Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

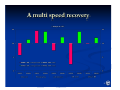

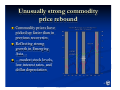

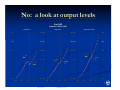

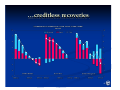

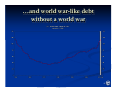

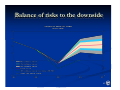

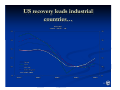

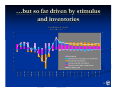

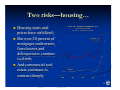

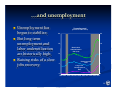

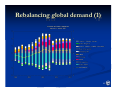

Global Outlook: Blue Skies or Clouds Ahead? By David Robinson IMF Presentation for the event: XXXI Meeting of the Latin American Network of Central Banks and Finance Ministries April 22-23, 2010 Washington, DC © Inter-American Development Bank, www.iadb.org The Inter-American Development Bank Presentations are documents prepared by both Bank and non-Bank personnel as supporting materials for events and are often produced on an expedited publication schedule without formal editing or review. The information and opinions presented in these publications are entirely those of the author(s), and no endorsement by the Inter-American Development Bank, its Board of Executive Directors, or the countries they represent is expressed or implied. This paper may be freely reproduced provided credit is given to the Inter-American Development Bank. Global Outlook: Blue Skies or Clouds Ahead? David Robinson International Monetary Fund April 22nd, 2010 Views expressed are those of the speaker alone and should not be reported as representing the official position of the International Monetary Fund. Outline of Presentation The global outlook—a multi speed recovery, but not business as usual; The United States—a stronger than expected rebound, but weaker than past recoveries; A key challenge: rebalancing demand. 1 Where are we now? WEO Real GDP Growth Projections (percent change from a year earlier) U.S. Euro Japan EMs EAsia LA World 2010 (Current) 2010 (Jan. 10) 3.1 2.7 1.0 1.0 1.9 1.7 6.3 6.0 8.7 8.4 4.0 3.7 4.2 3.9 2011 (Current) 2011 (Jan. 10) 2.6 2.4 1.5 1.6 2.0 2.2 6.4 6.3 8.6 8.4 4.0 3.8 4.3 4.3 Source: IMF, World Economic Outlook. 2 A multi speed recovery 3 Surging capital flows to emerging markets 4 Unusually strong commodity price rebound Commodity prices have picked up faster than in previous recoveries Reflecting strong growth in Emerging Asia… …modest stock levels, low interest rates, and dollar depreciation 5 Growth rates: back to business as usual? 6 No: a look at output levels Real GDP (indexes, 2000 = 100) 7 …creditless recoveries 8 …and world war-like debt without a world war 9 Balance of risks to the downside 10 US recovery leads industrial countries… 11 …but so far driven by stimulus and inventories 12 Two risks—housing… Housing starts and prices have stabilized; But over 20 percent of mortgages underwater, foreclosures and delinquencies continue to climb; And commercial real estate continues to contract sharply 13 …and unemployment Unemployment has begun to stabilize; But long term unemployment and labor underutilization are historically high; Raising risks of a slow jobs recovery. Unemployment (percent of labor force) 20 20 15 15 Broad Labor Underutilization Rate (U-6) 10 5 10 Unemployment Rate 5 Long-Term Unemployment Rate 0 0 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 14 Putting it all together 15 Rebalancing global demand (1) 16 Rebalancing global demand (2) 17 Conclusions Recovery to continue, with emerging markets remaining in the lead; Global rebalancing remains a key challenge: from public to private demand, and from deficit to surplus countries. Credible medium term fiscal strategies are urgently needed in many countries. 18