Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

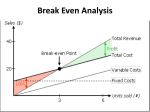

Determining the Price There are two key factors that determine price: the cost of doing business, and the profit that a company hopes to make from the sale of its product or service. All businesses – whether they are retail, wholesale, manufacturing, processing, importing, or service – use these two factors to establish prices. Suppose that a popular DVD on display in HMV's Canadian stores is priced at $29.99. This price means that: HMV expects customers to remit $29.99, plus applicable federal and/or provincial sales taxes, to own this DVD. Customers expect to be charged $29.99 for the DVD at HMV because most popular DVD releases cost approximately the same amount. HMV bought the DVD from a DVD manufacturer for considerably less than $29.99 and added an amount to the cost to reach the $29.99 price. The HMV has to consider both its costs and its amount of money that HMV added to the original cost of the product in order profit projections when it is deciding the price it will charge consumers for its DVDs to cover its business expenses and to make a profit is called markup. It is usually expressed in terms of a percentage of the cost. If a product costs $20 and a store adds a $10 markup to the cost, then the markup percentage on the cost is 50 percent: ($10 ÷ $20) x 100 = 50. HMV will apply the difference between what it paid for the DVD and what it charges its customers to cover store rent, salaries, and other business expenses. As retail stores can pay their expenses only after goods are sold, they prefer to calculate margin instead of markup. Margin is the percentage of the price charged to the consumer that is not used to pay for the cost of the item. If a product sells for $29.99 and costs $20, the store has $9.99 remaining in margin. The margin percentage on the selling price would be 33.3 percent: ($9.99÷$29.99) x 100 = 33.3. If there is any money left over after all the store's expenses are paid, the owners of HMV get to keep it. This is called profit. One formula for calculating profit is markup (margin) - business expenses = profit. The DVD cost the manufacturer much less than $20 to produce. The manufacturing company uses the money it receives from the sale of its products to cover the rent on the factory, salaries, the materials needed to make the DVD (for example, plastic, creative talent, printed liner notes), and other business expenses. If there is money left over, the company keeps it as profit. The manufacturers of the plastic, the people with the creative design talent, and the printing company that prints the liner notes sell their goods and services for more than it costs them to make these goods and provide these services. When price becomes part of the marketing mix, however, other considerations come into play: laws and pricing regulations; the competition's pricing; the position or image the company wants for the product or service; consumer demand; and the marketer's judgment (based on research or intuition) as to what price the market will accept. Break-Even Analysis The first step in calculating the price at which to sell a product or a service is to determine how many units must be sold at a given price to cover operating costs. This is the break-even analysis, and it is only a starting point for setting the actual price. The break-even analysis calculates the break-even point, which is the number of units that a business must sell at a given price to cover its costs. Once the business has covered costs, it can start calculating profit. In order to calculate the break-even point, a business must first calculate its variable costs, fixed costs, and gross profit (contribution margin). Variable Costs Variable costs are most often directly dependent on the quantity of goods sold or services rendered. A hairstylist, for example, might work with eight clients per day. Suppose each client requires 10ml of shampoo and conditioner. The 10ml of shampoo and conditioner costs the business 30 cents. Eight clients would use $2.40 worth of these supplies. If the stylist had 10 clients the next day, the shampoo and conditioner would cost the business $3.30. The cost of the materials that the business uses varies, depending on the number of clients it has. Other sales-dependent variable costs include raw materials, ingredients, cost of goods sold, sales commissions, packaging-material costs, maintenance costs, and shipping costs. Some variable costs, however, are not sales-dependent. For example, carpet-cleaning costs for a retail store vary with the weather. The worse the weather, the higher the cleaning costs because the cleaning has to be done more often. Advertising costs depend on how much advertising a business decides to do. A marketing executive could decide at any time to spend thousands of dollars on a new campaign. Employees vary in their use of supplies, making some supply costs variable. Businesses try to control the variability of these costs by establishing operating budgets, which set spending limits for items such as office supplies and for services such as advertising. Budgets enable a business to establish fixed costs for the purpose of calculating the break-even point. The variable costs of a hair salon include the amount of shampoo, conditioner, and other products required by the stylist to provide customers with the services offered by the business Fixed Costs Fixed costs are constant, independent of sales or other variables. Rent, insurance, salaries, utilities, and administrative costs are all fixed costs. What is important about fixed costs is that they usually remain the same no matter how many items a factory produces or a retail business sells. If, however, a business grows and must add new employees or build new factories, then costs are dependent on the sales. As an example of fixed costs, imagine a video-game company requires 20 employees, for a total daily salary expenditure of $3000. The daily insurance costs are $50. The company pays rent of $100 per day. The cost of utilities works out to $20 per day, administrative costs to $200 per day, and sales costs to $300 per day. The daily fixed costs for the video-game company are $3670. If the company produces 36 700 games in a single day, then the fixed cost for each game is 10 cents. If, on the other hand, the factory closes for a day because of a snowstorm after producing only one game, that game costs $3670 to make. Obviously, the company does not calculate the fixed costs on a daily basis. These calculations are made once or twice per year based on the total costs from the previous time period. Every day, technology companies must pay the fixed costs of their employees’ salaries no matter how many products the company produces on that day Gross Profit Gross profit is the selling price minus the variable costs. In the break-even analysis, it is sometimes referred to as the contribution margin. Both gross profit and the contribution margin refer to the money left over after the variable costs have been paid. This money is used to payoff the fixed costs. For example, each cup of takeout coffee that a restaurant sells might cost 10 cents when the restaurant adds together the cost of the cup, the lid, the coffee, the cream and sugar, the stir stick, and the napkin. These are variable costs, since they are dependent on the number of cups of coffee that the business sells. If the selling price of the cup of coffee is $1.25, then the gross profit is $1.15 ($1.25 - 0.10 = $1.15). The restaurant would then use the $1.15 to pay for its fixed costs. Break-Even Point As stated previously, the break-even point is the number of units that a business must sell at a given price to cover its costs. Once the variable costs have been covered, the only costs remaining are the fixed costs. The only money a business has to cover its fixed costs comes from the gross profit (contribution margin). Therefore, a business can calculate the break-even point by dividing the fixed costs by the gross profit. Break-Even Point (BEP) = Fix Costs ÷ Gross Profit With this formula, a business can determine the level of sales necessary for profit, the results of raising or lowering prices, and the results of increased or decreased sales. For example, a teddy-bear manufacturing company sells its bears to retailers for an average price of $18. The variable costs are $3 per bear. The company's fixed costs are $150 000. To calculate the breakeven point, a firm will use the break-even formula (BEP = fixed costs ÷ gross profit). Gross profit = selling price - variable costs Gross profit = $18 - $3 = $15 Therefore, BEP = $150 000 ÷ $15 = 10 000 bears This means that the company would have to sell 10 000 teddy bears at $15 each before it started to make a profit. The business must decide whether it can wait until it sells that many bears before it becomes profitable. Or, it could Break-Even Analysis: notice how, as the quantity of bears sold increases, the variable costs of the company also increase, but the fixed costs stay the same. The business will only make a profit if sales are above the break-even point. reduce the variable costs to increase the gross profit and reduce the break-even point increase the selling price to increase the gross profit and reduce the break-even point decrease the selling price to increase demand; higher sales might mean that the company can reach the break-even point more quickly increase sales costs, such as advertising and promotion, which may increase demand; higher sales might mean that the company can reach the break-even point more quickly reduce the fixed costs to reduce the break-even point