Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

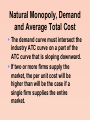

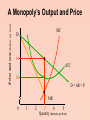

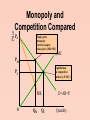

CHAPTER 13 Monopoly Competition and Efficiency Allocative efficiency occurs when no resources are wasted. This means no individual can be made better off without making someone else worse off. In the absence of any obstacles, perfect competition leads to allocative efficiency. Obstacles to Efficiency The three main obstacles to achieving allocative efficiency are: Public goods (national defense) Externalities (external costs and external benefits) Monopoly power Obstacles to Efficiency Public goods are those that can be consumed simultaneously by everyone and from which no one can be excluded. Externalities occur when costs or benefits are conferred on other members of society. Monopoly power is the absence of competition. Public Goods Public goods cannot be provided efficiently by the private market because of the free rider problem. A free rider is someone who consumes a good without paying for it. Because people can consume a public good without paying for it, no one has the incentive to pay for it. Thus, the government has to provide the good and tax everyone to pay for it. Externalities External costs are costs not borne by the producer but borne by other members of society. Pollution imposes external costs. External benefits are benefits accruing to people other than the buyer of a good. Education confers external benefits. Some goods produce both external benefits and costs (e.g., public gardens) Consequences of Externalities When there are external costs, such as pollution, too much of the good is produced in the private market When there are external benefits, such as from education, too little of the good is produced in the private market In both cases, government intervention is warranted to induce less or more of the good to be produced. Possible Government Actions to Deal With Externalities In the case of external costs, tax the private producer or directly restrict production. In the case of external benefits, subsidize the producer or directly provide the good. Monopoly A monopoly is an industry that produces a good or service for which no close substitute exists and in which there is one supplier that is protected from competition by a barrier preventing the entry of new firms. Examples of Monopoly Examples of monopolies include: Local telephone service (Bell South) Water service (Metro-Dade) Cable television The U.S. Postal Service (regular mail) Local Electric Power (FPL) Microsoft (?) Google(?) Facebook (?) eBay (?) Examples of “Monopoly” No Close Substitutes If there are close substitutes for a good or service, that means there is competition in the market. Competition in the market means the market cannot be a monopoly by definition. Innovation, Technological Change, and Substitutes Innovation and technological change create new products, some of which are substitutes for existing products. Example: FedEx, UPS, fax machines, and e-mail are substitutes for the services of the U.S. Postal Service, weakening their monopoly. Example: Satellite TV is a substitute for Cable TV, weakening its monopoly. Barriers to Entry Barriers to entry are legal or natural impediments protecting a firm from competition from potential new entrants. Barriers to entry include: Legal barriers Ownership barriers Natural barriers Of course, firms can create illegal barriers to entry, but this would be a violation of the Sherman Antitrust Act. Legal Barriers to Entry Legal barriers to entry create legal monopoly. A legal monopoly is a market in which competition and entry are restricted by the granting