The Relationship between Mortgage Markets and House Prices

... a subsequent significant resurgence thereafter. After the US subprime crisis in August 2007, house prices have then progressively declined and, in particular, during 2008. Mortgage credit, however, increased constantly (in per capita terms) throughout the period analysed. However, the intensity of ...

... a subsequent significant resurgence thereafter. After the US subprime crisis in August 2007, house prices have then progressively declined and, in particular, during 2008. Mortgage credit, however, increased constantly (in per capita terms) throughout the period analysed. However, the intensity of ...

Mortgage market in the Netherlands

... economy could stabilise the housing market. Recent mortgage borrowers in particular are facing increasing risks. Negative housing equity (higher mortgage than current value of house) is already emerging and this process will continue as long as house prices decline further. Still, the structure of t ...

... economy could stabilise the housing market. Recent mortgage borrowers in particular are facing increasing risks. Negative housing equity (higher mortgage than current value of house) is already emerging and this process will continue as long as house prices decline further. Still, the structure of t ...

REO Resources - Florida Realtors

... clear the inventory from their books. Due to this pricing, many properties receive multiple offers before it is even placed in the MLS, so it is very possible that the offer was presented, but not accepted. It is recommended you counsel your buyer about your opinion of the actual value of the proper ...

... clear the inventory from their books. Due to this pricing, many properties receive multiple offers before it is even placed in the MLS, so it is very possible that the offer was presented, but not accepted. It is recommended you counsel your buyer about your opinion of the actual value of the proper ...

PRODUCT GUIDELINES FHA STANDARD and HIGH BALANCE

... AUS Approve - Chapter 13 must document the following: 1) 1 year of the pay-out period under the bankruptcy has elapsed. 2) All borrower's payments have been made on time. 3) Borrower has received written permission from court to enter into mortgage transaction. If the Chapter 13 bankruptcy has not b ...

... AUS Approve - Chapter 13 must document the following: 1) 1 year of the pay-out period under the bankruptcy has elapsed. 2) All borrower's payments have been made on time. 3) Borrower has received written permission from court to enter into mortgage transaction. If the Chapter 13 bankruptcy has not b ...

Rebalancing the housing and mortgage markets – critical issues

... The housing and mortgage markets in the UK have undergone radical changes in recent years, in the wake of the international crisis in financial markets. New national and international regulatory frameworks for the mortgage markets are now in place, but considerable uncertainties remain about the fut ...

... The housing and mortgage markets in the UK have undergone radical changes in recent years, in the wake of the international crisis in financial markets. New national and international regulatory frameworks for the mortgage markets are now in place, but considerable uncertainties remain about the fut ...

Credit History and the Performance of Prime and Nonprime Mortgages

... Using a competing risk framework that allows for unobserved individual borrower heterogeneity this paper examines the performance (default and prepay probabilities and termination rates) of prime and nonprime loans that were originated from February 1995 through February 1998. The simple average fro ...

... Using a competing risk framework that allows for unobserved individual borrower heterogeneity this paper examines the performance (default and prepay probabilities and termination rates) of prime and nonprime loans that were originated from February 1995 through February 1998. The simple average fro ...

Patrick Bayer, Duke University and NBER

... purchased their homes between 2004 and 2007 – i.e., those drawn into the market at the peak of the credit expansion. Taken together, our results provide strong evidence that minority households drawn into homeownership late in the recent housing market boom were especially vulnerable in the subsequ ...

... purchased their homes between 2004 and 2007 – i.e., those drawn into the market at the peak of the credit expansion. Taken together, our results provide strong evidence that minority households drawn into homeownership late in the recent housing market boom were especially vulnerable in the subsequ ...

1 Barriers to Market Discipline: A Comparative Study of Mortgage

... 1999 the U.S. federal banking regulators recognized that “higher fees and interest rates [charged for subprime loans] combined with compensation incentives can foster predatory pricing or discriminatory 'steering' of borrowers to subprime products for reasons other than the borrower’s underlying cre ...

... 1999 the U.S. federal banking regulators recognized that “higher fees and interest rates [charged for subprime loans] combined with compensation incentives can foster predatory pricing or discriminatory 'steering' of borrowers to subprime products for reasons other than the borrower’s underlying cre ...

