Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Linear dependence (correlation)

Suppose we observe n pairs of values

{(x1 , y1 ), (x2 , y2 ),K (xn , yn )}

The covariance of x and y is the value

σ xy

1 n

= ∑ ( xi − x )( yi − y )

n i =1

The correlation of x e y is the value

σ xy

ρ xy =

σ xσ y

where σx and σy are the standard deviations of x and y.

Correlation

Takes values in [-1, 1]

Values close to 1 (-1) indicate an almost perfect linear

relation between x and y with positive (negative) slope.

Values close to 0 indicate absence of a linear relation

between the two variables

Warning

Zero correlation does not exclude any form of relation

between x e y, but only absence of linear relation.

Corr(SP100, NASDAQ) = 0.87

Percentage daily returns from 2.1.1998 to 3.6.2011

Quantiles / percentiles

The k-th percentile is the modality that separates the

smallest k% from the greatest (100 - k)%.

Formally, q is the k-th percentile if

# {xi < q}

≤k

n

# {xi > q}

and

≤ (1 − k )

n

The median is the quantile 0.5, or the 50-th percentile.

The quartiles are the quantiles that divide the ordered

data in 4 equal parts: percentiles 25, 50, 75

The deciles are the quantiles that divide the ordered data

in10 equal parts: percentiles 10, 20, …,90

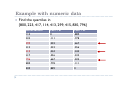

Example with numeric data

Find the quartiles in

{800, 223, 417, 114, 413, 299, 415, 830, 796}

Osservazioni

Perc < xi

Perc > xi

114

0

.889

223

.111

.778

299

.222

.667

413

.333

.556

415

.444

.444

417

.556

.333

796

.667

.222

800

.778

.111

830

.889

0

Elements of probability

Probability space

Ω sample space, set of elementary events. For ex. In a

dice there are 6 elementary elements.

F sigma-filed, subsets of Ω (events) that we are interested

to associate with a probability.

P probability measure, value in [0,1] to be associated to

each event in F.

Sample space

Any non empty set

Examples

Coin toss: H, C

Dice toss: the 6 facets

Throwing a chock against a blackboard: any two dimensional

point on the blackboard

Sigma-field (collection of events)

Set F of subsets of the sample space Ω such that:

The set Ω belongs to F.

If A belongs to F then also his complement with respect

to Ω belongs to F.

If A1, A2, … belong to F then also their union {A1∪A2∪…}

belongs to F.

Consequences: empty set ∅ and intersections of events are

in F.

Try to build example using the sample spaces of the

previous slide.

Probability measure

Set function that maps any element of F to a number in

[0,1] such that:

P(Ω) = 1

If A1, A2,… are disjoint sets (empty intersection), then

P(A1∪A2∪…) = P(A1) + P(A2) + …

There are different approaches to the construction of

probabilities:

Classic

Frequentist

Bayesian

Approaches to probabilities

Classic.

Tied to gambling. The probability of each elementary

event is equal 1/(number of elementary elements)

For ex. each facet of the dice has probability 1/6

Frequentist.

The probability of an event is the relative frequency of

that event as the number of tries goes to infinity.

For ex. I throw a dice n times and check the relative

frequency of each facet as n diverges.

Bayesian.

Subjectivist: it is a probability based on my own opinion

grounded on past experience.

Probability of «A or B»

We’ve seen that if A and B are disjoint the probability

P(A or B) = P(A∪B) = P(A) + P(B)

If A and B intersect the probability of the intersection is

to be subtracted from the total (otherwise counted

twice)

P(A or B) = P(A∪B) = P(A) + P(B) – P(A e B)

Probability of «A or B» and independence

Two events are dependent if there is some connection

btween the two. In this case knowing that A happened

tells us something about the happening of B and viceversa.

For ex. if I know that throwing a dice an even number

was extracted (A), this tell me something about the

extraction of number 3 (B).

The probability that B occurs knowing that A happened, is

termed conditional probability and is indicated with

P(B | A)

P(A e B) = P(A) P(B|A) = P(B) P(A|B)

Independence

Two events A and B are said independent when knowing

that A happened does not give any information on the

occurrence of B, and vice-versa.

For ex. knowing that in throwing a dice “an even number

was extracted” (A) does not provide any information of

the event “the extracted number is in the interval 1-4”

(B).