of a public franchise, license, patent or copyright, or in which a firm has legally acquired ownership of a significant portion of a key resource. Legal Barriers: Public Franchises and Licenses A public franchise is an exclusive right granted to a firm to supply a good or service. Example: U.S. Postal Service, Cable TV, FPL A government license controls entry into particular occupations, professions and industries. Example: licensing of medical doctors and lawyers. Legal Barriers: Patents and Copyrights A patent is an exclusive right granted to the inventor of a product or service. Patents are good for 20 years. A copyright is an exclusive right granted to the author or composer of a literary, musical, dramatic, or artistic work. Natural Barriers to Entry Natural barriers to entry give rise to natural monopoly. Natural monopoly occurs when one firm can supply the entire market at a lower price than two or more firms. Demand must limit sales to a quantity at which economies of scale exist. Natural Monopoly, Demand and Average Total Cost The demand curve must intersect the industry ATC curve on a part of the ATC curve that is sloping downward. If two or more firms supply the market, the per unit cost will be higher than will be the case if a single firm supplies the entire market. Price (cents per kilowatt-hour) Natural Monopoly 15 10 5 D = AR = P 0 1 2 3 4 Quantity (millions of kilowatt-hours) Price (cents per kilowatt-hour) Natural Monopoly 15 10 5 ATC D = AR = P 0 1 2 3 4 Quantity (millions of kilowatt-hours) Examples of Natural Monopoly Examples of natural monopoly usually involve economies of scale in distribution: Natural gas distribution systems Electric power distribution Trash collection Cable television Microsoft Monopolies are Regulated Most monopolies are regulated in some way by one or more government agencies. In the case of unregulated monopolies, the government must either break up the monopoly or make some other change to promote competition and economic efficiency. First, we study the operation of unregulated monopoly and how it differs from the operation of competitive markets. Then we discuss pricing strategies for regulated monopolies. Monopoly PriceSetting Strategies Price discrimination is the practice of selling different units of a good or service for different prices. (ex. pizza, airlines) A single-price monopoly is a firm that must sell each unit of its output for the same price. (ex. DeBeers)` Single-Price Monopoly The firm’s demand curve is the market demand curve. Marginal revenue is not the same as the market price. Single-Price Monopoly Bobbie’s Barbershop, in Cairo, Nebraska is the sole supplier of haircuts in town. Let’s examine the market for haircuts in Cairo. Demand and Marginal Revenue a b c d e f Price (P) Quantity demanded (Q) (dollars per haircut) (haircuts per hour) 20 18 16 14 12 10 0 1 2 3 4 5 Total revenue (TR=P Q) (dollars 0 18 32 42 48 50 Marginal revenue ( MR TR / Q ) (dollars per additional haircut) Demand and Marginal Revenue a b c d e f Price (P) Quantity demanded (Q) (dollars per haircut) (haircuts per hour) 20 18 16 14 12 10 0 1 2 3 4 5 Total revenue (TR=P Q) (dollars 0 18 32 42 48 50 Marginal revenue ( MR TR / Q ) (dollars per additional haircut) - Demand and Marginal Revenue a b c d e f Price (P) Quantity demanded (Q) (dollars per haircut) (haircuts per hour) 20 18 16 14 12 10 0 1 2 3 4 5 Total revenue (TR=P Q) (dollars 0 18 32 42 48 50 Marginal revenue ( MR TR / Q ) (dollars per additional haircut) 18 Demand and Marginal Revenue a b c d e f Price (P) Quantity demanded (Q) (dollars per haircut) (haircuts per hour) 20 18 16 14 12 10 0 1 2 3 4 5 Total revenue (TR=P Q) (dollars 0 18 32 42 48 50 Marginal revenue ( MR