Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

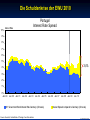

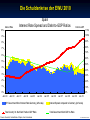

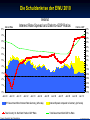

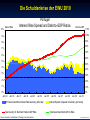

© RAINER MAURER, Pforzheim Die Schuldenkrise der EWU 2010 Prof. Dr. Rainer Maure -1- Die Schuldenkrise der EWU 2010 ➤ Die Rückkehr der Zinsdifferenzen: Nach der Gründung der Europäischen Währungsunion (EMU) verschwanden die Zinsdifferenzen zwischen den Mitgliedsländern beinahe vollständig. ■ Gegen Ende des Jahres 2008 kehrten sie zurück. ■ Bei den Krisenländern Spanien, Irland, Portugal und Griechenland sind diese Differenzen mittlerweile sehr groß geworden, wie die folgenden Schaubilder zeigen: © RAINER MAURER, Pforzheim ■ Prof. Dr. Rainer Maure -3- Die Schuldenkrise der EWU 2010 10% Spain Interest Rate Spread Interest Rate 9% 8% 7% 6% 5% 4% 2,0% 3% 2% 1% © RAINER MAURER, Pforzheim 0% Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 10Y Government Bond Interest Rate Germany (left scale) Source: Eurostat, Central Bank of Spain, Own Calculations Prof. Dr. Rainer Maure Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 Interest Spread compared to Germany (left scale) -4- © www.rainer-maurer.com Die Schuldenkrise der EWU 2010 Ireland Interest Rate Spread 10% Interest Rate 9% 8% 7% 6% 5% 4% 2,5% 3% 2% 1% © RAINER MAURER, Pforzheim 0% Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 10Y Government Bond Interest Rate Germany (left scale) Prof. Dr. Rainer Maure Source: Eurostat, Own Calculations Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 Interest Spread compared to Germany (left scale) -5- © www.rainer-maurer.com Die Schuldenkrise der EWU 2010 10% Portugal Interest Rate Spread Interest Rate 9% 8% 7% 6% 5% 3,4% 4% 3% 2% 1% © RAINER MAURER, Pforzheim 0% Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 10Y Government Bond Interest Rate Germany (left scale) Source: Eurostat, Central Bank of Portugal, Own Calculations Prof. Dr. Rainer Maure Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 Interest Spread compared to Germany (left scale) -6- © www.rainer-maurer.com Die Schuldenkrise der EWU 2010 10% Greece Interest Rate Spread Interest Rate 9% 8% 7% 6,9% 6% 5% 4% 3% 2% © RAINER MAURER, Pforzheim 1% 0% Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 10Y Government Bond Interest Rate Germany (left scale) Source: Eurostat, Own Calculations Prof. Dr. Rainer Maure Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 Interest Spread compared to Germany (left scale) -7- © www.rainer-maurer.com Die Schuldenkrise der EWU 2010 ➤ Was verursachte die Krise? ■ Stark steigende öffentliche und private Schuldenpositionen ....haben Zweifel an der Fähigkeit von Regierungen und Banken, die von diesen Regierungen gestützt werden, aufkommen lassen, die Schulden zurückzuzahlen. ■ Investoren berücksichtigen deshalb die gestiegend Wahrscheinlichkeit eines Ausfalls von Rückzahlungen © RAINER MAURER, Pforzheim .... und fordern deshalb höhere Riskoprämien. Prof. Dr. Rainer Maure -8- Die Schuldenkrise der EWU 2010 10% Interest Rate Spain Interest Rate Spread and Debt-to-GDP Ratios Debt-to-GDP 110% 9% 100% 8% 