Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

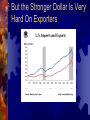

The Economy 2010 and How We Got Here Steven L. Cobb, Ph.D. UNT Center for Economic Education The U.S. Economy is on a Trajectory of Slow, but Improving Growth for 2010 Guitar-string theory: Deeper recessions are followed by stronger, more rapid recoveries. -Milton Friedman “The aftermath of deep financial crises shows deep and lasting effects on asset prices, output and employment. Unemployment and house price declines extend out for five and six years. Output declines last two years on average. Even recessions sparked by financial crises do eventually end, albeit almost invariably accompanied by massive increases in government debt.” -Reinhart and Rogoff(Dec. ‘08) The Current Situation GDP: 2-3%, more likely close to 3% Absent the financial crisis: 5-6% Headline inflation: 3.0% Core inflation: 1.5% Unemployment: 10.4% peak in 2010 Q2 Sustained employment growth to begin after Feb. 2010 What have we experienced? High unemployment Actual deflation Negative wealth shock Bursting of multiple bubbles Near-demise system of banking/financial Unemployment and Deflation High Unemployment High Unemployment Deflationary Fears Negative Wealth Shocks The Bursting of the Housing Bubble A Softening of the Housing Market As A Result Of Higher Interest Rates (’04 – ’07) The Inevitable Was Delayed By New Mortgage Instruments By 2006 Real Estate Prices Were No Longer Rising Sales of New and Existing Homes Fall Rapidly Construction Falls As Well The Consumption Bubble Also Burst GDP Growth Was Fueled By Consumption Expenditures As Long As Home Prices Were Rising, Consumers Were Using Equity To Finance Their Purchases Real Estate Concerns Negatively Impacted Consumer Confidence Falling Confidence Led To Falling Sales Consumption Fell in Both Nominal and Real Terms Falling Consumption Led to Declines In Retail Sales Global Shocks The Downturn Was Global The Largest Economies Were All Hit Hard The Trend Was Similar In Established and Rising Stars The US Experiences a Rise in the Value of the Dollar But the Stronger Dollar Is Very Hard On Exporters The Result of All This Is the Near Demise of the Financial System What have we experienced? This Recession is the most painful since the Great Depression Longest, Deep, and Wide It followed 25 years of growth interrupted by two short, mild recessions Bottom Line: Relative to a generation of experience, this was a truly traumatic event. Headwinds Credit to households and small businesses Banking system –Capital, Commercial Real Estate losses Anticipated taxes Policy uncertainty Higher energy prices Crosswinds Monetary policy Fiscal policy Regulatory policy Tailwinds Growth in temporary employment Declining initial unemployment claims Declining layoff announcements Employment gains in 11 states 11 sectors showing employment gains Synchronized global recovery Industrial production bounce-back Positives 2007 2008 2009 U.S. GDP Growth 2007 2008 2009 Low to Moderate Inflation Year-end inflation? Given fears of deflation at year-end 2008, economists thought a 1% deflation over 2009 was the most likely outcome. Federal Reserve Policy averted that outcome, and that’s a prediction we’re very happy to have been wrong about. Credit Chairman Bernanke and the FOMC Consumer Behavior After a number of years where the U.S. saving rate was negative, there is an indication that Americans are beginning to save again. This has the potential to be one of the more positive impacts of the recession. Remaining Concerns Unemployment not have peaked – some expect it to hit 10.4% in the second quarter of this year. Doesn’t measure discouraged workers and part-time workers that want full time jobs (may currently be as high as 16.3%) Some economists still fear a jobless recovery May Budget Deficits The spending measures may have been critical to avoiding a much larger crisis, but our national debt is rising rapidly. It is now over $12 Trillion (more than $40,000 per citizen) Current deficits are adding to this number at record rates Long-term concerns have been put on the back burner Social Security Medicare Lessons Learned Only traumatic events, not hiccups, produce behavior modification. What is the Bottom Line? The circulation of confidence is better than the circulation of money. -James Madison