TR / Q ) (dollars per additional haircut) 18 14 Demand and Marginal Revenue a b c d e f Price (P) Quantity demanded (Q) (dollars per haircut) (haircuts per hour) 20 18 16 14 12 10 0 1 2 3 4 5 Total revenue (TR=P Q) (dollars 0 18 32 42 48 50 Marginal revenue ( MR TR / Q ) (dollars per additional haircut) 18 14 10 Demand and Marginal Revenue a b c d e f Price (P) Quantity demanded (Q) (dollars per haircut) (haircuts per hour) 20 18 16 14 12 10 0 1 2 3 4 5 Total revenue (TR=P Q) (dollars 0 18 32 42 48 50 Marginal revenue ( MR TR / Q ) (dollars per additional haircut) 18 14 10 6 Demand and Marginal Revenue a b c d e f Price (P) Quantity demanded (Q) (dollars per haircut) (haircuts per hour) 20 18 16 14 12 10 0 1 2 3 4 5 Total revenue (TR=P Q) (dollars 0 18 32 42 48 50 Marginal revenue ( MR TR / Q ) (dollars per additional haircut) 18 14 10 6 2 (dollars per haircut) Price & marginal revenue Demand and Marginal Revenue Quantity (haircuts per hour) (dollars per haircut) Price & marginal revenue Demand and Marginal Revenue MR D Quantity (haircuts per hour) (dollars per haircut) Price & marginal revenue Demand and Marginal Revenue 20 Total revenue loss $4 c 16 d 14 Price falls from $16 to $14 Quantity rises from 2 to 3 MR 2 D 3 Quantity (haircuts per hour) (dollars per haircut) Price & marginal revenue Demand and Marginal Revenue 20 Total revenue loss $4 c 16 d 14 Total revenue gain $14 Price falls from $16 to $14 Quantity rises from 2 to 3 MR 2 D 3 Quantity (haircuts per hour) (dollars per haircut) Price & marginal revenue Demand and Marginal Revenue 20 Total revenue loss $4 c 16 d 14 Total revenue gain $14 10 Marginal revenue $10 MR 2 D 3 Quantity (haircuts per hour) Price falls from $16 to $14 Quantity rises from 2 to 3 A Monopoly’s Output and Price Decision Price (P) Quantity Total demanded revenue (Q) (TR = P Q) (dollars per haircut)(haircuts/hour) (dollars) Marginal revenue ( MR TR / Q ) (dollars per add. haircut) 20 0 0 - 18 1 18 18 16 2 32 14 14 3 42 10 12 4 48 6 10 5 50 2 Marginal Total cost cost ( MC TC / Q ) Profit (TC) (dollars per (TR – TC) (dollars) add. haircut) (dollars) A Monopoly’s Output and Price Decision Price (P) Quantity Total demanded revenue (Q) (TR = P Q) (dollars per haircut)(haircuts/hour) (dollars) Marginal revenue ( MR TR / Q ) (dollars per add. haircut) Marginal Total cost cost ( MC TC / Q ) Profit (TC) (dollars per (TR – TC) (dollars) add. haircut) 20 0 0 - 20 18 1 18 18 21 16 2 32 14 24 14 3 42 10 30 12 4 48 6 40 10 5 50 2 55 (dollars) A Monopoly’s Output and Price Decision Price (P) Quantity Total demanded revenue (Q) (TR = P Q) (dollars per haircut)(haircuts/hour) (dollars) Marginal revenue ( MR TR / Q ) (dollars per add. haircut) Marginal Total cost cost ( MC TC / Q ) Profit (TC) (dollars per (TR – TC) (dollars) add. haircut) 20 0 0 - 20 18 1 18 18 21 16 2 32 14 24 14 3 42 10 30 12 4 48 6 40 10 5 50 2 55 - (dollars) A Monopoly’s Output and Price Decision Price (P) Quantity Total demanded revenue (Q) (TR = P Q) (dollars per haircut)(haircuts/hour) (dollars) Marginal revenue ( MR TR / Q ) (dollars per add. haircut) Marginal Total cost cost ( MC TC / Q ) Profit (TC) (dollars per (TR – TC) (dollars) add. haircut) 20 0 0 - 20 - 18 1 18 18 21 1 16 2 32 14 24 14 3 42 10 30 12 4 48 6 40 10 5 50 2 55 (dollars) A Monopoly’s Output and Price Decision Price (P) Quantity Total demanded revenue (Q) (TR = P Q) (dollars per haircut)(haircuts/hour) (dollars) Marginal revenue ( MR TR / Q ) (dollars per add. haircut) Marginal Total cost cost ( MC TC / Q ) Profit (TC) (dollars per (TR – TC) (dollars) add. haircut) 20 0 0 - 20 - 18 1 18 18 21 1 16 2 32 14 24 3 14 3 42 10 30 12 4 48 6 40 10 5 50 2 55 (dollars) A Monopoly’s Output and Price Decision Price (P) Quantity