Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

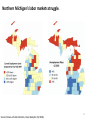

Economic Update Chicago Region 2016 Banker Workshop Series Rob Vilim Senior Financial Analyst, Chicago Region Division of Insurance and Research Federal Deposit Insurance Corporation The views expressed are those of the presenter and do not necessarily reflect official positions of the Federal Deposit Insurance Corporation. Some of the information used in the preparation of this presentation was obtained from publicly available sources that are considered reliable. However, the use of this information does not constitute an endorsement of its accuracy by the Federal Deposit Insurance Corporation. 1 Moderate GDP growth is expected to continue, despite recent weakness. GDP beats expectations in Q3. • Real GDP increased at an annual rate of 2.9% in third quarter 2016 • Blue Chip consensus forecast for the same period was 2.7% • Post-recession GDP growth averaged 2.1% compared with 3.0% average annual growth between 1980 and 2007 Personal consumption expenditures should continue to support growth. • Inventories’ contribution to GDP increase was substantial from negative in Q2 to 0.61 Q3 • Residential fixed investment should return to being a positive contributor – had been a positive contributor for 9 quarters • Private fixed investment in equipment may be a persistent drag • Exports’ contribution may be temporary according to analysts 2 Volatility in the global economy is supporting a strong dollar, putting pressure on U.S. exports and manufacturing activity. As the world’s safe haven currency, the dollar strengthened again on the Brexit vote. • The strength of the U.S. dollar puts pressure on exports • Commodity producers and export-oriented manufacturers suffer • IHS/Markit forecasts the dollar peaking in 4Q2016 Manufacturing production measures flirt with contraction. • Manufacturing production was unchanged in September compared to a year ago • The ISM index slipped recently, but remains in expansion territory • The strong dollar and reduced energy exploration activity will weigh on US exports 3 Labor markets are also slowly improving. Both headline and broader measures of unemployment are improving. • The U.S. added 156,000 jobs in September after very strong growth in the summer • The pace of job growth has slowed, averaging 181,500 in 2016, compared with average monthly gains of 229,000 in 2015 • The U-6 unemployment rate, at 9.7% in third quarter 2016, remains above pre-recession levels of 8.4% Declining labor force participation aids falling unemployment rates, but the participation rate has been falling for some time. • The participation rate peaked in 2000 • The rate of decline accelerated during the recession, but may have stabilized • As the U.S. adds jobs, the employment to population ratio is increasing – indicating improving labor market fundamentals 4 Income growth remains weak, indicating potential ongoing slack in the labor market; inflation remains below FOMC targets. Compared to pre-recession, income growth has been moderate. • Personal income grew 5.2% on average prerecession, compared with 3.6% postrecession • Average hourly earnings increased 2.6% from Q3 2015 to Q3 2016 • Personal income increased 3.2% during the same time period Both the total and core personal consumption expenditure deflator measures remain below the FOMC target of 2%. • Falling energy prices caused inflation measures to decline, but measures recently increased • In August, core PCE (less food & energy) increased 1.7% year over year • In August, total PCE increased 0.9% year over year 5 Global forecasts expect weak growth in most developed countries. Blue Chip International Concensus Forecasts Real GDP Inflation (% Change) Interest Rates 2015 2016(F) 2017(F) 2015 2016(F) 2017(F) 2016(F) 2017(F) United States 2.6 1.5 2.2 0.1 1.2 2.3 0.32 0.81 Canada 1.1 1.2 2.0 1.1 1.6 2.0 0.75 1.01 Mexico 2.5 2.2 2.4 2.7 2.9 3.3 4.38 5.08 Japan 0.6 0.6 0.8 0.7 -0.2 0.4 -0.05 -0.02 South Korea 2.6 2.7 2.6 0.7 0.9 1.5 1.32 1.34 United Kingdom 2.2 1.8 0.6 0.0 0.7 2.1 0.34 0.38 Germany 1.5 1.7 1.4 0.1 0.4 1.4 -0.26 -0.14 France 1.2 1.3 1.1 0.1 0.3 1.2 -0.26 -0.14 Euro Zone 1.6 1.6 1.4 0.0 0.2 1.2 -0.26 -0.14 Brazil -3.8 -3.3 0.9 9.0 8.6 5.7 13.91 11.60 Russia -3.7 -0.7 1.1 15.5 7.2 5.3 10.34 8.04 China 6.9 6.6 6.2 1.4 2.0 2.0 2.83 2.86 India 7.6 7.5 7.6 4.9 5.3 5.3 6.81 6.66 • U.S. growth is projected to be stronger than most of our largest trading partners in 2017 • U.S. inflation expectations are subdued • Chinese growth is expected to continue on its path of moderation • Russia and Brazil are expected to exit recession in 2017 Source: Blue Chip Economic Indicators, Oct. 10, 2016. 