Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

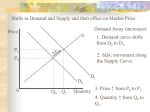

Chapter 6—Prices Section 1—Combining Supply + Demand Supply and Demand work together to determine price -consumers can buy the products they want -producers make enough profit to stay in business -producers respond to changing needs + tastes of consumers Balancing the market Combined Supply + Demand Schedule P of a Slice of Qd Qs Result Pizza $.50 $1.00 $1.50 $2.00 $2.50 $3.00 300 250 200 150 100 50 100 150 200 250 300 350 Shortage From Excess Demand Equilibrium Surplus From Excess Supply -Equilibrium is the point where D + S come together—the point of balance b/t P + Q -at E the market is stable -buyers will purchase exactly as much of the product as firms are willing to sell -Equilibrium can also be illustrated w/ a graph -point at which demand curve intersects supply curve Disequilibrium -Qs is not = to Qd -Excess Demand -Qd is > Qs -when P is below EP...b/c low P encourages buyers + discourages sellers -buyers wait in long lines or go without -sellers raise P -Excess Supply -Qd is < QS -when P is above EP…b/c high P discourages buyers + encourages sellers -Customers will buy less or go elsewhere -sellers lower price -market forces push P toward E Government Intervention -some cases government steps in to control prices -Price Ceilings -maximum price that can be legally charged for a good -usually placed on essential goods that might become too expensive -excess demand and a shortage of goods -cost -long waiting lines…discrimination… bribery… luck are used to allocate goods -luck also becomes factor -sellers try to cut costs to increase income -long waiting lines cause little incentive to improve product -ending price ceilings -more supply for those looking for good -quantity + quality improve -sellers have incentive to improve good. -poorer people may not be able to afford higher price -Price Floors -minimum price that must be paid for a good -most well-known is minimum wage -govt set lowest wage that must be paid for 1 hour of work…states may set it higher -if wage is higher than equilibrium…decrease in employment -excess in supply of workers -agriculture -until 1996 government bought excess crops creating demand when price fell below -Congress abolished programs in 1996 -today subsidies are used Section 2—Changes in Market Equilibrium Changes in Equilibrium Price -Demand changes and Equilibrium Price Changes -When demand increases, price rises-demand curve shifts to the right -when demand decreases, price falls- demand curve shifts to the left -Supply changes and Equilibrium Price Changes -when supply increases, price decreases-supply curve shifts to the right -when supply decreases, price increases-supply curve shifts to the left Changes in Supply and Demand at the same time -Demand increases and Supply increases -increase in demand is greater than increase in supply -demand curve shifts further right than the supply curve shifts to the right -equilibrium price increases -increase in supply is greater than increase in demand -supply curve shifts further right than the demand curve shifts to the right -equilibrium price decreases -increase in demand is equal to increase in supply -both supply and demand curve shift the same amount to the right -equilibrium price remains constant -Demand decreases and Supply decreases -decrease in demand is greater than decrease in supply -demand curve shifts further left than the supply curve shifts to the left -equilibrium price decreases -decrease in supply is greater than decrease in demand -supply curve shifts further left than the demand curve shifts to the left -equilibrium price increases -decrease in demand is equal to decrease in supply -both supply and demand curve shift the same amount to the left -equilibrium price remains constant Importance of Equilibrium Price -keeps buyers purchasing -keeps sellers producing -no shortages -no surpluses Section 3—The Role of Prices Prices in the free market -move land, labor + capital to producers + finished goods to buyers Advantages -Prices as incentives -let consumers know if goods are plentiful or scarce -increase in demand lets producers know to raise -decrease in price lets consumers know to buy -Price as Signals -high prices let producers know that they can produce more -low price lets them know they should produce less -high prices let consumers know they should buy something else -low prices let them know to buy more -Flexibility -prices need to change to solve problems of surplus or shortage -supply shock…sudden shortage of a good -rising prices are the easiest way to solve -Price system is free -distribution based on decisions of consumers Wide choice of goods -allows consumers to choose from similar goods -rationing + shortages -food, metal, rubber during WWII…gasoline in the 1970s…. -short lived hardships -the Black Market -when people do business w/o regard for government controls on price or quantity -allows consumers to buy goods at a higher price when rationing makes it otherwise unavailable Efficient resource allocation -land, labor, capital will be used for their most valuable purposes Prices + the profit incentive -An Inquiry into the Nature and Causes of the Wealth of Nations (1776) -A Smith -explained that it is not b/c of charity that the baker + the butcher provide people w/ food -business find out what people want + then provide it to them -Market Problems -imperfect competition affects prices…higher prices affect decisions to buy -one or few sellers not enough competition to keep prices at costs of production level -spillover costs -externalities…costs of production such as air pollution + water pollution -affects people who have no control over how much of a good is produced -producers don’t pay spillover costs so price is artificially low -imperfect information -when buyers don’t have enough information to make an informed decision