Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Commodity Forward Curves :

The Old and the New

Helyette Geman

Birkbeck, University of London & ESCP Europe

Member of the Board of the UBS- Bloomberg Commodity Index

To be presented at the Workshop on New Commodity Markets

Oxford Man Institute - June 13 to 15, 2011

Commodities and Shipping

→ They have existed as long as humankind, and will continue to be there for a long

time…

→ In the last 100 years, there have been a number of cycles of boom. The end of the

1970s boom can be identified with the crash in 1980 of precious commodities – and

the failure of the famous Hunt brothers’ squeeze of the silver market. Then

followed nearly 20 years of stagnation in commodity prices.

The 2000s decade started with gigantic rises in all commodity prices (at different

points in time across the years 2001 to 2005), witnessed the effect of the financial

crisis on commodities and a rebound afterwards.

As far as theory is concerned, commodities have been up to the late 1980s

essentially part of economic theory, with no major results coming from finance, and

contributions by economists called Keynes (1936), Kaldor (1939), Working (1949)

The Outlook of Commodity Markets in 2010

→ Increasing wealth invested in commodity indexes (DJ –UBS, GSCI, DB, RICI…)

→ Financial investors were usually positioned on the first nearby as the best to the spot

and avoid the hurdles of physical delivery and warehousing. Given the « noise » on

the first nearby and the frequent contango shape of the forward curve, they now go

to more and more distant maturities – which used to be the domain of action of the

specific industry. Hence, correlations and co- movements of the forward curve need

to be taken into account

→ Banks and private equity are buying physical assets, such as power plants, aluminium

smelters, which give them direct exposure to the spot price – in particular for

hedging activities.

→ At the same time, we witness a flurry of M&As, sometimes hostile, in the mining

industry worlwide, with some major actors being partly or fully state- owned

(Chinalco, Petrobras..)

m

ai

-9

oc 1

m t-91

ar

sao 92

ût

ja 92

nv

-9

ju 3

in

no 93

v9

av 3

r-9

se 4

pt

fé 94

vr

-9

ju 5

ildé 95

cm 95

ai

-9

oc 6

m t-96

ar

sao 97

ût

ja 97

nv

-9

ju 8

in

no 98

v9

av 8

rse 9 9

pt

-9

9

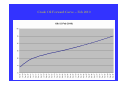

180

160

140

120

100

80

60

GSCI TR

DJ-AIGCITR

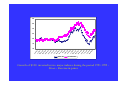

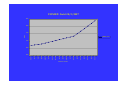

Growth of $100 invested in two major indexes during the period 1991-1999 :

Mean – Reversion in prices

ar

s00

ju

in

-0

se 0

pt

-0

dé 0

cm 00

ar

s01

ju

in

-0

se 1

pt

-0

dé 1

cm 01

ar

s02

ju

in

-0

se 2

pt

-0

dé 2

cm 02

ar

s03

ju

in

-0

se 3

pt

-0

dé 3

cm 03

ar

s04

m

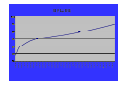

190

170

150

130

110

90

GSCI TR

DJ-AIGCITR

Commodities as a Valuable Asset Class as of 2000

DJ – AIG Petroleum Index Dec 2001 - June 2006

500

450

400

350

300

250

200

150

100

50

1

3

5

7

9

11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57

DJ-AIG Petroleum Sub-index

Is Mean-Reversion Dead ? ( Geman - Sept 2005, J of

Alternative Investments )

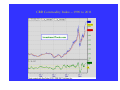

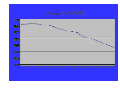

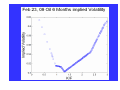

CRB Commodity Index – 1990 to 2011

Commodity Prices: Back to Fundamentals

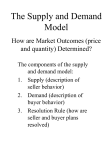

→ The price of a commodity is firstly driven by supply and demand

Quantity

Demand

Supply

Q°

P°

Supply

Demand

Price

Short-term inelastic supply and

demand

→ Another key quantity is the available inventory at the date of analysis, worldwide or

in a given region. This inventory has in impact on prices – hence, is carefully

watched by many CTAs (Commodity Trading Advisers) and on price volatility (see G Nguyen , Management Science, 2005).

