Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

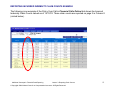

Additional Concepts in Financial Data Reporting (Module #2) Lesson 3: Reporting Claim Counts Additional Concepts in Financial Data Reporting Lesson 3: Reporting Claim Counts © Copyright 2004 National Council on Compensation Insurance. All Rights Reserved. 1 Lesson 3: Objectives • Understand the importance of reporting counts accurately • Define Closed Indemnity Claim Counts, and know the specific Financial Calls on which they are reported • Define Open Indemnity Claim Counts, and know the specific Financial Calls on which they are reported • Define Incurred Indemnity Claim Counts, and know the specific Financial Calls on which they are reported • Know how to identify Closed Indemnity Claim Counts, Open Indemnity Claim Counts, and Incurred Indemnity Claim Counts in Financial Calls Online • Become familiar with the most common claim count reporting issues Additional Concepts in Financial Data Reporting Lesson 3: Reporting Claim Counts © Copyright 2004 National Council on Compensation Insurance. All Rights Reserved. 2 CLAIM COUNTS OVERVIEW Financial data claim counts refer to the number of indemnity claims an insurance company is responsible for paying on behalf of the insured for a specified period—whether they are already settled or still open. Financial data claim counts apply only to indemnity claims, which are losses that involve lost wages due to an injured worker sustaining a work-related injury. Insured claims that only have medical benefits (medical-only claims) are not included in claim counts for Financial Calls. Claim count information reported on Financial Calls is necessary for NCCI to determine the frequency, severity, and claim count development, which are used in trend factor analysis. These analyses uncover changing patterns that are not apparent in loss ratio trends. Timely information on emerging trends is critical for developing accurate loss costs and rates, as well as for providing key information for reform legislation. The status of a claim can be either “Open” or “Closed.” This lesson covers the specifics of claim count reporting for closed claims, open claims, and incurred (open and closed) claims. Additional Concepts in Financial Data Reporting Lesson 3: Reporting Claim Counts © Copyright 2004 National Council on Compensation Insurance. All Rights Reserved. 3 CLOSED INDEMNITY CLAIM COUNTS OVERVIEW Closed Indemnity Claim Counts are the number of claims that are paid in full and do not contain outstanding case reserves and/or Defense and Cost Containment Expenses (DCCE) claim reserves. Closed Claim Counts are reported in Column 19 (entitled Accumulated Closed [Paid]) of the following four Financial Calls: Call Number 3 3A 5 5A Call Name Policy Year Policy Year — Assigned Risk Calendar-Accident Year Calendar-Accident Year — Assigned Risk Additional Concepts in Financial Data Reporting Lesson 3: Reporting Claim Counts © Copyright 2004 National Council on Compensation Insurance. All Rights Reserved. 4 REPORTING CLOSED INDEMNITY CLAIM COUNTS General rules for reporting Closed (Paid) Indemnity Claim Counts are as follows: • This count includes those indemnity claims that are paid in full with no existing outstanding loss and/or Defense and Cost Containment Expense (DCCE) claim reserves • • Claims that started out as medical-only claims but were resolved as indemnity claims at a future valuation should be added to closed claims • Additional Concepts in Financial Data Reporting Lesson 3: Reporting Claim Counts © Copyright 2004 National Council on Compensation Insurance. All Rights Reserved. 5 REPORTING CLOSED INDEMNITY CLAIM COUNTS EXAMPLE The following is an example of the Policy Year Call in Financial Calls Online that shows the Closed (Paid) Indemnity Claim Counts valued as of 12/31/03. These claim counts are reported in Column 19 (circled below), which is displayed on page 4. Additional Concepts in Financial Data Reporting Lesson 3: Reporting Claim Counts © Copyright 2004 National Council on Compensation Insurance. All Rights Reserved. 6 OPEN INDEMNITY CLAIM COUNTS OVERVIEW Open Indemnity Claim Counts are the number of claims that are not paid in full and have outstanding case reserves and/or Defense and Cost Containments Expenses (DCCE) reserves. Open Claim Counts are reported in Column 20 (Open [Outstanding]) of the following Financial Calls, which are the same four Calls that require Closed Indemnity Claim Counts: Call Number 3 3A 5 5A Call Name Policy Year Policy Year — Assigned Risk Policy Year Calendar-Accident Year Calendar-Accident Year — Assigned Risk Additional Concepts in Financial Data Reporting Lesson 3: Reporting Claim Counts © Copyright 2004 National Council on Compensation Insurance. All Rights Reserved. 7 REPORTING OPEN INDEMNITY CLAIM COUNTS General rules for reporting Open (Outstanding) Indemnity Claim Counts are as follows: • This count includes those indemnity claims for which outstanding case and/or Defense and Cost Containment Expense (DCCE) reserves exist at year-end, regardless of whether or not any payments have been made on those claims • Indemnity claims that were closed at the previous valuation but were reopened and remain open as of this valuation date should be added open claims Additional Concepts in Financial Data Reporting Lesson 3: Reporting Claim Counts © Copyright 2004 National Council on Compensation Insurance. All Rights Reserved. 