credit union trends report

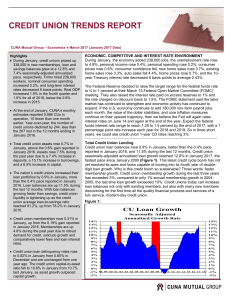

... has exceeded 3%, compared to only 1% annual membership growth in 20042005, the last time loan growth exceeded 10%. Credit unions today can increase loan balances not only with existing members, but also with many new members discovering for the first time all the quality financial products and servi ...

... has exceeded 3%, compared to only 1% annual membership growth in 20042005, the last time loan growth exceeded 10%. Credit unions today can increase loan balances not only with existing members, but also with many new members discovering for the first time all the quality financial products and servi ...

Joint Center for Housing Studies Harvard University

... During the early stages of the crisis, in 2007 and the first part of 2008, public policy was mostly concerned with impending rate resets on ARMs. As the crisis progressed, however, the spike in early payment defaults made clear that increasing numbers of homeowners could not afford their monthly mor ...

... During the early stages of the crisis, in 2007 and the first part of 2008, public policy was mostly concerned with impending rate resets on ARMs. As the crisis progressed, however, the spike in early payment defaults made clear that increasing numbers of homeowners could not afford their monthly mor ...

Can Jane Get a Mortgage Loan? Depends on When

... The literature on discrimination in US mortgage lending focuses primarily on racial discrimination and examines three different dimensions of the issue. The first approach examines differences in loan performance, while the second approach examines differences in loan pricing, and the third approach ...

... The literature on discrimination in US mortgage lending focuses primarily on racial discrimination and examines three different dimensions of the issue. The first approach examines differences in loan performance, while the second approach examines differences in loan pricing, and the third approach ...

TO DETERMINE INTEREST AND LOAN DEFAULT RATES AMONG

... however, more pronounced in privately owned banks than in the state owned. The literature review focused on term structure theory as the guiding frame and other researchers who explored the concepts of interest rates in banks, loan default in commercial banks, and the relationship between interest r ...

... however, more pronounced in privately owned banks than in the state owned. The literature review focused on term structure theory as the guiding frame and other researchers who explored the concepts of interest rates in banks, loan default in commercial banks, and the relationship between interest r ...

Compiled by CA. Aditya Kumar Maheshwari AS – 30 :: Financial

... this loan at an amortised cost of Rs. 2,50,000. Aakshaya Ltd. Has plant to hive off the receivable at a later stage and as a measure to safeguard against fall in value of its due enters into a pay-fixed, received floating interest rate swap to convert the fixed interest receipts into floating rate r ...

... this loan at an amortised cost of Rs. 2,50,000. Aakshaya Ltd. Has plant to hive off the receivable at a later stage and as a measure to safeguard against fall in value of its due enters into a pay-fixed, received floating interest rate swap to convert the fixed interest receipts into floating rate r ...

SIMPLE INTEREST VS COMPOUND INTEREST

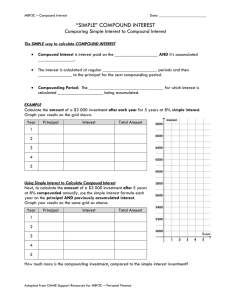

... a) Carlene wants to borrow $7 000 for five years. Compare the growth of this loan at 7% per year, simple interest, to the same loan at 7% per year, compounded annually. ...

... a) Carlene wants to borrow $7 000 for five years. Compare the growth of this loan at 7% per year, simple interest, to the same loan at 7% per year, compounded annually. ...

Existing proposals for taming procyclicality

... • Some variables, both macroeconomic and bank-specific, had statistically significant effect on the size of the loan loss provisions. • As expected, the coefficient on GDP growth was generally negative (though often not significant), indicating that provisioning is higher during economic downswings ...

... • Some variables, both macroeconomic and bank-specific, had statistically significant effect on the size of the loan loss provisions. • As expected, the coefficient on GDP growth was generally negative (though often not significant), indicating that provisioning is higher during economic downswings ...

