold a greater share of their portfolios in the United States, and the strength of thi ...

... The empirical results suggest that a primary factor driving both equity and bond flows into the United States is a country’s level of financial development. Countries with less developed financial markets tend to hold a greater share of their portfolios in the United States, and the strength of thi ...

the structure of forward and futures markets

... Which of the following correctly orders the process of daily settlement? a. clearinghouse officials establish a settlement price; each account is marked to market; accounts of those holding long/short positions are credited/debited appropriately; differences between today’s settlement price and the ...

... Which of the following correctly orders the process of daily settlement? a. clearinghouse officials establish a settlement price; each account is marked to market; accounts of those holding long/short positions are credited/debited appropriately; differences between today’s settlement price and the ...

ABB Successfully Completes Tender Offer for Baldor Common Stock

... 47,455,713 outstanding shares, were tendered and not withdrawn pursuant to the tender offer, including 2,907,369 shares that were tendered pursuant to notices of guaranteed delivery. According to the terms of the tender offer, shares that were validly tendered and not validly withdrawn have been acc ...

... 47,455,713 outstanding shares, were tendered and not withdrawn pursuant to the tender offer, including 2,907,369 shares that were tendered pursuant to notices of guaranteed delivery. According to the terms of the tender offer, shares that were validly tendered and not validly withdrawn have been acc ...

Form 425, 5/26/11

... June 8th, we’re — our hope is that we’re dependent on the speed with which it gets heard, the appeal, and exactly the process the appeal occurs. Because it’s not, to my understanding, which is always a risk — is not rocks clear solid about which way it’ll go. But likely from June 8th, it’s probably ...

... June 8th, we’re — our hope is that we’re dependent on the speed with which it gets heard, the appeal, and exactly the process the appeal occurs. Because it’s not, to my understanding, which is always a risk — is not rocks clear solid about which way it’ll go. But likely from June 8th, it’s probably ...

Volume and Liquidity After Cross

... shares on the foreign market at the cross-listing date or soon after it. One would expect such stocks to feature a larger foreign trading volume than that of others. Empirically, therefore, the distribution of trading volume should be related to the fraction of foreign ownership around the cross-lis ...

... shares on the foreign market at the cross-listing date or soon after it. One would expect such stocks to feature a larger foreign trading volume than that of others. Empirically, therefore, the distribution of trading volume should be related to the fraction of foreign ownership around the cross-lis ...

Stock exchange

A stock exchange is an exchange or stock market where stock brokers and traders can buy and/or sell stocks (also called shares), bonds, and other securities. Stock exchanges may also provide facilities for issue and redemption of securities and other financial instruments, and capital events including the payment of income and dividends. Securities traded on a stock exchange include stock issued by listed companies, unit trusts, derivatives, pooled investment products and bonds. Stock exchanges often function as ""continuous auction"" markets, with buyers and sellers consummating transactions at a central location, such as the floor of the exchange.To be able to trade a security on a certain stock exchange, it must be listed there. Usually, there is a central location at least for record keeping, but trade is increasingly less linked to such a physical place, as modern markets use electronic networks, which gives them advantages of increased speed and reduced cost of transactions. Trade on an exchange is restricted to brokers who are members of the exchange. In recent years, various other trading venues, such as electronic communication networks, alternative trading systems and ""dark pools"" have taken much of the trading activity away from traditional stock exchanges.The initial public offering of stocks and bonds to investors is by definition done in the primary market and subsequent trading is done in the secondary market. A stock exchange is often the most important component of a stock market. Supply and demand in stock markets are driven by various factors that, as in all free markets, affect the price of stocks (see stock valuation).There is usually no obligation for stock to be issued via the stock exchange itself, nor must stock be subsequently traded on the exchange. Such trading may be off exchange or over-the-counter. This is the usual way that derivatives and bonds are traded. Increasingly, stock exchanges are part of a global securities market.