Total demanded revenue (Q) (TR = P Q) (dollars per haircut)(haircuts/hour) (dollars) Marginal revenue ( MR TR / Q ) (dollars per add. haircut) Marginal Total cost cost ( MC TC / Q ) Profit (TC) (dollars per (TR – TC) (dollars) add. haircut) 20 0 0 - 20 - 18 1 18 18 21 1 16 2 32 14 24 3 14 3 42 10 30 6 12 4 48 6 40 10 5 50 2 55 (dollars) A Monopoly’s Output and Price Decision Price (P) Quantity Total demanded revenue (Q) (TR = P Q) (dollars per haircut)(haircuts/hour) (dollars) Marginal revenue ( MR TR / Q ) (dollars per add. haircut) Marginal Total cost cost ( MC TC / Q ) Profit (TC) (dollars per (TR – TC) (dollars) add. haircut) 20 0 0 - 20 - 18 1 18 18 21 1 16 2 32 14 24 3 14 3 42 10 30 6 12 4 48 6 40 10 10 5 50 2 55 (dollars) A Monopoly’s Output and Price Decision Price (P) Quantity Total demanded revenue (Q) (TR = P Q) (dollars per haircut)(haircuts/hour) (dollars) Marginal revenue ( MR TR / Q ) (dollars per add. haircut) Marginal Total cost cost ( MC TC / Q ) Profit (TC) (dollars per (TR – TC) (dollars) add. haircut) 20 0 0 - 20 - 18 1 18 18 21 1 16 2 32 14 24 3 14 3 42 10 30 6 12 4 48 6 40 10 10 5 50 2 55 15 (dollars) A Monopoly’s Output and Price Decision Price (P) Quantity Total demanded revenue (Q) (TR = P Q) (dollars per haircut)(haircuts/hour) (dollars) Marginal revenue ( MR TR / Q ) (dollars per add. haircut) Marginal Total cost cost ( MC TC / Q ) Profit (TC) (dollars per (TR – TC) (dollars) add. haircut) 20 0 0 - 20 - 18 1 18 18 21 1 16 2 32 14 24 3 14 3 42 10 30 6 12 4 48 6 40 10 10 5 50 2 55 15 (dollars) -20 A Monopoly’s Output and Price Decision Price (P) Quantity Total demanded revenue (Q) (TR = P Q) (dollars per haircut)(haircuts/hour) (dollars) Marginal revenue ( MR TR / Q ) (dollars per add. haircut) Marginal Total cost cost ( MC TC / Q ) Profit (TC) (dollars per (TR – TC) (dollars) add. haircut) (dollars) 20 0 0 - 20 - -20 18 1 18 18 21 1 -3 16 2 32 14 24 3 14 3 42 10 30 6 12 4 48 6 40 10 10 5 50 2 55 15 A Monopoly’s Output and Price Decision Price (P) Quantity Total demanded revenue (Q) (TR = P Q) (dollars per haircut)(haircuts/hour) (dollars) Marginal revenue ( MR TR / Q ) (dollars per add. haircut) Marginal Total cost cost ( MC TC / Q ) Profit (TC) (dollars per (TR – TC) (dollars) add. haircut) (dollars) 20 0 0 - 20 - -20 18 1 18 18 21 1 -3 16 2 32 14 24 3 +8 14 3 42 10 30 6 12 4 48 6 40 10 10 5 50 2 55 15 A Monopoly’s Output and Price Decision Price (P) Quantity Total demanded revenue (Q) (TR = P Q) (dollars per haircut)(haircuts/hour) (dollars) Marginal revenue ( MR TR / Q ) (dollars per add. haircut) Marginal Total cost cost ( MC TC / Q ) Profit (TC) (dollars per (TR – TC) (dollars) add. haircut) (dollars) 20 0 0 - 20 - -20 18 1 18 18 21 1 -3 16 2 32 14 24 3 +8 14 3 42 10 30 6 +12 12 4 48 6 40 10 10 5 50 2 55 15 A Monopoly’s Output and Price Decision Price (P) Quantity Total demanded revenue (Q) (TR = P Q) (dollars per haircut)(haircuts/hour) (dollars) Marginal revenue ( MR TR / Q ) (dollars per add. haircut) Marginal Total cost cost ( MC TC / Q ) Profit (TC) (dollars per (TR – TC) (dollars) add. haircut) (dollars) 20 0 0 - 20 - -20 18 1 18 18 21 1 -3 16 2 32 14 24 3 +8 14 3 42 10 30 6 +12 12 4 48 6 40 10 +8 10 5 50 2 55 15 A Monopoly’s Output and Price Decision Price (P) Quantity Total demanded revenue (Q) (TR = P Q) (dollars per haircut)(haircuts/hour) (dollars) Marginal revenue ( MR TR / Q ) (dollars per add. haircut) Marginal Total cost cost ( MC TC / Q ) Profit (TC) (dollars per (TR – TC) (dollars) add. haircut) (dollars) 20 0 0 - 20 - -20 18 1 18 18 21 1 -3 16 2 32 14 24 3 +8 14 3 42 10 30 6 +12 12 4 48 6 40 10 +8 10 5 50 2 55 15 -5 A Monopoly’s Output and Price Decision Price (P) Quantity Total demanded revenue (Q) (TR = P Q) (dollars