In this case P(B | A) = P(B) and

P(A and B) = P(A) P(B)

Exercises

Compute the probability that in one dice toss one gets

{1 or 2 or 3}.

A: 1/6 + 1/6 + 1/6 = 1/2

Compute the probability that in one dice toss one gets {1

or 2 or 3} knowing that an even number is extracted.

A: P(1 or 2 or 3 | 2 or 4 or 6) = P(2)/P(2 or 4 or 6) =

(1/6) / (1/2) = 1/3

Compute the probability that tossing two dices the sum

of the results is 3.

A: P({D1=1} and {D2=2}) + P({D1=2} and {D2=1}) =

P{D1=1} P{D2=2} + P{D1=2} P{D2=1} = 2/36

Random variables (r.v.)

Given a probability space (Ω, F, P), a (misurable) function that

associates numbers to events in Ω is called random

variable. If we call ω the generic element of Ω, we can

indicate a r.v. with X(ω), but for brevity usually only X is

used. For ex. for the dice toss:

ω

⚀

⚁

⚂

⚃

⚄

⚅

X(ω

ω)

1

2

3

4

5

6

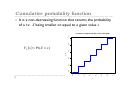

Cumulative probability function

It is a non-decreasing function that returns the probability

of a r.v. X being smaller or equal to a given value x

0.8

1.0

Funzione di ripartizione per il lancio del dado

0.6

FX (x ) = Pr( X ≤ x)

0.0

0.2

0.4

F(x)

0

1

2

3

4

x

5

6

7

Discrete vs. continuous r.v.

When X ranges only in a finite or numerable set of

values, X is discrete.

When X ranges in a set with the power of continuous

(real numbers or intervals), then X is continuous.

There are also «intermediate» situations in which X can

be seen as the sum of a continuous and a discrete r.v. We

will not see any example of this kind in this course.

Probability function

For a discrete r.v. it is possible to define the function p(x)

that map each outcome to its probability.

E.g. for the dice toss we have:

1 6 per x = 1,2,3,4,5,6

p(x ) =

altrementi

0

Off course

F ( x) = ∑ p (i )

i≤ x

Bernoulli r.v.

for x = 0,1

otherwise

1.0

Funzione di probabilità di Bernoulli (p=0.7)

0.8

p x (1 − p )1− x

p(x ) =

0

0.6

with p in [0,1]

0.4

0.2

0.0

Takes only the two values {0,1}

The probability function is

p(x)

0.0

0.2

0.4

0.6

x

0.8

1.0

Binomial r.v.

n!

n− x

p x (1 − p )

p ( x ) = x!(n − x )!

0

for x = 0,1,..., n

otherwise

0.20

Funzione di probabilità binomiale (p=0.7, n=10)

Binomial

probability function with p = .7, n=10

0.10

0.00

Takes the values {1,2,…n}

It is the sum of n independent Bernoulli r.v.

It has two parameters p e n

p(x)

0

2

4

6

x

8

10

Poisson r.v.

Takes the values {1,2,…}

Used for modeling the probability of occurrence of a

number of events in a given time span (e.g. number of

calls in a call-center)

λx exp(− λ )

per x = 0,1,...

(

)

p

x

=

Only one parameter λ > 0

x!

altrimenti

0.10

0.05

0.00

p(x)

0.15

0.20

di probabilità di

Poisson (lambda=3.5)

PoissonFunzione

probability

function

with λ = 3.6

0

0

5

10

x

15

Expectaion

The mean or expectation of a discrete r.v. is

E( X ) = ∑ x ⋅ p(x )

x∈Χ

where Χ represents the range of X, that is the support of

X.

As a consequence the variance is given by

Var ( X ) = ∑ [x − E( X )] ⋅ p( x )

2

x∈Χ

Exercises

Compute mean and variance of Bernoulli, Binomial and

Poisson r.v.

Solutions:

V.C.

E(X)

Var(X)

Bernoulli

p

p(1 – p)

Binomiale

np

np(1 – p)

Poisson

λ

λ

Probability density function

The probability that a continuous random variable hits a

given number is zero and so no probability function can

be defined.

For continuous r.v. one uses the probability density

function f (x): the area underneath the curve over an

interval gives the probability that the r.v. assumes a value

in that interval.