8 REPORTING OPEN INDEMNITY CLAIM COUNTS EXAMPLE The following is an example of a Policy Year Call in Financial Calls Online that shows the Open (Outstanding) Indemnity Claim Counts valued as of 12/31/03. These claim counts are reported in Column 20 (circled below), which is displayed on page 4. Additional Concepts in Financial Data Reporting Lesson 3: Reporting Claim Counts © Copyright 2004 National Council on Compensation Insurance. All Rights Reserved. 9 INCURRED INDEMNITY CLAIM COUNTS OVERVIEW Incurred Indemnity Claim Counts are the accumulated number of claims for which indemnity payments have been made and/or an outstanding loss or Defense and Cost Containment Expenses (DCCE) reserve exists. The Incurred Claim Counts are reported in Column 8 (Incurred Indemnity Claim Count). Incurred Indemnity Claim Counts are reported on the following seven Financial Calls (three additional calls other than those that require Closed and Open Indemnity Claim Counts): Call Number 3 3A 5 Call Name Policy Year Policy Year — Assigned Risk Calendar-Accident Year 5A Calendar-Accident Year — Assigned Risk 11 Policy Year F-Classification 20 Policy Year Large Deductible 21 Calendar-Accident Year Large Deductible Additional Concepts in Financial Data Reporting Lesson 3: Reporting Claim Counts © Copyright 2004 National Council on Compensation Insurance. All Rights Reserved. 10 REPORTING INCURRED INDEMNITY CLAIM COUNTS Incurred indemnity claim count is the accumulated number of claims for which an indemnity payment has been made and/or an outstanding indemnity loss reserve exists. Insured claims that only have medical benefits (medical-only claims) are not included in claim counts for Financial Calls. The incurred indemnity claim count excludes those claims that start out with an indemnity reserve but were subsequently resolved as medical-only claims, Defense and Cost Containment Expense-only claims, or claims closed without payment. • If in a previous Call valuation, claims were originally thought to include indemnity losses, but at a subsequent Call valuation do not include indemnity benefits, the indemnity claim count should be reduced for these claims in the subsequent Call valuation. The incurred indemnity claim count includes claims that start out as medical-only but were resolved as indemnity at future valuations. • If a medical-only claim develops indemnity, the incurred indemnity claim count should be increased in the Call valuation year where the indemnity losses were first determined to exist. • If indemnity claims that closed with payment are reopened, they should not be added to the incurred indemnity claim count. • If claims closed without payment are reopened as indemnity claims, they should be added to the incurred indemnity claim count. Additional Concepts in Financial Data Reporting Lesson 3: Reporting Claim Counts © Copyright 2004 National Council on Compensation Insurance. All Rights Reserved. 11 REPORTING INCURRED INDEMNITY CLAIM COUNTS EXAMPLE The following is an example of the Policy Year Call in Financial Calls Online that shows the Incurred Indemnity Claim Counts valued as of 12/31/03. These claim counts are reported on page 2 in Column 8 (circled below). Additional Concepts in Financial Data Reporting Lesson 3: Reporting Claim Counts © Copyright 2004 National Council on Compensation Insurance. All Rights Reserved. 12 COMMON CLAIM COUNT REPORTING ISSUES It is important to be aware of the most common claim count related reporting issues in order to help maintain quality data for NCCI’s products and services. Carefully check your data to prevent the following errors from being reported: • Column 8—A common reporting issue is when the Incurred Indemnity Claim Count includes medicalonly claims or claims closed with no payments. Reminder: Claim counts only include indemnity claims (with work-related injuries and benefits). Medical-only claims (with only medical benefits) are not included in claim counts for Financial Calls. • Columns 19 and 20—A common reporting issue is when a data provider applies a different definition for an open claim than NCCI’s definition of an open claim. Reminder: NCCI defines an indemnity claim as open if it has outstanding case and/or DCCE reserves, regardless of whether or not any payments have been made on the claim. Column 20 should include only open claims as defined by NCCI, and Column 19 should include the claims that were closed. Additional Concepts in Financial Data Reporting Lesson 3: Reporting Claim Counts © Copyright 2004 National Council on Compensation Insurance. All Rights Reserved. 13 COMMON CLAIM COUNT REPORTING ISSUES (Continued) • Columns 8, 19, and 20—A common reporting issue is when the closed claim totals plus the open claim totals do not equal the incurred claim totals. The correct data equation is as follows for Calls 3, 3A, 5, and 5A: = Totals in Column 19 Totals in Column 20 + (closed claims) (open claims) • Total Claim in Column 8 (incurred claims) TPA and MGA procedures—A common reporting issue for insurance carriers that use a Third Party Administrator (TPA) or Managing General Agent (MGA) to manage their claims is when the TPA/MGA does not report the claim details to the insurance carrier in a timely manner. This sometimes causes claim counts reported to NCCI to be inaccurate. Reminder: When using a TPA or MGA to manage claims, it is important that the carrier’s processes and procedures ensure that the TPA/MGA provides the carrier with the claim information in a timely and accurate manner so it can be reported to NCCI in compliance with the financial data reporting rules. Additional Concepts in Financial Data Reporting Lesson 3: Reporting Claim Counts © Copyright 2004 National Council on Compensation Insurance. All Rights Reserved. 14