Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

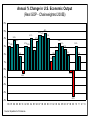

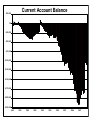

Institute for Supply Management, ISM Manufacturing Index (Measure of Manufacturing Activity) Web: http://www.ism.ws/ISMReport/index.cfm No monthly revisions,…but reassessments of seasonal adjustment factors in January ISM is a private, Tempe, Arizona based group that represents corporate purchasing managers – procure production materials and supplies to make products – in the goods-producing industry – highly sensitive to the ebb and flow overall economic activity. Survey results come out the first business day of every month (very timely) ISM surveys 400 companies, representing 20 industries, to assess if activity is rising, falling or unchanged in the following fields: New Orders (30%) - by purchasing agents Production (25%) - manufacturing output Employment (20%) – hiring by the company Supplier deliveries/Vendor performance (15%) – speed of supplier delivery Inventories (10%) – the rate of liquidating manufacturers’ inventories Purchasing Managers Index (PMI) is a compilation of the 5 components listed above weighted by the given percentages. The PMI is a diffusion index, showing changes in month to month activity, but not actual levels of production. Component number = % reporting rising + ½ % reporting no change PMI is an effective gauge of business cycle turning points If PMI > 60 for a sustainable period with the economy operating above potential => Fed raising interest rates If PMI > 50 => expanding manufacturing sector, with every additional full index point adding 0.3 percentage points of economic growth over next 12 months. If PMI = 50 => no change in manufacturing activity, with DY/Y = 2.5% If 43 < PMI < 50 => contracting manufacturing sector, but economy may still be growing If PMI < 43 on a sustained basis => recession. Expect Fed to lower interest rates. ISM Non-Manufacturing Business Activity Index – measures service sector business activity (non-manufacturing industries represent 80% of economy) Service sector (medical care, communication, financial, consulting, entertainment, legal, insurance, lodging) is not as cyclical as manufacturing A reading of 50 shows the same percentage of managers reporting higher activity as lower activity Index > 50 indicates growth in service industry Index < 50 indicates contraction in service industry ------------------------------------------------------------------------------------------------------------------------------------------------------------------ Market Analysis: Bonds: PMI > 50 and Y > YPot => DP/P => DBonds => iBonds Stocks: PMI > 50 and Y < YPot => DY/Y => profits => PStocks Dollar: PMI < 50 => DY/Y => iBonds => dollar ISM Purchasing Managers Index (SA) 70 70 65 65 60 60 55 55 50 50 45 45 40 40 Recession 35 Manufacturing Activity 35 No Change in Manufacturing Activity 30 30 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 Annual % Change in U.S. Economic Output (Real GDP - Chainweighted 2005$) 6% 4.8% 5% 4.5% 4.4% 4.1% 4.1% 3.8% 4% 3.7% 3.5% 3.4% 3.1% 3% 2% 3.1% 2.9% 3.1% 2.9% 2.5% 2.5% 1.8% 1.8% 3.0% 2.7% 1.9% 1.7% 1.1% 1% 0% -1% -0.5% -0.3% -2% -3% -3.5% -4% 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 Source: Department of Commerce. Keynesian ISLM Model Model Explains 2 things: 1. Determination of Output, Y 2. Why Ye < YFE Aggregate Expenditure Model: focuses on the relationship between spending (AE) and production (Y) assuming fixed price level. (nominal = real) => DY without D P AE = C + I + G + X-M Macroeconomic Equilibrium AE = Y (no D in inventories => no D in production rate) Assume no organic DY/Y %D(Y/L) = 0 DL/L = 0 Domestic Production, GDP, Y Foreign Production, M Macro Equilibrium Y = AE Inventory AE = C + I + G + X Equilibrium Condition Inflow = Outflow QS = QD The Circular Flow Diagram AE = C+I+G+X-M Recent U.S. Economic Performance Housing Market Contraction AE = Y AEE06 AE05 Series of induced C Multiplier Effect AE06 DY DY DC DC Inventory => Homebuilders’ Y D Autonomous Spending •Low pent up demand •Fewer investors •Tighter underwriting •Higher interest rates •Expected lower future home prices Y08 Y05Pot Y06 Recession Optimism => Firm’s production Unplanned housing inventory accumulation Y Output Income Falling Home Prices Negative Downward Spiral Falling Household Wealth Falling Household Spending HELOC •Salaries •Commissions •Bonuses •Tips Lower income •Self-reinforcing spiral •Feedback Loop •Multiplier Effect •Sum of an Infinite Geometric Series Increase unemployment Rising Inventories Lower Factory Production Real Personal Consumption Expenditures (% chg from quarter one year ago) 16 16 Total average growth = 3.3% 13 . 