The relation with the cumulative probability function is

F (x ) =

x

∫

−∞

f (z ) d z

d F (x )

f (x ) =

dx

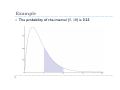

Example

The probability of the interval [5, 10] is 0.25

Mean and variance

Mean

E( X ) =

∞

∫ x ⋅ f (x ) d x

−∞

Variance

var( X ) =

∞

2

(

)

[

x

−

E

X

]

⋅ f (x ) d x

∫

−∞

One notation for the expectation

Note that one can compute the expectation of any

function of the g(X) of a r.v. (if it exists) and the notation

can be made uniform as

E[g ( X )] =

∞

∫ g (x ) d F (x )

−∞

This is a Riemann-Stieltjes integral, but for those who do

not know this definition, they can can just read it as:

∞

continuous r.v. g (x ) ⋅ f (x ) d x

∫

−∞

Discrete r.v.

∑ g (x ) ⋅ p(x )

x∈Χ

Normal or Gaussian r.v.

Density function: it has two paramaters µ e σ.

2

1

1 x−µ

f (x ) =

exp

2π σ

2 σ

Mean = µ

Variance = σ 2

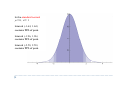

In the standard normal

µ = 0, σ = 1

Interval (-1.64, 1.64)

contains 90% of prob.

Interval (-1.96, 1.96)

contains 95% of prob.

Interval (-2.58, 2.58)

contains 99% of prob.

Note: standardization

Let X be a r.v. with mean µ and standard deviation σ.

Then

X −µ

Y=

σ

is a r.v. with mean 0 and standard deviation 1.

If X is normal, then Y is standard normal.

Chi Square r.v.

It has one param. κ > 0 named degrees of freedom (dof).

Takes only positive values.

Summing the square of k std. normal independent r.v.

gives a Chi Square r.v. with κ = k dof

Mean = κ

Variance = 2κ

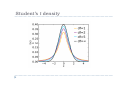

Student’s t r.v.

It has one param. κ > 0 named degrees of freedom (dof).

Takes values in ℝ (real numbers).

If Z is standard normal and S2 is Chi Square with κ dof

independent of Z, then

Z

S2 κ

is Student’s t with κ dof.

For κ →∞ Student’s t converges to a std. normal

Mean = 0

Variance = κ / (κ - 2) if κ > 2, infinite otherwise.

Student’s t density

Moments

The p-th moment of a r.v. is defined as

∞

µ p = E (X p ) = ∫ x p d F ( x )

−∞

The p-th central moment if a r.v. is defined as

[

] ∫ (x − µ )

m p = E ( X − µ1 ) =

p

∞

1

p

d F (x )

−∞

Obviously: µ1 is the mean and e m2 the variance.

Symmetry

A r.v. X is symmetric when for all x

Pr{X − med < x} = 1 − Pr{X − med > x}

where med stands for the median.

In other words we say that a random variable is

symmetric when its density reflects with respect to the

vertical axis centered on the median.

Odd central moments are zero in symmetric

distributions.

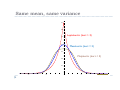

Skewness

It is the standardized third moment

X − µ 3 m3

γ 1 = E

= 3

σ σ

Kurtosis or «tail thickness»

The fourth central std. moment is a measure of «tail

thickness»:

X − µ 4 m4

kurt = E

= 4

σ σ

In normal distr. the kurtosis is 3, and the kurtosis index

(or excess kurtosis):

γ2 =

m4

σ

4

−3

Same mean, same variance

0.7

0.6

0.5

Leptokurtic (kurt > 3)

0.4

Mesokurtic (kurt = 3)

0.3

Platykurtic (kurt < 3)

0.2

0.1

-4

-2

2

4

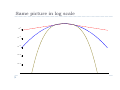

Same picture in log scale

10-5

10-13

10-21

10-29

10-37

-5

0

5

10

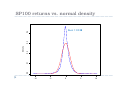

SP100 returns vs. normal density

Densità rendimenti SP100 vs. normale (media = 0.0005, st.dev. = 1.34)

0.2

0.1

0.0

Density

0.3

0.4

Kurt = 10.28

-10

-5

0

5

10