→ For exhaustible commodities like crude oil, copper, gold.. reserves are the fourth key

quantity ultimately important

→ In contrast to financial markets, volume risk in commodity markets is as important as

price risk. Commodity markets (electricity, natural gas) have been used to handling

volume risk (Operational research, dynamic programming); financial markets are

used to price risk. The mathematical challenge today is to address both

simultaneously; the financial economics one is the market incompleteness, of various

degrees of profoundity.

Playing the WTI/ Brent spread while being “crude oil price neutral”

Theory of Storage

Keynes (1936), Kaldor (1939), Working (1949), Brennan (1958)

Four fundamentals results:

→ The convenience yield accounts for the benefit that accrues to the holder

of the physical commodity but not to the holder of the futures contract. It

is represented as an implicit dividend

→ The volatility of the commodity spot price is high when inventory is low

→ The volatility of Futures contracts decreases with the maturity:

"Samuelson effect“

→ Moreover, forward curves used to be viewed as being mostly in

backwardation, the so- called “normal backwardation”, due both to the

convenience yield and an assumption of mean- reversion in prices

Spot-Forward Relationship for a Storable Commodity

Under no arbitrage

⎤

⎡

f T (t ) = S(t ) ⎢ 1 + r ( T − t ) + c( T − t ) − y1 ( T − t ) ⎥

123

123

1

424

3 ⎥

⎢

⎣⎢ cos t of financing cos t of storage implicit dividend ⎥⎦

If we define a convenience yield net of cost of storage

f T (t ) = S(t )[1 + (r − y ) ( T − t )]

Or in continuous time, at a fixed date t for a given maturity T

f T (t ) = S(t ) e ( r − y )( T −t )

Correlation Spot- Prompt month (Nordpool):

The standard convenience yield does not apply to electricity

(Eydeland- G, RISK, 1998)

The Forward Curve

→ The set {FT (t) , T > t} is the forward curve prevailing at date t for a given

commodity in a given location

→ It is the fundamental tool when trading commodities, as spot prices may be

unabservable and options not always liquid

→ It allows to identify possible « carry arbitrage » : buy S, sell a future maturity T and

pay the cost of storage and financing as long as the net cashflow is strictly positive

→ The shape of the forward curve is at any date t in a one-to-one mapping with the

convenience yield y

→ It will reflect the seasonality in the case of seasonal commodities such as natural gas or

Agriculturals

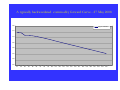

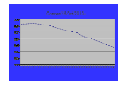

A typically backwardated commodity forward Curve - 27 May 2008

380

Copper COMEX

375

370

365

360

355

350

345

M1

M2

M3

M4

M5

M6

M7

M8

M9

M10

M11

M12

M13

M14

M15

M16

M17

M18

M19

M20

M21

M22

M23

M24

Copper Forward Curve, Oct 2009

Gold as a Numéraire Commodity

→ Historically, gold has been held as an international currency, independent

of individual countries.

→ At various times in history, domestic currencies have been backed by gold:

the “gold standard”

→ The unit of account of the International Monetary Fund (IMF) used to be

denominated in gold; now, a currency basket is used for indexation

→ Over the period following the financial crisis and up to now, gold is viewed

in all nations as a currency of intrinsic value and even as an “asset class”

→ Gold is traded in fine Troy ounces, ounces of actual gold in the ingot (there

are 32.15 Troy ounces in a kilo)

