More Than You Ever Wanted to Know About

... This material is for your private information, and we are not soliciting any action based upon it. This report is not to be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. Certain transactions ...

... This material is for your private information, and we are not soliciting any action based upon it. This report is not to be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. Certain transactions ...

pdf

... quadratic variation / integrated variance, leaving tests of discrete sampling for future research. Realized variance can be traded by means of a variance swap, a contract which pays at time T the difference between realized variance and an agreed fixed leg. The variance swap has become a leading too ...

... quadratic variation / integrated variance, leaving tests of discrete sampling for future research. Realized variance can be traded by means of a variance swap, a contract which pays at time T the difference between realized variance and an agreed fixed leg. The variance swap has become a leading too ...

Pricing and Hedging Volatility Derivatives

... over the life of the volatility derivative. A variance swap has a payoff which is a linear function of the realized variance, a volatility swap has a payoff which is a concave function of the realized variance and a variance call option’s payoff is a convex function of the realized variance. We provide ...

... over the life of the volatility derivative. A variance swap has a payoff which is a linear function of the realized variance, a volatility swap has a payoff which is a concave function of the realized variance and a variance call option’s payoff is a convex function of the realized variance. We provide ...

The Effect of Interest Rate Options Hedging on Term

... position in the underlying asset, and the required size of this position varies with the price of the underlying asset. This variability of the hedge position results from the varying sensitivity of the option’s value to the price of the underlying asset as its price changes. When the underlying ass ...

... position in the underlying asset, and the required size of this position varies with the price of the underlying asset. This variability of the hedge position results from the varying sensitivity of the option’s value to the price of the underlying asset as its price changes. When the underlying ass ...

Interest Rate Variance Swaps and the Pricing of

... income market and serves as the underlying for standardized futures and options contracts for volatility trading. A model-free options-based volatility pricing methodology prices and exchange rates) was branded and popularized as the ogy has been carried over to other markets, such as those for gold ...

... income market and serves as the underlying for standardized futures and options contracts for volatility trading. A model-free options-based volatility pricing methodology prices and exchange rates) was branded and popularized as the ogy has been carried over to other markets, such as those for gold ...

Fourier transform algorithms for pricing and hedging discretely

... realized and implied volatility levels. Unlike equity options, volatility derivatives can provide pure exposure to volatility of the underlying equity. The volatility measure used to define the payoff structures in volatility derivatives may be either the implied volatility derived from option price ...

... realized and implied volatility levels. Unlike equity options, volatility derivatives can provide pure exposure to volatility of the underlying equity. The volatility measure used to define the payoff structures in volatility derivatives may be either the implied volatility derived from option price ...

Lecture 7: Quadratic Variation

... We know that the implied volatility of an at-the-money forward option in the Heston model is lower than the square root of the expected variance (just think of the shape of the implied distribution of the final stock price in Heston). In practice, we start with a strip of European options of a given ...

... We know that the implied volatility of an at-the-money forward option in the Heston model is lower than the square root of the expected variance (just think of the shape of the implied distribution of the final stock price in Heston). In practice, we start with a strip of European options of a given ...

Master`s Thesis Pricing Constant Maturity Swap Derivatives

... be for example a LIBOR rate, on a given notional principal. The amount of the notional, however, is never exchanged. In a standard swap, we exchange a floating short term rate, like a LIBOR rate, against a fixed rate. In a CMS swap, the floating rate is no longer a short term rate, but a swap rate w ...

... be for example a LIBOR rate, on a given notional principal. The amount of the notional, however, is never exchanged. In a standard swap, we exchange a floating short term rate, like a LIBOR rate, against a fixed rate. In a CMS swap, the floating rate is no longer a short term rate, but a swap rate w ...

interest rate swaps - McGraw Hill Higher Education

... specified time in the future at prices specified today. – It’s not an option: both parties are expected to hold up their end of the deal. – If you have ever ordered a textbook that was not in stock, you have entered into a forward contract. ...

... specified time in the future at prices specified today. – It’s not an option: both parties are expected to hold up their end of the deal. – If you have ever ordered a textbook that was not in stock, you have entered into a forward contract. ...

2015-51 - National Association of Insurance Commissioners

... significant in the reporting of derivatives as it is used in calculating other reported amounts (e.g., per SSAP No. 86, unrealized gains and losses, foreign currency premiums, etc.) With regards to futures, although the term “notional” is a reported element in Schedule DB-Part B, it has been communi ...

... significant in the reporting of derivatives as it is used in calculating other reported amounts (e.g., per SSAP No. 86, unrealized gains and losses, foreign currency premiums, etc.) With regards to futures, although the term “notional” is a reported element in Schedule DB-Part B, it has been communi ...

Pricing Volatility Derivatives with General Risk Functions Alejandro Balbás University Carlos III

... equals the variance or volatility swap maturity. In the general case, under very weak assumptions we can also prove that the volatility swap final pay-off is a function depending on ST, underlying price at 41 the option maturity. ...

... equals the variance or volatility swap maturity. In the general case, under very weak assumptions we can also prove that the volatility swap final pay-off is a function depending on ST, underlying price at 41 the option maturity. ...

Interest Rate Models

... that I held in the fall term 2002–2003 at the Department of Operations Research and Financial Engineering at Princeton University. The number of books on fixed income models is growing, yet it is difficult to find a convenient textbook for a one-semester course like this. There are several reasons f ...

... that I held in the fall term 2002–2003 at the Department of Operations Research and Financial Engineering at Princeton University. The number of books on fixed income models is growing, yet it is difficult to find a convenient textbook for a one-semester course like this. There are several reasons f ...