Economic Performance, Wealth Distribution and Credit

... In the extensions, we add labor to the model. There is a threshold level of wealth such that agents with less wealth have no access to credit and become workers, while the rest become entrepreneurs, with a discrete jump in individual welfare. Thus, changes in the financial market parameters or in th ...

... In the extensions, we add labor to the model. There is a threshold level of wealth such that agents with less wealth have no access to credit and become workers, while the rest become entrepreneurs, with a discrete jump in individual welfare. Thus, changes in the financial market parameters or in th ...

The Story of CMLTI 2006-NC2

... To sell the bonds, Citi needed the rating agencies to rate them. On September 11, S&P ran its model and confirmed the ratings of the individual tranches. When the deal was priced on September 12, the interest rates on some of the bonds were slightly different than those S&P had originally modeled. ...

... To sell the bonds, Citi needed the rating agencies to rate them. On September 11, S&P ran its model and confirmed the ratings of the individual tranches. When the deal was priced on September 12, the interest rates on some of the bonds were slightly different than those S&P had originally modeled. ...

Concession Agreement of IPP - Department of Energy Business

... GOL to maintain ratification of New York Convention 1958 GOL to waive its sovereign immunity ...

... GOL to maintain ratification of New York Convention 1958 GOL to waive its sovereign immunity ...

A Call to ARMs: Adjustable Rate Mortgages in the 1980s

... lower initial interest rates than FRMs. The relaxation of restrictions on ARMs nationBecause borrowers typically qualify for mortwide in 1981 was followed by a period of experimengages based on the rafio of their initial mortgage tation with the various allowable ARM features to payment to their cur ...

... lower initial interest rates than FRMs. The relaxation of restrictions on ARMs nationBecause borrowers typically qualify for mortwide in 1981 was followed by a period of experimengages based on the rafio of their initial mortgage tation with the various allowable ARM features to payment to their cur ...

PDF Download

... selection bias should not play an overwhelmingly important role in our data set. Also other papers show that the selection bias is not severe. Using data on both firms with and without loans, Chakraborty and Hu (2006) show that the selection bias is not severe when estimating whether a loan is colla ...

... selection bias should not play an overwhelmingly important role in our data set. Also other papers show that the selection bias is not severe. Using data on both firms with and without loans, Chakraborty and Hu (2006) show that the selection bias is not severe when estimating whether a loan is colla ...

Got rejected? Real effects of not getting a loan

... Considerable attention has been devoted to the role of firm’s cash holdings. One theory postulates that firms hold cash for precautionary motives, because cash protects them against adverse funding shocks. However, little is known about the role of cash holdings in the transmission of funding shocks ...

... Considerable attention has been devoted to the role of firm’s cash holdings. One theory postulates that firms hold cash for precautionary motives, because cash protects them against adverse funding shocks. However, little is known about the role of cash holdings in the transmission of funding shocks ...

A Critical Comparison of cash- and asset-based Microcredit

... In order to demonstrate the advantages of this approach we must first address two important questions; firstly, have traditional microcredit markets been able to overcome inherent imperfections to provide efficient credit services to the poor, secondly, does access to credit lead to significant pove ...

... In order to demonstrate the advantages of this approach we must first address two important questions; firstly, have traditional microcredit markets been able to overcome inherent imperfections to provide efficient credit services to the poor, secondly, does access to credit lead to significant pove ...

Manual for municipalities: Part 1: Becoming creditworthy

... For a minority of urban areas, where there is a well-run municipality with a reasonable tax base, and an appropriate national legislative framework, the possibility exists that the municipality may take out loans to finance some of its infrastructure requirements. This manual is directed primarily a ...

... For a minority of urban areas, where there is a well-run municipality with a reasonable tax base, and an appropriate national legislative framework, the possibility exists that the municipality may take out loans to finance some of its infrastructure requirements. This manual is directed primarily a ...

Lending-Standards-Business-Loans-and-Output-CEA-JUNE

... Viessmann European Research Centre Brady Lavender, Bank of Canada ...