Contract months

déc-11

juin-11

déc-10

juin-10

déc-09

juin-09

déc-08

oct-08

août-08

juin-08

avr-08

févr-08

déc-07

oct-07

août-07

juin-07

mai-07

avr-07

mars-07

Price

COMEX Gold 28/2/2007

850

800

750

COMEX Gold

700

650

600

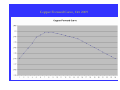

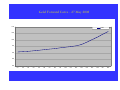

Gold Forward Curve - 27 May 2008

1100

Gold

1050

1000

950

900

850

800

M1

M2

M3

M4

M5

M6

M7

M8

M9

M10

M11

M12

M13

M14

M15

M16

M17

M18

Gold Forward Curve, October 26, 2009

Gold Forward Curve – Feb 2010

Number of Ounces of Gold that can buy the Average US House:

the Role of the Numéraire in the study of Commodities

Forward Curves and Inventories

→ The importance of inventory in explaining spot price volatility has been

widely documented in the economic literature

→ Brennan (1958) and Telser (1958) analyze in the context of several

agricultural commodities the spread between a long-term future and the

prompt month divided by the prompt month

→ They exhibit a negative correlation between this "relative spread" and the

variance of the commodity

→ Fama & French (1987) take as a given the property of the spread being

an adequate proxy for inventory. This allows them to analyze 21

commodities, including metals, for which good inventory data were

missing in their period of analysis

→ Ng & Pirrong (1994) examine four industrial and one precious metals

over the period 1986-1992 and use the same proxy for inventory to

conclude that fundamentals drive metal price dynamics

→ G. & Nguyen (2005) reconstruct a world database of soybean inventory

(with Brazil and Argentina having become more important than the US

in the last few years) and establish a quasi perfect affine relationship

between scarcity defined as inverse inventory and spot price volatility

Inventory and Forward Curve Adjusted Spread in Oil

and Natural Gas Markets

→ As said before, crude oil is not a seasonal commodity, natural gas is a very

seasonal commodity

→ G- Ohana (Energy Economics, 2009) choose the maturity of the “distant”

Future on criteria of liquidity and ability to filter out the seasonality

→ We used a price database consisting of daily NYMEX Futures prices

for the oil from January 1990 to August 2006

for natural gas from January 1993 to August 2006

→ We use for inventory data the EIA website

for crude oil, we collect the volume of all stored petroleum products in

OECD countries at the end of each month from the end of December

1989 to the end of July 2006. This volume is expressed in billion barrels

for oil

for natural gas, the website provides the volume of stored natural gas in

the United States at the end of each month during the period end of

December 1992 - end of July 2006

This inventory is expressed in Trillion cubic feet

0.2

0.0

-0.2

-0.4

gas relative spread

0.4

→ Using detrended inventory, it becomes

Rel-spread = 0.046 – 0.691 Inv

with

Residual standard error = 0.092

R² = 26%

1.5

2.0

deseasonalized gas inventory

2.5

Crude Oil Adjusted Spread vs Detrended Inventory

Crude Oil

Matthew Simmons, Twilight in the Desert

→ "Sooner or later, the worldwide use of oil must peak because oil, like the

other two fossils - coal and natural gas - is non renewable“

→ Over the past 30 years, daily oil consumption has risen by approximately 33

million barrels, Asia accounting for more than half of this growth in demand

→ Current consumption levels suggest that the world's oil supply should last

until around 2045 (without including tar sands)

→ The world's largest producers are Saudi Arabia (13% of world production),

Russia (12%), the United States (7%), Iran (6%) and China (5%)