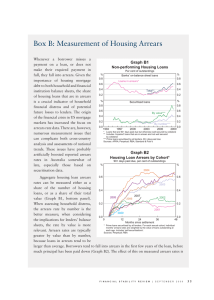

Box B: Measurement of Housing Arrears Graph B1

... amplified because average new loan sizes tend to increase over time, relative to the average size of loans already outstanding, as nominal housing prices and incomes rise. The criteria for defining a given loan as being in arrears can differ across countries and lenders. In Australia, housing loans ...

... amplified because average new loan sizes tend to increase over time, relative to the average size of loans already outstanding, as nominal housing prices and incomes rise. The criteria for defining a given loan as being in arrears can differ across countries and lenders. In Australia, housing loans ...

How the Affluent Manage Home Equity to Safely and Conservatively

... he answer? Most of what we believe about mortgages and home equity, which we learned from our parents and grandparents, is wrong. They taught us to make a big down payment, get a fixed rate mortgage, and make extra principle payments in order to pay off your loan as early as you can. Mortgages, they ...

... he answer? Most of what we believe about mortgages and home equity, which we learned from our parents and grandparents, is wrong. They taught us to make a big down payment, get a fixed rate mortgage, and make extra principle payments in order to pay off your loan as early as you can. Mortgages, they ...

Riding the Stagecoach to Hell: A Qualitative Analysis of

... than equally qualified whites to receive high-cost, high-risk loans during the U.S. housing boom, evidence taken to suggest widespread discrimination in the mortgage lending industry. The evidence, however, was indirect, being inferred from racial differentials that persisted after controlling for o ...

... than equally qualified whites to receive high-cost, high-risk loans during the U.S. housing boom, evidence taken to suggest widespread discrimination in the mortgage lending industry. The evidence, however, was indirect, being inferred from racial differentials that persisted after controlling for o ...

PDF

... G10 countries. Even though the Basel Committee cannot enforce any of the accords, most member countries still follow their recommendations. The goal of the Basel Committee is to help banks measure and control their risks more accurately and efficiently, which can help increase the profitability, pri ...

... G10 countries. Even though the Basel Committee cannot enforce any of the accords, most member countries still follow their recommendations. The goal of the Basel Committee is to help banks measure and control their risks more accurately and efficiently, which can help increase the profitability, pri ...

CSS Slideshow for 1997-98 Counselor Workshops

... Stafford, PLUS, Perkins, HEAL, or other federal student loans ...

... Stafford, PLUS, Perkins, HEAL, or other federal student loans ...

The Top Seven Financial Pitfalls Every - No

... Please note that most loans are no longer assumable. In 1985 a law was passed that restricts the ability to assume loans and most if not all major lenders no longer allow their loans to be fully assumed by a new buyer or mortgagor. “Subject to” transactions have been attractive to investors because ...

... Please note that most loans are no longer assumable. In 1985 a law was passed that restricts the ability to assume loans and most if not all major lenders no longer allow their loans to be fully assumed by a new buyer or mortgagor. “Subject to” transactions have been attractive to investors because ...

CAPSTEAD MORTGAGE CORP (Form: 8-K, Received: 01

... Commenting on current operating and market conditions, Phillip A. Reinsch, President and Chief Executive Officer, said, “Earnings for the fourth quarter were hampered by slower than anticipated declines in mortgage prepayment levels. As a result, portfolio yields did not improve as much as expected. ...

... Commenting on current operating and market conditions, Phillip A. Reinsch, President and Chief Executive Officer, said, “Earnings for the fourth quarter were hampered by slower than anticipated declines in mortgage prepayment levels. As a result, portfolio yields did not improve as much as expected. ...

Fact Sheet: Xerox to Acquire Advectis, Inc.

... Q: Why is Xerox acquiring Advectis? A: Consistent with our growth strategy in services, we have been exploring acquisitions that strengthen Xerox’s document management capabilities in targeted industries. We continue to identify technology and services that help simplify document-intensive processes ...

... Q: Why is Xerox acquiring Advectis? A: Consistent with our growth strategy in services, we have been exploring acquisitions that strengthen Xerox’s document management capabilities in targeted industries. We continue to identify technology and services that help simplify document-intensive processes ...

assisting the start-up and growing business

... application, he or she may then be able to anticipate and satisfy the lender’s requirements. Applying for a loan is typically viewed as a process involving a person in need of funds applying to an institution that has those funds but is reluctant to lend to the one in need. The borrower may commonly ...