... Viessmann European Research Centre Brady Lavender, Bank of Canada ...

MLAR definitions - Bank of England

... NOTES FOR COMPLETION OF THE MORTGAGE LENDERS & ADMINISTRATORS RETURN (‘MLAR’) ...

... NOTES FOR COMPLETION OF THE MORTGAGE LENDERS & ADMINISTRATORS RETURN (‘MLAR’) ...

The use of intangible assets as loan collateral

... loan collateral. Over the last several years, unregulated lenders (finance companies, insurance firms, investment banks, institutional investors) with greater risk appetite have become an important source of credit. These financial intermediaries have been willing to lend to distressed borrowers by ...

... loan collateral. Over the last several years, unregulated lenders (finance companies, insurance firms, investment banks, institutional investors) with greater risk appetite have become an important source of credit. These financial intermediaries have been willing to lend to distressed borrowers by ...

5. F M F

... risk of deflation, the ECB cut the policy rate and the negative interest rate imposed on banks for their deposits by 10 basis points each and decided to launch a two-year asset-backed securities purchase program starting in the final quarter of this year. Another highlight of this quarter was the sh ...

... risk of deflation, the ECB cut the policy rate and the negative interest rate imposed on banks for their deposits by 10 basis points each and decided to launch a two-year asset-backed securities purchase program starting in the final quarter of this year. Another highlight of this quarter was the sh ...

Non-Owner-Occupancy Misrepresentation and Loan Default

... merge between (i) loan-level mortgage data collected by BlackBox Logic and (ii) borrower-level credit report information collected by Equifax. The merge is performed by Equifax using a proprietary merge algorithm utilizing more than 25 variables. Equifax is one of the three largest credit bureaus in ...

... merge between (i) loan-level mortgage data collected by BlackBox Logic and (ii) borrower-level credit report information collected by Equifax. The merge is performed by Equifax using a proprietary merge algorithm utilizing more than 25 variables. Equifax is one of the three largest credit bureaus in ...

NBER WORKING PAPER SERIES ALL BANKS GREAT, SMALL, AND GLOBAL:

... the two types of financial openness yield very different impacts on interest rates, even in this case where they have little effect on aggregate outcomes. In our general equilibrium model, heterogeneous banks compete through their choice of interest rate to supply an identical product (loans). We def ...

... the two types of financial openness yield very different impacts on interest rates, even in this case where they have little effect on aggregate outcomes. In our general equilibrium model, heterogeneous banks compete through their choice of interest rate to supply an identical product (loans). We def ...

Access to Refinancing and Mortgage Interest Rates

... their homes (LTV 95). In all, an estimated 30 percent of mortgage borrowers did not have sufficient equity to refinance their loans in the beginning of 2010 (CoreLogic, 2013). Mounting job losses during the Great Recession put a further dent into household ability to refinance mortgages as lenders w ...

... their homes (LTV 95). In all, an estimated 30 percent of mortgage borrowers did not have sufficient equity to refinance their loans in the beginning of 2010 (CoreLogic, 2013). Mounting job losses during the Great Recession put a further dent into household ability to refinance mortgages as lenders w ...

Consumer Loans in Cambodia - Munich Personal RePEc Archive

... to be negative, while the borrowing for investment in houses, property, and businesses is viewed to be positive and prosperous. This behavior will likely shift over time as newer generations express their interest in such consumer loans, in line with better economic prospect and better financial lit ...

... to be negative, while the borrowing for investment in houses, property, and businesses is viewed to be positive and prosperous. This behavior will likely shift over time as newer generations express their interest in such consumer loans, in line with better economic prospect and better financial lit ...

Loan shark

A loan shark is a person or body who offers loans at extremely high interest rates. The term usually refers to illegal activity, but may also refer to predatory lending with extremely high interest rates such as payday or title loans. Loan sharks sometimes enforce repayment by blackmail or threats of violence. Historically, many moneylenders skirted between legal and extra-legal activity. In the recent western world, loan sharks have been a feature of the criminal underworld.