Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

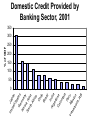

Benchmarking the Development of NBFIs in Latin America Michael Pomerleano The World Bank Regional Seminar on NBFIs in Latin America December 4 – 6, 2002 Santiago, Chile Financial Sector Structure and Conditions • The region suffers from low public and private savings. • Long term financing is lacking, and certain sectors do not have access to finance. • Banking sector lending is low relative to GDP, and concentrated in short-term financing. Credit to the private sector is among the lowest in the world. • Banking sector structure has changed significantly: market share of state banks declined, while foreign banks have increased their presence ( e.g., Mexico). • The region’s securities markets are small and illiquid; both size and volume have mostly shrunk in recent years. • Institutional investors do not play a major role in domestic markets (with the exception of Chilean pension funds and Brazilian mutual funds). Bank and Non-Bank Assets Venezuela Peru Mexico Argentina Ecuador Brazil Bolivia Chile Germany US Japan 0% 10%, 1% 20%, 1% 14%, 9% 24%, 0% 28%, 6% 39%, 6% 50%, 1% 55%, 15% 138%, 6% 73%, 144% 128%, 162% 50% 100% 150% 200% 250% 300% % of GDP Bank AssetsFinancial to GDPAssets, Non-Bank Assets to GDP Source: World Bank, Financial Structure and Economic Development Database, created by Beck, Demirguç-Kunt, and Levine. 350% Ja ni te pan d St a G te s er Ko m a n re a, y So Re ut p. h Af ric a C hi le Br az il I Ar ndi ge a nt C i na ol om bi a Pe r Ve M u n e ex zu ic o el a, R B Source: World Bank, GDF & WDI Central Database U % of GDP Domestic Credit Provided by Banking Sector, 2001 350 300 250 200 150 100 50 0 Domestic Credit to the Private Sector, 2001 % of GDP 200 150 100 50 Ch i le Br az il Ind ia Co l om bia Pe ru Ar ge nti Ve na ne zu el a ,R B Me x ic o Ja pa Un n i te dS tat es Ge rm an Ko y rea ,R ep So . u th Afr ic a 0 Source: World Bank. Domestic credit to private sector refers to financial resources provided to the private sector, such as through loans, purchases of nonequity securities, and trade credits and other accounts receivable, that establish a claim for repayment. For some countries these claims include credit to public enterprises. Br az il Ar ge nti na Me xic o Afr i ca ed St ate s Ve ne zu el a Co lom bi a Ja pa n th Un it Public Sector So u Private Sector Ch ile 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Pe ru % of Domestic Credit Composition of Domestic Credit, 2001 Source: International Financial Statistics (IMF) Note: Other credit includes credit to central and local governments, nonfinancial public enterprises and non-bank financial institutions Un i te dS tat es Ja pa n Ch So i le u th Afr ic a Arg en ti n a Ge rm an Ko y rea ,R ep . Bra z il Ind ia Me x ic o Pe ru Co l om Ve ne zue bia l a, RB % of GDP Market Capitalization Comparison as % of GDP, 2001 140 120 100 80 60 40 20 0 Source: World Bank Market Capitalization, USD Billion, 2001 13,984 3,910 4,000 Billion, USD 3,500 3,000 2,500 2,000 1,500 1,000 500 1,072 232 192 186 127 110 88 57 13 10 6 Ve Pe ne ru zu el a, RB Co lo m bia Ch i le In di So a ut h Af ric a o M ex ic Br az il Ja pa n G er m an Ko y re a, Re p. Ar ge nt in a Un i te d St at es 0 Source: World Bank Note: Market caps. as of beginning of November 2002 are: Argentina- $101 Billion, Brazil- $114 Billion, Mexico- $97 Billion (Source: Bloomberg) 120 100 80 60 40 20 1996 2001 Source: World Bank Ar ge nt in Ve a ne zu el a, R B ol om bi a C Pe ru Br az il C M ex ic o 0 hi le Market Cap., % of GDP Market Capitalization in Latin America, 1996-2001 ni te d Ve hi le ne zu el a C ol om bi Ar a ge nt in a C Pe ru Source: Emerging Markets Database and FIBV (for US). Note: US figure is NYSE 2. 33 3. 17 5. 49 7. 49 7. 86 39 .1 1 37 .3 8 34 .5 31 .5 5 86 .9 120 100 80 60 40 20 0 Br az il M ex ic o St at es R So us s ia ut h Af ric a U Trading, % of market capital Turnover Ratio, 2001 1996 2001 Source: Emerging Markets Database Co lo m bia Ar ge nt in a Ch i le a Ve ne zu el Pe ru M ex ic o 70 60 50 40 30 20 10 0 Br az il Turnover, % Turnover Ratio in Latin America, 1996-2001 Market Concentration, 2001 Source: FIBV Total Number of New Firms Listed, Sample Stock Exchanges, 1996-2001 140 120 100 80 60 40 20 0 117 113 110 62 61 32 1996 1997 1998 1999 2000 2001 Source: FIBV Note: Sample includes exchanges of Mexico, Buenos Aires, Lima, Santiago, Sao Paulo, Bogota and Caracas. Gross New Capital Raised by Domestic Companies, Average, 1997-2001 5.0% 4.0% % of 3.0% market 2.0% cap. 1.0% Already listed UK Ar ge nti na US Ch ile Pe ru Br az il 0.0% Newly admitted Source: FIBV Note: US figure is for NYSE. Figures for newly admitted companies unavailable for Argentina. Return on a US dollar basis over the fiveyear period ended December 31, 2001. Argentina