Coupon Blending. Automated. Scalable. Available to ALL Market

... Inc. COMEX is a trademark of Commodity Exchange, Inc. KCBOT, KCBT and Kansas City Board of Trade are trademarks of The Board of Trade of Kansas City, Missouri, Inc. All other trademarks are the property of their respective owners. The information within this presentation has been compiled by CME Gro ...

... Inc. COMEX is a trademark of Commodity Exchange, Inc. KCBOT, KCBT and Kansas City Board of Trade are trademarks of The Board of Trade of Kansas City, Missouri, Inc. All other trademarks are the property of their respective owners. The information within this presentation has been compiled by CME Gro ...

colour ppt

... debt instrument and they have several dimensions • Specifications of the actual debt instrument that will be delivered at a future date • Amount of debt instrument to be delivered • Price (interest-rate) on debt instrument when delivered • Date on which delivery may take place ...

... debt instrument and they have several dimensions • Specifications of the actual debt instrument that will be delivered at a future date • Amount of debt instrument to be delivered • Price (interest-rate) on debt instrument when delivered • Date on which delivery may take place ...

Chapter 1: Intro to Derivatives

... • The Role of the Financial Markets – Financial markets impact the lives of average people all the time, whether they realize it or not o Employer’s prosperity may be dependent upon financing rates o Employer can manage risk in the markets o Individuals can invest and save o Provide diversification ...

... • The Role of the Financial Markets – Financial markets impact the lives of average people all the time, whether they realize it or not o Employer’s prosperity may be dependent upon financing rates o Employer can manage risk in the markets o Individuals can invest and save o Provide diversification ...

Final Exam Preparation

... the intermediary might become the counterparty to the extent of $15 million. That is, the intermediary would warehouse or take a position as a principal to the transaction to make up the $15 million difference between client objectives. To protect itself ...

... the intermediary might become the counterparty to the extent of $15 million. That is, the intermediary would warehouse or take a position as a principal to the transaction to make up the $15 million difference between client objectives. To protect itself ...

securitonomics ii/ cheat sheet on asset and mortgage backed lending

... An interest rate swap is an agreement between two parties to exchange cash flows for a period of time. In a plain vanilla interest rate swap, Company Y agrees to pay Company Z an amount equal to a predetermined, fixed rate of interest on a notional principal amount for a period of time. At the same ...

... An interest rate swap is an agreement between two parties to exchange cash flows for a period of time. In a plain vanilla interest rate swap, Company Y agrees to pay Company Z an amount equal to a predetermined, fixed rate of interest on a notional principal amount for a period of time. At the same ...

Basic interest rate and currency swap products

... The World Bank was raising most of its funds in DM (interest rate = 12%) and Swiss francs (interest rate = 8%). It did not borrow in dollars, for which the interest rate cost was about 17%. Though it wanted to lend out in DM and Swiss francs, the bank was concerned that saturation in the bond market ...

... The World Bank was raising most of its funds in DM (interest rate = 12%) and Swiss francs (interest rate = 8%). It did not borrow in dollars, for which the interest rate cost was about 17%. Though it wanted to lend out in DM and Swiss francs, the bank was concerned that saturation in the bond market ...

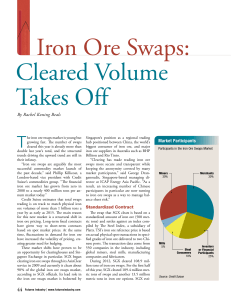

Investment banks to face multi-billion pound CDS claims in

... attempts were made in 2007/2008 to bring those exchanges to market and get them operational. These exchanges would have reduced the credit risk inherent in OTC transactions and would have substantially reduced the transaction costs paid by buy-side market participants and investors. The market for C ...

... attempts were made in 2007/2008 to bring those exchanges to market and get them operational. These exchanges would have reduced the credit risk inherent in OTC transactions and would have substantially reduced the transaction costs paid by buy-side market participants and investors. The market for C ...

PowerPoint Slides

... • Recall that in an interest rate swap, two parties exchange periodic interest payments on a notional principal amount • Typically, one interest rate is a floating rate and the other is the fixed rate • Markets refer to swap positions based on fixed vs. floating position – Purchasing a swap or being ...

... • Recall that in an interest rate swap, two parties exchange periodic interest payments on a notional principal amount • Typically, one interest rate is a floating rate and the other is the fixed rate • Markets refer to swap positions based on fixed vs. floating position – Purchasing a swap or being ...

PowerPoint Slides

... • Recall that in an interest rate swap, two parties exchange periodic interest payments on a notional principal amount • Typically, one interest rate is a floating rate and the other is the fixed rate • Markets refer to swap positions based on fixed vs. floating position – Purchasing a swap or being ...

... • Recall that in an interest rate swap, two parties exchange periodic interest payments on a notional principal amount • Typically, one interest rate is a floating rate and the other is the fixed rate • Markets refer to swap positions based on fixed vs. floating position – Purchasing a swap or being ...

Options

... Often when a market participant suffers a large newsworthy loss, the term “derivatives” is used almost as if it were an explanation ...

... Often when a market participant suffers a large newsworthy loss, the term “derivatives” is used almost as if it were an explanation ...

day 6

... Understanding financial derivatives • The potential gain or loss in value of the derivative is huge. – If the underlying asset is volatile, the derivative is even more volatile because it is so leveraged. – For the interest rate swap, a 1% interest rate change can cause thousands of dollars per yea ...

... Understanding financial derivatives • The potential gain or loss in value of the derivative is huge. – If the underlying asset is volatile, the derivative is even more volatile because it is so leveraged. – For the interest rate swap, a 1% interest rate change can cause thousands of dollars per yea ...