→ The Gulf of Mexico region provides about 29% of the US oil production,

hence the disruption created by the long shutdown of many oil rigs after

hurricanes Katrina and Rita in summer 2005, and the recent rig accident

10/30/2007

7/10/2007

3/20/2007

11/28/2006

8/8/2006

4/18/2006

12/27/2005

9/6/2005

5/17/2005

1/25/2005

10/5/2004

6/15/2004

2/24/2004

11/4/2003

7/15/2003

3/25/2003

12/3/2002

8/13/2002

4/23/2002

1/1/2002

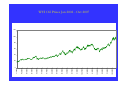

WTI Oil Prices Jan 2002 - Oct 2007

120

100

80

60

40

20

0

c9

av 5

rao 96

ût

-9

dé 6

c9

av 6

rao 97

ût

-9

dé 7

c9

av 7

rao 98

ût

-9

dé 8

c9

av 8

rao 99

ût

-9

dé 9

c9

av 9

rao 00

ût

-0

dé 0

c0

av 0

r

ao -01

ût

-0

dé 1

c0

av 1

r

ao -02

ût

-0

dé 2

c0

av 2

r

ao -03

ût

-0

dé 3

c0

av 3

r

ao -04

ût

-0

dé 4

c0

av 4

r-0

5

dé

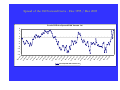

Spread of the Oil Forward Curve - Dec 1995 / Dec 2005

Crude Oil Price Spread 29th Versus 1st

6

4

2

0

-2

-4

-6

-8

-10

-12

-14

Price Spread 29th Versus 1st

ar

s-

06

ju

il0

no 6

vm 06

ar

s07

ju

il0

no 7

vm 07

ar

s08

ju

il0

no 8

v

m -0 8

ar

s09

ju

il0

no 9

vm 09

ar

s10

ju

il1

no 0

vm 10

ar

s11

ju

il1

no 1

vm 11

ar

s12

ju

il1

no 2

vm 12

ar

s13

ju

il1

no 3

vm 13

ar

s14

ju

il14

m

Forward Price

Oil Forward Curve - March 2006 (Bid and Ask)

Forward Curv e

68,37

67,37

66,37

65,37

64,37

63,37

62,37

Maturity

WTI Forward Bid

WTI Forward Offer

Back to Backwardation in September 2007

80

78

76

74

72

70

68

M1

M5

M9

M13

M17

M21

M25

M29

M33

M37

M41

M45

M49

M53

M57

M61

Crude Oil Future curve (17/11/2008)

85

80

75

70

65

60

55

50

M1

M4

M7

M10

M13

M16

M19

M22

M25

M28

M31

M34

M37

M40

M43

M46

M49

M52

M55

M58

M61

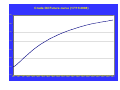

Crude Oil Forward Curve – Feb 2010

References

H.Geman (2010) “Commodities and Numéraire”, Encyclopedia of Quantitative Finance

H. Geman and Yfong Shi (2009) “ The CEV model for Commodity Prices”, Journal of Alternative Investments

H. Geman and S. Kourouvakalis (2008) "A Lattice-Based Method for Pricing Electricity Derivatives under the GemanRoncoroni Model", Applied Mathematical Finance

H. Geman and C. Kharoubi( 2008) “Diversification with Crude Oil Futures : the Time-to- Maturity Effect, Journal of Banking

and Finance

S. Borovkova and H. Geman (2007) "Seasonal and Stochastic Effects in Commodity Forward Curves", Review of Derivatives

Research

H. Geman and A. Roncoroni (2006) "Understanding the Fine Structure of Electricity Prices", Journal of Business

H. Geman (2005) "Energy Commodity Prices: Is Mean Reversion Dead?", Journal of Alternative Investments

H. Geman and S. Ohana (2009) "Inventory, Reserves and Price volatility in Oil and Natural Gas Markets“,Energy Economics

H. Geman (2005) "Commodities and Commodity Prices: Pricing and Modelling for Agriculturals, Metals and Energy", Wiley

Finance

H. Geman and V. Nguyen (2005) "Soybean inventory and forward curves dynamics", Management Science

H.Geman (2004) “Water as the Next Commodity”, Journal of Alternative Investments

H. Geman and M. Yor (1993) "An Exact Valuation for Asian Option", Mathematical Finance

A. Eydeland and H. Geman (1999) "Fundamentals of Electricity options" in Energy Price Modelling, Risk Books

H. Geman and O. Vasicek (2001) "Forwards and Futures on Non Storable Commodities", RISK

H. Geman (2002) "Pure Jump Lévy Processes in Asset Price Modelling", Journal of Banking and Finance

H. Geman (2003) "DCF versus Real Option for Pricing Energy Physical Assets" Conference of the International Energy Agency - Paris

- March 2003

[email protected]