90% 80% 7% 70% 6% 60% 5% 50% 4% 40% 3% 30% 20% 1% 10% 0% Jan. 99 0% © RAINER MAURER, Pforzheim 2% Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 10Y Government Bond Interest Rate Germany (left scale) Interest Spread compared to Germany (left scale) Total Country Int. Net Debt Position GDP Ratio Total Government Debt GDP-to-Ratio Source: Eurostat, Central Bank of Spain, Own Calculations Prof. Dr. Rainer Maure -9- © www.rainer-maurer.com Die Schuldenkrise der EWU 2010 10% Interest Rate Ireland Interest Rate Spread and Debt-to-GDP Ratios Debt-to-GDP 80% 70% 9% 60% 8% 50% 7% 40% 30% 6% 20% 5% 10% 0% 4% -10% 3% -20% 2% -30% -40% 1% -50% © RAINER MAURER, Pforzheim 0% Jan. 99 -60% Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 10Y Government Bond Interest Rate Germany (left scale) Interest Spread compared to Germany (left scale) Total Country Int. Net Debt Position GDP Ratio Total Government Debt GDP-to-Ratio Prof. Dr. Rainer Maure Source: Eurostat, Own Calculations - 10 - © www.rainer-maurer.com Die Schuldenkrise der EWU 2010 10% Interest Rate Portugal Interest Rate Spread and Debt-to-GDP Ratios Debt-to-GDP 110% 9% 100% 8% 90% 80% 7% 70% 6% 60% 5% 50% 4% 40% 3% 30% 20% 1% 10% 0% Jan. 99 0% © RAINER MAURER, Pforzheim 2% Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 10Y Government Bond Interest Rate Germany (left scale) Interest Spread compared to Germany (left scale) Total Country Int. Net Debt Position GDP Ratio Total Government Debt GDP-to-Ratio Source: Eurostat, Central Bank of Portugal, Own Calculations Prof. Dr. Rainer Maure - 11 - © www.rainer-maurer.com Die Schuldenkrise der EWU 2010 10% Interest Rate Greece Interest Rate Spread and Debt-to-GDP Ratios Debt-to-GDP 130% 120% 9% 110% 8% 100% 7% 90% 6% 80% 70% 5% 60% 4% 50% 3% 40% 30% 2% 20% © RAINER MAURER, Pforzheim 1% 10% 0% 0% Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 10Y Government Bond Interest Rate Germany (left scale) Interest Spread compared to Germany (left scale) Total Country Int. Net Debt Position GDP Ratio Total Government Debt GDP-to-Ratio Prof. Dr. Rainer Maure Source: Eurostat, Own Calculations - 12 - © www.rainer-maurer.com Die Schuldenkrise der EWU 2010 ➤ Die Situation ist noch schlimmer als diese Schaubilder zeigen! ■ Die Veränderung des Gesamtschuldenstandes eines Landes ist der negative Leistungsbilanzüberschuss. ■ Man kann den Leistungsbilanzüberschuss, der notwendig ist, um die aktuelle Schuldenquote konstant zu halten mit folgender Formel berechnen (Herleitung s. Exkurs): Zinssatz Leistungsbilanzüberschuss © RAINER MAURER, Pforzheim EX-IM-i*D B Y i BIP Wachstum Y dY dt Nettoschuldenstand eines Landes D Y BIP Prof. Dr. Rainer Maure - 13 - Die Schuldenkrise der EWU 2010 © RAINER MAURER, Pforzheim ➤ Wendet man diese Formel auf die Daten der Schuldenländer an, zeigt sich, dass ihr aktuelle Leistungsbilanzüberschuss noch weit entfernt ist, von dem Überschuss, der notwendig wäre, um ihre Schuldenstandsquote zu stabilisieren: Prof. Dr. Rainer Maure - 18 - Die Schuldenkrise der EWU 2010 Spain 15% Current Account Surplus Gap Percent of GDP 15% Der Leistungsbilanzüberschuss zur Stabilisierung der Schuldenstandsquote beträgt 7,5% des