... application, he or she may then be able to anticipate and satisfy the lender’s requirements. Applying for a loan is typically viewed as a process involving a person in need of funds applying to an institution that has those funds but is reluctant to lend to the one in need. The borrower may commonly ...

Editable Agenda - Mortgage Bankers Association

... Seasoned industry experts analyze recent regulatory changes and their impacton access to credit moving forward. Discuss the challenges lenders face withcertain borrower segments and the underserved, including first time homebuyers,those with thin credit files, those with repaired credit, credit invi ...

... Seasoned industry experts analyze recent regulatory changes and their impacton access to credit moving forward. Discuss the challenges lenders face withcertain borrower segments and the underserved, including first time homebuyers,those with thin credit files, those with repaired credit, credit invi ...

Money Adviser Pack Update – Summary of main changes

... order issued against their property are not excluded from HMS, nor do they need agreement from their charging order creditor to enter the scheme. Where payments are being made in respect of the charging order, these should be reviewed as part of the holistic money advice offered and factored into th ...

... order issued against their property are not excluded from HMS, nor do they need agreement from their charging order creditor to enter the scheme. Where payments are being made in respect of the charging order, these should be reviewed as part of the holistic money advice offered and factored into th ...

New Trends in Mortgage Fraud - National Crime Prevention Council

... Financial institutions sought to increase profits by adding features to their loans, including adjustable interest rates and prepayment penalties, which increased costs for borrowers. ...

... Financial institutions sought to increase profits by adding features to their loans, including adjustable interest rates and prepayment penalties, which increased costs for borrowers. ...

Lease

... Conventional mortgage • Offered by a lender who assumes all the risk of loss Federal Housing Administration (FHA) mortgage insurance • Offers lenders mortgage insurance on loans having a high loan-to-value ratio • Intent is to encourage loans to home buyers who have very little money available for a ...

... Conventional mortgage • Offered by a lender who assumes all the risk of loss Federal Housing Administration (FHA) mortgage insurance • Offers lenders mortgage insurance on loans having a high loan-to-value ratio • Intent is to encourage loans to home buyers who have very little money available for a ...

Mortgage Interest Rates

... The Canada Deposit Insurance Corporation (CDIC), a federal Crown corporation, insures up to $100,000 of most deposits (chequing and savings accounts, guaranteed investment certificates and other term deposits with a maturity of five years or less) made at Canadian financial institutions that are mem ...

... The Canada Deposit Insurance Corporation (CDIC), a federal Crown corporation, insures up to $100,000 of most deposits (chequing and savings accounts, guaranteed investment certificates and other term deposits with a maturity of five years or less) made at Canadian financial institutions that are mem ...

The Economy Drags Housing Upward

... Under his leadership, in 2015 Fannie Mae’s Economic and Strategic Research Group won the NABE Outlook Award presented annually for the most accurate GDP and Treasury note yield forecasts. In addition, the Group was awarded Pulsenomics best home price forecast. Named one of Bloomberg / BusinessWeek's ...

... Under his leadership, in 2015 Fannie Mae’s Economic and Strategic Research Group won the NABE Outlook Award presented annually for the most accurate GDP and Treasury note yield forecasts. In addition, the Group was awarded Pulsenomics best home price forecast. Named one of Bloomberg / BusinessWeek's ...

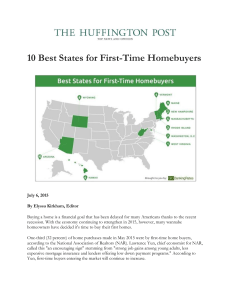

10 Best States for First-Time Homebuyers

... Vermont is yet another Northeast state that has seen strong growth among first-time home buyers, with a 48.2 percent rise from 2003 to 2013. The state also has one of the lowest foreclosure rates at 0.02 percent. The MOVE mortgage credit certificates offered through the Vermont Housing Finance Agenc ...

... Vermont is yet another Northeast state that has seen strong growth among first-time home buyers, with a 48.2 percent rise from 2003 to 2013. The state also has one of the lowest foreclosure rates at 0.02 percent. The MOVE mortgage credit certificates offered through the Vermont Housing Finance Agenc ...