per haircut)(haircuts/hour) (dollars) Marginal revenue ( MR TR / Q ) (dollars per add. haircut) Marginal Total cost cost ( MC TC / Q ) Profit (TC) (dollars per (TR – TC) (dollars) add. haircut) (dollars) 20 0 0 - 20 - -20 18 1 18 18 21 1 -3 16 2 32 14 24 3 +8 14 3 42 10 30 6 +12 12 4 48 6 40 10 +8 10 5 50 2 55 15 -5 (dollars per hour) Total revenue and total cost A Monopoly’s Output and Price 50 40 30 20 10 0 1 2 3 4 5 Quantity (haircuts per hour) (dollars per hour) Total revenue and total cost A Monopoly’s Output and Price TR 50 40 Note TR curve is not linear like it is in perfect competition 30 20 10 0 1 2 3 4 5 Quantity (haircuts per hour) (dollars per hour) Total revenue and total cost A Monopoly’s Output and Price TR 50 40 Note slope of TR curve (which is MR) declines as Q increases 30 20 10 0 1 2 3 4 5 Quantity (haircuts per hour) (dollars per hour) Total revenue and total cost A Monopoly’s Output and Price TC TR 50 40 Note slope of TC curve is MC 30 20 10 0 1 2 3 4 5 Quantity (haircuts per hour) (dollars per hour) Total revenue and total cost A Monopoly’s Output and Price TC TR 50 40 Note MC increases with Q because of diminishing returns 30 20 10 0 1 2 3 4 5 Quantity (haircuts per hour) (dollars per hour) Total revenue and total cost A Monopoly’s Output and Price 50 Economic profit = $12 TC TR 42 30 20 10 0 1 2 3 4 5 Quantity (haircuts per hour) (dollars per hour) Total revenue and total cost A Monopoly’s Output and Price 50 Economic profit = $12 TC TR 42 30 Note that at maximum profits slope of TR = slope of TC (or MR=MC) 20 10 0 1 2 3 4 5 Quantity (haircuts per hour) Price and cost (dollars per hour) A Monopoly’s Output and Price 20 14 10 D = AR = P 0 1 2 3 4 5 Quantity (haircuts per hour) Price and cost (dollars per hour) A Monopoly’s Output and Price 20 14 10 D = AR = P MR 0 1 2 3 4 5 Quantity (haircuts per hour) Price and cost (dollars per hour) A Monopoly’s Output and Price MC 20 14 10 D = AR = P MR 0 1 2 3 4 5 Quantity (haircuts per hour) Price and cost (dollars per hour) A Monopoly’s Output and Price MC 20 14 ATC D = AR = P MR 0 1 2 3 4 5 Quantity (haircuts per hour) Price and cost (dollars per hour) A Monopoly’s Output and Price MC 20 14 ATC D = AR = P TR = 14x3 = 42 MR 0 1 2 3 4 5 Quantity (haircuts per hour) Price and cost (dollars per hour) A Monopoly’s Output and Price MC 20 14 ATC 10 D = AR = P MR 0 1 2 3 4 5 Quantity (haircuts per hour) Price and cost (dollars per hour) A Monopoly’s Output and Price MC 20 14 ATC 10 D = AR = P TC = 10x3 = 30 MR 0 1 2 3 4 5 Quantity (haircuts per hour) Price and cost (dollars per hour) A Monopoly’s Output and Price MC 20 Profit = $12 ($4 x 3 units) 14 ATC Economic profit = $12 10 D = AR = P MR 0 1 2 3 4 5 Quantity (haircuts per hour) Monopoly Profits A positive profit is still not guaranteed, even for a monopoly. Total profit depends on the position of the ATC curve relative to the demand curve. However, we don’t see many unprofitable monopolies. If you’re the sole supplier of a good and still can’t make a profit, how long will you stay in the business? Rent Seeking Because a monopoly creates economic profit in the long-run, people devote a lot of effort to obtain monopoly rights. This activity is called rent seeking. The firm is attempting to capture some of the consumer surplus for itself. Comparing Monopoly and Competition How do the quantities produced, prices, and profits of a monopoly compare with those of a perfectly competitive industry? Consider a hypothetical example of a perfectly competitive industry which suddenly becomes a monopoly. Comparison of Monopoly and Perfect Competition Compared to a perfectly competitive market, a single-price monopoly restricts its output and charges a higher price. Price