BIPs. 10% 10% 5% 5% 0% 0% Jan. 99 -5% © RAINER MAURER, Pforzheim -10% -15% Prof. Dr. Rainer Maure Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 -5% Der tatsächliche Leistungsbilanzüberschuss ist: - 5,5% of GDP! -10% => Aktuelle Leistungsbilanzlücke: 13 % des BIPs! -15% Constant Intern. Net Debt-to-GDP Ratio Current Account Surplus (right scale) Actual Current Account Surplus Source: Eurostat, Own Calculations - 19 - © www.rainer-maurer.com Die Schuldenkrise der EWU 2010 Portugal 15% Current Account Surplus Gap Percent of GDP 15% 10% 10% 5% 5% 0% 0% Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 -5% -5% Aktuelle Leistungsbilanzlücke:18,5 % des BIPs! © RAINER MAURER, Pforzheim -10% -10% -15% Prof. Dr. Rainer Maure -15% Constant International Net Debt-to-GDP Ratio Current Account Surplus Actual Current Account Surplus Source: Eurostat, Own Calculations - 20 - © www.rainer-maurer.com Die Schuldenkrise der EWU 2010 Ireland 15% Current Account Surplus Gap Percent of GDP 15% 10% 10% Aktuelle Leistungsbilanzlücke: 15 % des BIPs! 5% 0% Jan. 99 0% Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 -5% -5% © RAINER MAURER, Pforzheim -10% -10% -15% Prof. Dr. Rainer Maure 5% -15% Constant International Net Debt-to-GDP Ratio Current Account Surplus Actual Current Account Surplus Source: Eurostat, Own Calculations - 21 - © www.rainer-maurer.com Die Schuldenkrise der EWU 2010 Greece 15% Current Account Surplus Gap Percent of GDP 15% 10% 10% 5% 5% 0% 0% Jan. 99 Jan. 00 Jan. 01 © RAINER MAURER, Pforzheim -5% Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 Aktuelle Leistungsbilanzlücke: 25 % des BIPs! -5% -10% -10% -15% -15% Prof. Dr. Rainer Maure Constant International Net Debt-to-GDP Ratio Current Account Surplus Actual Current Account Surplus Source: Eurostat, Own Calculations - 22 - © www.rainer-maurer.com Die Schuldenkrise der EWU 2010 Interest Rates (Average: Sept. 2009 - May 2010) and Constant International Debt Position-to-GDP Ratio Primary Current Account Gap (Average: Jan. 2009 - Aug. 2009) 6,0% Nominal Interest Rates 10Y Bonds Correlation Coefficient: 70,1% Greece Je größer die Leistungsbilanzlücke, desto höher die Risikoprämie! 5,5% 5,0% Ireland Cyprus 4,5% Malta © RAINER MAURER, Pforzheim Italy Belgium Luxembourg Austria Finland3,5% Netherlands Portugal Slovakia 4,0% Slovenia Spain United Kingdom France Germany Constant IDP-to-GDP Ratio Current Account Surplus Gap 3,0% -15% -10% Source: Eurostat, Own Calculations Prof. Dr. Rainer Maure -5% 0% 5% 10% 15% - 20% 23 - © www.rainer-maurer.com Die Schuldenkrise der EWU 2010 ➤ Die Lage ist prekär! ➤ Welche Lösungsmöglichkeiten gibt es??? ➤ Ländern wie Griechenland, Spanien, Portugal und Irland müssen ihre "Leistungsbilanzlücke" schließen: B Y Bt Yt it dYt dt Yt Dt Bt Yt Yt © RAINER MAURER, Pforzheim o Prof. Dr. Rainer Maure Depressed - 25 EMU Die Schuldenkrise der EWU 2010 ➤ Welche Lösungsmöglichkeiten gibt es??? ➤ Problem für verschuldete Länder, die Mitgliedsländer einer Währungsunion sind: 1. Sie können keine eigene Währung abwerten, um ihren Leistungsbilanzüberschuss zu verbessern: e$€ ↓ => P€ e$€ ↓ < P$ => ( EX ↑ – IM ↓ ) ↑ © RAINER MAURER, Pforzheim Reduktion der Leistungsbilanzlücke! 