73 (Furniture, appliances, autos) average growth = 6.0% (14%) (Food, clothing, energy) average growth = 3.4% (29%) 12 10 . 78 11. 0 4 8 .8 7 7. 8 3 8 3 .2 4 2 . 52 4 7. 3 6 .4 5. 55. 1 4 .5 6 .6 2 .4 3 1. 2 2 0 . 77 12 8 .3 5 6 . 73 5. 53 5. 9 4 5. 2 5 4 . 72 Services average growth = 2.8% (57%) (Housing, transportation, medical care, recreation) 10 8 6 .3 5. 4 4 . 44 . 64 . 6 3 .6 4 4 2 . 1 2 . 32 . 3 0 .8 0 0 0 0 Q1 0 1Q 1 0 2 Q1 0 3 Q1 0 4 Q1 0 5Q 1 0 6 Q1 0 7Q 1 0 8 Q1 - 1. 2 0 9 Q1 - 1. 5 -4 -4 - 5. 4 -8 -8 - 8 .-98 . 8 -12 - 11. 8 -16 -12 -16 Durable Nondurable Total Services D Autonomous Expenditure (Intercept) => multiple D Y Consumption: 1. 2. 3. 4. Household Wealth PAssets => Wealth => C Expected Future Income YEt+1 => Ct Price level P => W/P (real wealth) => C Interest rate r =>cost of borrowing => Cdurables Investment: 1. 2. 3. 4. PE(t+1) Cost of Capital Taxes Cash flow Animal Spirits, business confidence Real long-term interest rates Retained earnings, profits Net Exports: 1. PLU.S./PLROW 2. (DY/Y)U.S. / (DY/Y)ROW 3. Exchange rate PL U.S. => NX (YU.S. / YROW ) => NX (e/$ ) => NX Current Account Balance $25,000 $0 -$25,000 -$50,000 -$75,000 -$100,000 -$125,000 -$150,000 -$175,000 -$200,000 -$225,000 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 ISM-Chicago Business Barometer Index (BBI) (Measure of Manufacturing Activity in the Midwest Region) Web: https://www.ism-chicago.org/index.cfm? Reassessments of seasonal adjustment factors in January The Chicago chapter is an affiliate (one of ten local ISM chapters) of the Institute for Supply Management, (ISM). The Chicago group publishes their survey one business day before the national ISM manufacturing number is released. The Chicago Business Barometer Index, BBI, moves in same direction as the national ISM numbers about 60% of the time and has a 90% correlation regarding their magnitude change. But for financial market traders, the direction is more relevant than the level of change. Survey region covers the industrial heartland of Illinois, Indiana and Michigan, which contains a large part of the auto and auto parts sectors. The Federal Reserve monitors the Chicago NAPM report to study conditions in the manufacturing sector and check for signs of production imbalances. ISM-Chicago, queries 200 purchasing managers regarding their business activity to assess if activity is rising, falling or unchanged. Survey results are compiled into a diffusion index, (BBI), based on a weighted average of 5 subcomponent indexes: New Orders (35% weight) - by purchasing agents Production (25% weight) - manufacturing output Employment (10% weight) – hiring by the company Supplier deliveries/Vendor performance (15% weight) – speed of supplier delivery Order backlogs (15% weight) The Business Barometer Index (BBI) is a compilation of the 5 components listed above weighted by the given percentages. The BBI is a diffusion index, showing changes in month to month activity, but not actual levels of production. Component number = % reporting rising + ½ % reporting no change The difference between % reporting rising and % reporting falling: ( % - %) = (Index - 50) x 2. (Recall, 100% = % + no chg % + % and Index = % + ½ (no chg %) ISM-Chicago is an effective gauge of business cycle turning points: If BBI > 50 indicates expansion in business activity. If BBI < 50 indicates contraction in business activity. Data for the Chicago BBI is not the same data used to calculate the National ISM Index. ------------------------------------------------------------------------------------------------------------------------------------------------------------------ Market Analysis: Bonds: Unexpected BBI => DY/Y => DP/P => DBonds => iBonds Stocks: Unexpected BBI => DY/Y => profits => PStocks However if Y > YPot and BBI => expected interest rates by Fed. Res => PStocks Dollar: BBI => DY/Y => profits & interest rates => Ddollar => $ ISM Chicago (Diffusion Index, SA) 75 75 70 70 65 65 60 60 55 55 50 50 45 45 40 40 Recession Chicago Index 35 35 No Change in Manufacturing Activity 30 30 00 01 02 03 04 05 06 07 08 09 10 11 12 13