and Output A perfectly competitive industry will produce the quantity of output and charge the price at the equilibrium point where the industry MC curve intersects the demand curve. A monopoly will produce the quantity of output dictated by the intersection of the MR and MC curves, charging a price set by the demand curve. Price Monopoly and Competition Compared PA Single-price monopoly restricts output, raises price (MR=MC) S,MC PM Equilibrium in competitive industry (P=MC) PC MR 0 QM QC D=AR=P Quantity Price Inefficiency of Monopoly PA Consumer Surplus under Competition Perfect Competition S, MC PC D=AR=P 0 QC Quantity Price Inefficiency of Monopoly PA Consumer Surplus under Competition Perfect Competition S, MC Producer Surplus under Competition PC D=AR=P 0 QC Quantity Price Inefficiency of Monopoly PA Consumer Surplus under Monopoly Monopoly S, MC PM PC Producer Surplus under Monopoly MR 0 QM QC D=AR=P Quantity Price Inefficiency of Monopoly PA Consumer Surplus under Monopoly Monopoly S, MC PM Deadweight loss in Consumer Surplus PC Monopoly’s gain in Producer Surplus MR 0 QM QC D=AR=P Quantity Price Inefficiency of Monopoly PA Consumer Surplus under Monopoly Monopoly S, MC PM Deadweight loss in Consumer Surplus PC Monopoly’s gain in Producer Surplus Deadweight loss in Producer Surplus MR 0 QM QC D=AR=P Quantity Price Inefficiency of Monopoly Assuming Constant Marginal Cost PA Consumer Surplus Under Competition PC Perfect Competition S, MC D=AR=P 0 QC Quantity Price Inefficiency of Monopoly Assuming Constant Marginal Cost PA Consumer Surplus under Monopoly Monopoly PM S, MC PC MR 0 QM QC D=AR=P Quantity Price Inefficiency of Monopoly Assuming Constant Marginal Cost PA Consumer Surplus under Monopoly Monopoly Loss in Consumer Surplus under Monopoly PM S, MC PC MR 0 QM QC D=AR=P Quantity Price Inefficiency of Monopoly Assuming Constant Marginal Cost PA Consumer Surplus under Monopoly Monopoly PM S, MC PC Monopoly’s gain in Producer Surplus MR 0 QM QC D=AR=P Quantity Price Inefficiency of Monopoly Assuming Constant Marginal Cost PA Consumer Surplus under Monopoly Monopoly Deadweight loss Under Monopoly PM S, MC PC Monopoly’s gain in Producer Surplus MR 0 QM QC D=AR=P Quantity Monopoly Policy Issues Regulating Natural Monopoly When demand and cost conditions create natural monopoly, government agencies regulate the monopoly. This figure shows how a natural monopoly might be regulated. Monopoly Policy Issues With no regulation, the monopoly maximizes profit. It produces the quantity at which marginal revenue equals marginal cost. In this case, profits=$4, calculated as (P-ATC)xQ=(20-18)x2=$4 Monopoly Policy Issues This regulation is the marginal cost pricing rule, and it results in an efficient use of resources. Regulating a natural monopoly in the public interest sets output where MB = MC and thus the price equal to marginal cost (D=AR=P=MC). 14 Monopoly Policy Issues But with price equal to marginal cost, ATC exceeds price and the monopoly incurs an economic loss. In this case, the loss=$16, calculated as (P-ATC)xQ=(10-14)x4=-$16 If the monopoly receives a subsidy to cover its loss, taxes must be imposed on other economic activity, which create deadweight loss. 14 Monopoly Policy Issues Where possible, a regulated natural monopoly might be permitted to price discriminate to cover the loss from marginal cost pricing. Another alternative (which is easy to implement in practice) is to produce the quantity at which price equals average total cost and to set the price equal to average total cost—the average cost pricing rule (P=ATC). With this pricing rule, the natural monopoly earns only normal profits (economic profits are zero). This is because (PATC)xQ=(15-15)x3=0