2. Sie können keine eigene Währung mit der sie ihre Schulden Prof. Dr. Rainer Maure weg inflationieren können! - 26 - Die Schuldenkrise der EWU 2010 ➤ Welche Lösungsmöglichkeiten gibt es??? ➤ Problem für verschuldete Länder, die Mitgliedsländer einer Währungsunion sind: 3. Bei einem Verlassen der Währungsunion kann die Verschuldung explodieren!!! ◆ Wenn Griechenland die Eurozone verlässt: ...wird die neue Währung (Neodrachme) gegen den Euro abwerten: e€Neodrame ↓ DNeodrame ↓ Prof. Dr. Rainer Maure Die Schuldenlast in Neodramen wird im Gefolge der Abwertung stark ansteigen: = ( D€ / e€Neodrame ↓ ) ↓ © RAINER MAURER, Pforzheim Die Schulden des Landes sind aber in Euro D€ denominiert! - 28 - Die Schuldenkrise der EWU 2010 ➤ Warum ist es soweit gekommen? ■ Die EMU ist eine Währungsunion von Ländern mit sehr unterschiedlichen Konjunkturzyklen: GDP Gaps of ECU Member States and the USA © RAINER MAURER, Pforzheim (Trend Deviation of GDP in Percent of Trend measured by Hodrick-Prescott-Filter) 0,020 0,015 0,010 0,005 2009Q03 2009Q01 2008Q03 2008Q01 2007Q03 2007Q01 2006Q03 2006Q01 2005Q03 2005Q01 2004Q03 2004Q01 2003Q03 2003Q01 2002Q03 2002Q01 -0,005 -0,010 -0,015 GDP Gap = Aktuelles BIP minus Trend-BIP in % des Trend-BIP -0,020 Germany (left scale) USA (left scale) Standard Deviation without Cyprus, Malta, Slovenia, Slovakia, USA (right scale) Source: Eurostat, Own Prof. Dr. Rainer Maure 2001Q03 2001Q01 2000Q03 0,000 2000Q01 8% 7% 6% 5% 4% 3% 2% 1% 0% -1% -2% -3% -4% -5% -6% -7% -8% www.rainer-maurer.com - 29 - Die Schuldenkrise der EWU 2010 ➤ Warum ist es soweit gekommen? ■ Als Folge sind die Inflationsraten in den Mitgliedsländern sehr unterschiedlich: GDP Price Deflator Relative to Germany Indices Relative to Germany (1999 = 100%) 130% 125% 120% 115% 110% Euro area (16 countries) Source: EU Commission, AMECO, Own Calculations Prof. Dr. Rainer Maure Ireland Greece Spain 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 100% 1999 © RAINER MAURER, Pforzheim 105% Portugal www.rainer-maurer.com - 30 - Die Schuldenkrise der EWU 2010 ➤ Warum ist es soweit gekommen? ■ die Europäische Zentralbank hat nur einen Zinssatz (den Hauptrefinanzierungszins) für alle Länder setzen. ■ Deshalb konvergierten nach dem Start der EMU die Nominalzinsen: ■ Konvergierende Nominalzinsen bei unterschiedlichen länderspezifischen Zinssätzen verursachen divergierende Realzinsen! Realzins © RAINER MAURER, Pforzheim r Nominalzin s Inflation i => Länder mit hohen Inflationsraten haben niedrige Realzinsen! Prof. Dr. Rainer Maure Länder mit niedrigen Inflationsraten haben hohe Realzinsen! - 31 - Die Schuldenkrise der EWU 2010 ➤ Warum ist es soweit gekommen? ■ Konvergenz der Nominalzinsen & Divergenz der Realzinsen: Variance Coefficients across the 12 EMU Founding Member States 1,5% 1,3% 1,1% 0,9% 0,7% 0,5% © RAINER MAURER, Pforzheim 0,3% Prof. Dr. Rainer Maure 0,1% Jan. 97 Jan. 98 Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 -0,1% Source: Eurostat, Own Calculations Nominal Interest Rates for 10-Year Government Bonds Inflation Rates (HCPI) Real Interest Rates for 10-Year Government Bonds © www.rainer-maurer.com - 32 - Die Schuldenkrise der EWU 2010 ➤ Warum ist es soweit gekommen? ■ Realzinsen der Krisenländer im Vergleich zu Deutschland: 9,0% Real Interest Rates for 10 Years Government Bonds (based on BIPDeflator) 8,0% 7,0% 6,0% 5,0% 4,0% 3,0% 2,0% 1,0% © RAINER MAURER, Pforzheim 0,0% Jan. 97 Jan. 98 Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 -1,0% -2,0% -3,0% -4,0% Germany Prof. Dr. Rainer Maure Source: Eurostat, Own Calculations Spain Greece Ireland Portugal © www.rainer-maurer.com - 33 - Die Schuldenkrise der EWU 2010 ➤ Warum ist es soweit gekommen? ■ Realzinsen und Verschuldung der EWU-Mitgliedsländer: Bis Dezember 2009 aufgelaufene Nettoauslandsverschuldung in Prozent des BIP und durchschnittlicher Realzins von Januar 1999 bis Dezember 2009 120% Nettoauslandsverschuldung in % des BIP 100% Portugal Spain Greece 80% Ireland 60% 40% Italy © RAINER MAURER, Pforzheim 20% 0% 1,3% France Austria Finland 1,5% -20% 1,7% 1,9% 2,1% 2,3% 2,5% -40% Eurostat, Eigene Berechnungen 2,7% Netherlands Belgium Prof. Dr. Rainer Maure Quelle: Realzins Germany - 34 - Die Schuldenkrise der EWU 2010 ➤ Warum ist es soweit gekommen? ■ Inflationsrate und Verschuldung der EWU-Mitgliedsländer: Bis Dezember 2009 aufgelaufene Nettoauslandsverschuldung in Prozent des BIP und durchschnittliche HVPI Inflationsrate von Januar 1999 bis Dezember 2009 120% Nettoauslandsverschuldung in % des BIP 100% Portugal Spain Greece 80% Ireland 60% 40% Italy © RAINER MAURER, Pforzheim 20% 0% 1,4% France Finland Austria 1,6% 1,8% Inflationsrate 2,0% 2,2% 2,4% 2,6% 2,8% 3,0% 3,2% Netherlands -20% Germany Belgium -40% Prof. Dr. Rainer MaureQuelle: Eurostat, Eigene Berechnungen © www.rainer-maurer.com - 35 - Der EMU Gesamtkapitalmarkt ist im Gleichgewicht, Die in Schuldenkrise EWU 2010 ist! während den Einzelländern der ein Ungleichgewicht ➤ Warum ist es soweit gekommen? ■ Die Hochinflationsländer hatten also immer niedrigere Realzinsen als die Niedriginflationsländer: r r S(Y) S(Y) Überschussangebot rL * r* © RAINER MAURER, Pforzheim Überschussnachfrage Prof. Dr. Rainer Maure rH* Low inflation country: rL*= i*- πL I(Y) S, I I(Y) High inflation country: S, I rH*= i*- πH - 36 - Die Schuldenkrise der EWU 2010 ➤ Warum ist es soweit gekommen? ■ Länder mit hohen Inflationsraten haben deshalb eine ■ Nettoschuldenposition aufgebaut. Länder mit niedrigen Inflationsraten haben deshalb eine Nettovermögensposition aufgebaut. International Net Debt Position of Eurozone Debtor and Creditor Countries 1500 Bn. Euro 1000 500 0 Jan. 98 Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 © RAINER MAURER, Pforzheim -500 -1000 -1500 Sum of Net International Debt Position of Spain, Greece, Ireland, Portugal Sum of Net International Debt Position of Germany, Belgium, Netherlands Prof. Dr. Rainer Maure Source: Eurostat, Own Calculations © www.rainer-maurer.com - 37 - 4.2. Historische Finanzmarktkrisen 4.2.5. Die Schuldenkrise der EWU 2010 ➤ Warum ist es soweit gekommen? Die Schuldenkrise in der EMU ist also kein Zufall! ■ Sie ist das Ergebnis eines Konstruktionsfehlers der EMU! ■ Wie kann die EMU stabiler für die Zukunft gemacht werden? © RAINER MAURER, Pforzheim ■ Prof. Dr. Rainer Maure - 38 -