Brazil Chile Colombia Mexico Peru Venezuela Source: Wilshire Associates -5.30% -1.10% -2.90% -8.80% 11.70% -4.80% -7.10% Return/Risk Ratio, 1997-2001 bia ru Pe ue la Co lom Source: Wilshire Associates Ve ne z na Ar ge nti Ch ile il az Br Me xic o 0.4 0.3 0.2 0.1 0 -0.1 -0.2 -0.3 Note: Risk is measured by standard deviation of return on a US dollar basis over the period. Transaction Costs Argentina Capital Gains Tax 0% Dividend Tax 0% Stamp Duty 0% Other Charges Brazil 0% 0% 0% 0.2% tax on cash in/out of country* Chile 10%-42% 10%-42% 0% 3% central bank tax (buyer); 18% VAT; 0.44% exchange tax Colombia 0% 0% 1% 16% VAT on FX purchases (Seller) México 0% 0% 0% 20% withholding on off-exchange trades Peru 0% 0% 0% 0.18% stock exchange; levy Venezuela 1% VAT 0% 0% 0.75% FX tax (buyer); 1% government tax (seller) 0.24% exchange levy; 0.005% year end tax Source: Brinson Partners, Inc. * Transactions in the stock exchange have recently been exempted for all investors Settlement Proficiency Trading technology Days to settle trades (T+_) DvP method Scri-less settlement Argentina Partially automated 3 Yes Yes Brazil Partially automated 3 Yes Yes Chile Partially automated 2 Yes, for shares. For OTC, fixed income & money market transactions at the exchanges funds are not Central Bank funds, so transfers are not final. Yes Source: International Securities Services Association, Wilshire Associates Settlement Proficiency- continued Trading Technology Days to Settle Trades (T+_) Colombia Partially automated México Fully automated 2 Peru Partially automated 2 (buyer); 3 (seller) Venezuela Fully automated 3 to 6 0 to 90 DvP Scrip-less Settlement Only at DCV, the central depository for government securities. Yes Yes No, equities are held in physical form and immobilized, and represented by book entry. Yes Yes No No - share certificates are never printed, however a transfer slip is necessary. Source: International Securities Services Association, Wilshire Associates Ratings for Settlement Wilshire Score for Settlement Proficiency, end 2001 (Best: 3) GSCS Settlement Index Score (Q1-02) (Best: 100) Argentina 2 89.54 Brazil 2 85.81 Chile 2 NA Colombia 1 NA Korea 3 98.50 Malaysia 2 94.14 México 3 89.96 Peru 2 93.08 Venezuela 1 64.81 Source: GSCS Benchmarks provides the international securities industry with measures of operational performance in over 20 major markets, 20 emerging markets see www.gscsbenchmarks.com/ Stock Markets • Local stock markets are “hallowing” due to migration to global financial markets, resulting in lower capitalization and volume. • Primary issuance has decreased in Argentina, Brazil, Chile and Mexico between 1996-2001. • In 2000, the market capitalization of Latin America’s stock exchanges represented only 32 percent of GDP, compared with 114 percent in Southeast Asia, 115 percent in Europe, and 164 percent in the U.S.* • Market liquidity is also low: 33 percent in LAC, compared with 105 percent in Europe, 106 percent in the U.S., and 133 percent in Southeast Asia*. • Markets have suffered from volatile capital flows, transaction taxes, and a lack of transparency and protection of minority shareholders’ rights. • In a majority of countries (especially less developed ones) family based ownership predominates, and in some cases is growing. * Source: The McKinsey Quarterly, 2001(4) Source: Merrill Lynch, IMF Ve ne zue la o Me x ic Ch i le Bra z External debt Domestic debt Co l om bia Arg en ti n a 80% 70% 60% 50% 40% 30% 20% 10% 0% il % of GDP Tradable Debt in Latin America, end 2001 Composition of Outstanding Domestic Securities, September 2001 % of domestic securities 100% 80% 60% 40% 20% Corporate securities Source: BIS Ch i le Fra nce Ja pa n Me x ic o Bra z il Arg en ti n a US Pe ru UK 0% Government securities Bond Markets • Some countries (Mexico, Brazil, Chile, Argentina and Colombia) have made considerable progress in developing bond markets while others are in pre-developmental stages. • Developmental differences are attributable to diversity in the size of regional economies. • In some countries, governments have been able to extend bond maturities and issue fixed rate instruments, however inflation indexed bonds are still common (e.g., Brazil). • The more developed markets are using primary dealers and many countries have regular issuance calendars. • The majority of Latin American countries still require (directly or indirectly) that banking reserves be met exclusively by government securities. Additionally, countries like Colombia, Costa Rica, Jamaica and others rely heavily on public sector investments in government securities. • Bond markets are currently faced with a serious threat following Argentina’s default, and the risks confronting Brazilian government bonds. Assets of Open-end Mutual Funds, 2001 35% 30% 20% 15% 10% 5% Source: Investment Company Institute , IMF a Ar ge nt in o ex ic M le Ch i Ja pa n an y G er m UK l 0% Br az i % of GDP 25% Br az il C hi le M ex ic o Bo l iv ia Ar ge nt in a U ru gu ay Pe ru C ol um Ve bi ne a zu el a Mutual Fund Assets, 1998 20 15 10 5 0 % of GDP Source: OECD Mutual Funds • Brazil’s mutual fund industry is the most developed in the region (emerged from the high-inflation period of the late 80’s and offered inflation-indexed accounts). • Around 90% of assets are in fixed income instruments; composition of portfolios by asset classes similar across the region. • Most mutual funds in the region are owned and administered by private banks, and there is a high degree of functional and administrative integration between the institutions. • Most Latin American countries separate mutual funds oriented to domestic investors from those oriented towards foreign investors. • The mutual fund industry is less concentrated than the pension fund and insurance industries. • Commission level are comparable with those for mutual funds in OECD countries. Life any Source: Swiss Re, World Bank 16 14 12 10 8 6 4 2 0 Peru Mexi co uel a Vene z Braz il Arge ntina Colo mbi a Non-life Jama ica Chile Germ US UK Premiums, % of GDP Insurance Penetration, 2000 Insurance Industry • Latin America is a small and yet promising insurance market. • LAC premium volume in 2000 was 1.6% of all premiums worldwide, while GDP was 6% of the global product. • Over 90% of premium income comes from Argentina, Brazil, Chile, Colombia, Mexico and Venezuela. • Penetration is lower than in other emerging markets, however on a per capita basis the people of the region spend more than those in ECA, Africa or emerging Asia. • Since 1990, the insurance markets have been liberalized, and foreign insurers play an important role in all major markets. • Life insurance premiums have grown at double digit rates (except for Brazil and Venezuela, where social insurance schemes are state-run) from 1995-2000, as a result of reforms in pensions’ systems in the region. • Non-life insurance has enjoyed high growth rates between 1995-2000, rising in line with GDP. • In many markets, new distribution channels designed to reach the lower-and middle-income target group are being tried. Pension Fund Assets, 2000 Source: IADB Pension Funds • In 8 countries (starting with Chile in 1981), PAYG systems have been replaced, to varying degrees, by fully funded defined contribution systems, with individual pension accounts managed by pension fund administrators. • Another 5 countries, including Brazil, are in the process of considering pension reform. • Ownership of administrators usually in the hands of large banks and financial conglomerates; Foreign participation is extensive. • Brazil, Chile account for approximately 80% of regional pension assets. • Investment is concentrated in domestic markets, which are at a low level of development. • Investment regulation are rigid and inflexible, thus increasing costs. • Historical pension fund real returns have been high, yet difficult to assess future performance. Volatile returns reduced by international instruments. • Pension fund coverage low. • Operational costs decreased in reformed systems, yet are still high. In part attributable to an incentive structure that encourages marketing (has increased costs) and leads to a high switching rate. Recent Developments in Corporate Governance • Mexico- in June 2001 a new Capital Markets Law came into effect; – It grants explicit authority to the CNBV to regulate tender offers in order to prevent minority shareholder exclusion; – The law restricts the issuance of non-common shares to 25%, requires independent members on the board and allows minority shareholders to appoint board members; – The law turns insider trading and market manipulation into criminal offenses punishable with incarceration. • Argentina- A capital markets reform law passed in June 2001; – It imposes mandatory tender offers for control once 35% has been acquired; – Minority shareholders were given a ‘fair price’ protection for their holdings; – Public companies are required to create audit committees; – Shareholders’ access to information and participation in shareholder meetings have been eased. Recent Developments in Corporate Governance- cont. • Brazil- in October 2001 the new Corporate Law was passed; – It strengthens the protection of minority shareholders by providing more power to the CVM, – adding 80% tag-along rights for common shareholders, – Board of directors representation for all shareholders, – improved voting conditions and more. – In 2001 BOVESPA launched the Novo Mercado, which aspires to int’l corporate governance standards. Companies listed there are prohibited from issuing non-voting shares, have to abide by US or int’l accounting standards, and have a minimum 25% free float. Only 4 listings.