vsi10 ee Kanniainen 2 13411368 en

... Worldcom, Merck, AOL Time Warner, Xerox and others. The economic recession since 2008 resulting from the uncontrolled financial market sicknesses is not yet over. The oil scandal caused by BP at the Mexican Gulf is a further example. The capitalistic market economy appears as a subject of a paradox: ...

... Worldcom, Merck, AOL Time Warner, Xerox and others. The economic recession since 2008 resulting from the uncontrolled financial market sicknesses is not yet over. The oil scandal caused by BP at the Mexican Gulf is a further example. The capitalistic market economy appears as a subject of a paradox: ...

Implications for Cooperation among OIC Cotton Producing Countries

... their national/regional associations, already know the most challenging problems, and they should be able to take advantage of such an opportunity. As cotton is an important commodity in the world, there are many international entities that represent the interests of cotton producing/trading parties ...

... their national/regional associations, already know the most challenging problems, and they should be able to take advantage of such an opportunity. As cotton is an important commodity in the world, there are many international entities that represent the interests of cotton producing/trading parties ...

krugman_mods_3e_irm_micro_econ_mod20

... 1. Definition: The optimal consumption rule states that when a consumer maximizes utility, the marginal utility per dollar spent must be the same for all goods and services in the consumption bundle. 2. In equation form, the optimal consumption rule for two goods C and P is ...

... 1. Definition: The optimal consumption rule states that when a consumer maximizes utility, the marginal utility per dollar spent must be the same for all goods and services in the consumption bundle. 2. In equation form, the optimal consumption rule for two goods C and P is ...

Answers to the Problems – Chapter 10

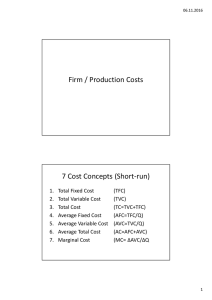

... GM and Ford could decrease their average total cost if they could increase their sales so that they produce more cars and thereby move downward along their average total cost curve. They can also try to shift their average total cost curve downward by closing factories and laying off workers. But th ...

... GM and Ford could decrease their average total cost if they could increase their sales so that they produce more cars and thereby move downward along their average total cost curve. They can also try to shift their average total cost curve downward by closing factories and laying off workers. But th ...

Chapter 8. Production and Cost Start Up: Street Cleaning Around

... factor in the production of vegetables. Suppose you are able to hold constant all other factors—water, sunshine, temperature, fertilizer, and seed—and vary the amount of labor devoted to the garden. How much food could the garden produce? Suppose the marginal product of labor kept increasing or was ...

... factor in the production of vegetables. Suppose you are able to hold constant all other factors—water, sunshine, temperature, fertilizer, and seed—and vary the amount of labor devoted to the garden. How much food could the garden produce? Suppose the marginal product of labor kept increasing or was ...

Chapter 21: Consumer Behavior and Utility Maximization

... B. The utility maximizing rule explains how consumers decide to allocate their money incomes so that the last dollar spent on each product purchased yields the same amount of extra (marginal) utility. A consumer is in equilibrium when utility is “balanced (per dollar) at the margin.” When this is tr ...

... B. The utility maximizing rule explains how consumers decide to allocate their money incomes so that the last dollar spent on each product purchased yields the same amount of extra (marginal) utility. A consumer is in equilibrium when utility is “balanced (per dollar) at the margin.” When this is tr ...

Monopoly and Other Forms of Imperfections

... Perfect Competition An ideal market that maximizes economic ...

... Perfect Competition An ideal market that maximizes economic ...

Implementing efficient graphs in connection networks (EC`11

... We introduce two new properties of implementation. The first property, Pareto Nash implementation (PNI), requires that the efficient outcome always be implemented in a Nash equilibrium and that the efficient outcome Pareto dominates any other Nash equilibrium. The average cost mechanism (AC) and oth ...

... We introduce two new properties of implementation. The first property, Pareto Nash implementation (PNI), requires that the efficient outcome always be implemented in a Nash equilibrium and that the efficient outcome Pareto dominates any other Nash equilibrium. The average cost mechanism (AC) and oth ...

Principles of Economics, Case and Fair,8e

... OLIGOPOLY The Kinked Demand Curve Model kinked demand curve model A model of oligopoly in which the demand curve facing each individual firm has a “kink” in it. The kink results from the assumption that competitor firms will follow if a single firm cuts price but will not follow if a single firm rai ...

... OLIGOPOLY The Kinked Demand Curve Model kinked demand curve model A model of oligopoly in which the demand curve facing each individual firm has a “kink” in it. The kink results from the assumption that competitor firms will follow if a single firm cuts price but will not follow if a single firm rai ...

Cost Curves of the Firm

... Unless it is offset by transport costs, then, a flat or downward-sloping marginal cost curve for a competitive firm is a great theoretical nuisance. For many firms the costs of transport are insignificant. Clothing manufacturers on Seventh Avenue or automobile dealers in Los Angeles or wheat farmers ...

... Unless it is offset by transport costs, then, a flat or downward-sloping marginal cost curve for a competitive firm is a great theoretical nuisance. For many firms the costs of transport are insignificant. Clothing manufacturers on Seventh Avenue or automobile dealers in Los Angeles or wheat farmers ...

utils

... obtain, the less they will desire more units of that product. This can be illustrated with almost any item. ...

... obtain, the less they will desire more units of that product. This can be illustrated with almost any item. ...

pdf version

... property, that it does not become more dear by becoming more scarce, because population always diminishes at the same time that food diminishes, and consequently the quantity of these products demanded, diminishes at the same time as the quantity supplied. Besides, it is not observed that corn is mo ...

... property, that it does not become more dear by becoming more scarce, because population always diminishes at the same time that food diminishes, and consequently the quantity of these products demanded, diminishes at the same time as the quantity supplied. Besides, it is not observed that corn is mo ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