6 Michigan Conditions Contributors Drag • Labor Markets • Manufacturing (long term) • Housing Markets • Demographics • Manufacturing (last 6 yrs.) • Municipal Fiscal Issues • Energy markets (recently) 7 Michigan’s demographics pose long-term economic risk. Michigan had negative population growth from 2005-2015. • Michigan’s current population is 1.3% below its pre-recession peak • Michigan has experienced slow growth for decades, growing only 7% since 1990. The national average was 29% for the same time period • Michigan and Rhode Island were the only states to see population loss from 2005-2015 Michigan also has a relatively high median population age. • With a median age of 39.7, Michigan has one of the oldest populations in the Region and the county • The US median age is 37.7, two years younger than Michigan’s • Many of Michigan’s youth have migrated south or to neighboring states such as Illinois and Indiana 8 Michigan job growth tops Region growth, picks up pace from last year. Michigan's job growth picks up pace. • Michigan added over 84,900 jobs during the year ending September 2016, a 2% increase • During the prior year period, Michigan added more than 59,300 jobs, a 1.4% increase • Despite above average job growth, Michigan has yet to reach pre-recession employment levels. Michigan has regained 86% of jobs lost during the recession, the only state in the Region below 100%. Michigan’s unemployment rate ticked down in Q3 2016. • At 4.5%, Michigan's unemployment rate is below the national and regional average • The unemployment rate has risen in the US as job seekers reenter the labor force faster than the economy adds jobs • Michigan’s low unemployment rate may be due to a smaller labor force caused by discouraged workers or net-out-migration 9 Strong job growth across many sectors. Michigan’s job growth has been broad based. • The professional and business services sector; and Finance, Insurance, and Real Estate led job growth. • Declining commodity prices are affecting mining employment Nationally, automotive sales and employment may have plateaued. • Automotive manufacturing jobs nationally increased as vehicle sales rose, but jobs and sales appear to have plateaued. 10 Auto manufacturing has yet to fully recover despite increased output. Michigan’s auto manufacturing employment is far from pre-recession levels. • Michigan’s automotive manufacturing employment underperforms compared to Regional post-recession job growth • In 2015, Michigan’s automotive manufacturing employment was 28% below 2005 level Despite sluggish employment recovery, auto production increases nationally. • Auto manufacturing has increased without commensurate growth in auto manufacturing employment • Production has rebounded quicker than auto employment, suggesting an increase in the sector’s efficiency 11 Northern Michigan’s labor markets struggle. Source: Bureau of Labor Statistics, Haver Analytics (Q2 2016). 12 Housing market fundamentals have improved markedly. Michigan's housing market continues to improve. • Michigan’s home prices increased 5.3% over the last year, compared to national growth of 5.6% • As of second quarter 2016, Michigan’s home prices were 2.9% below the 2005 peak. Illinois is the only other state in the Region that has yet to reach the pre-recession peak Other housing market fundamentals are showing significant improvement. • Michigan’s foreclosure inventories have fallen; the percent of loans in foreclosure fell from 4.6% at peak to just 0.7% currently • Michigan’s foreclosure starts are below prerecession levels at 0.8% compared with a recession peak of 1.7% • Past due mortgages are also below prerecession levels and were 4.7% in June, compared with a pre-recession peak of 7.6% 13 State Fiscal Situation Michigan’s debt per capita is below the national and regional average. • Lower debt per capita reduces long term fiscal risks. • In the Region, only Indiana has a lower debt per capita Unfunded Pension liabilities. • Michigan has amassed a much smaller unfunded pension liability than the two worst states in the Region, Kentucky and Illinois. • Michigan’s unfunded pension liabilities are, however, above the US average and far from the Region’s best preforming state, Wisconsin 14 Local fiscal distress persists in many communities. Municipalities and School Districts in Financial Emergency Municipalities Allen Park Detroit Ecorse Flint Hamtramck Lincoln Park Pontiac Royal Oak Township School Districts Benton Harbor Area Schools Detroit Public Schools Highland Park School District Pontiac Public Schools Muskegon Heights School District Status Receivership-Transition Advisory Board Financial Review Commission Receivership-Transition Advisory Board Receivership-Transition Advisory Board Receivership-Transition Advisory Board Receivership-Transition Advisory Board Receivership-Transition Advisory Board Consent Agreement Status Consent Agreement Emergency Manager Emergency Manager Consent Agreement Emergency Manager Michigan has many distressed municipalities and school districts. • The vast majority of municipalities and school districts in financial emergency are located within the Detroit Metropolitan Area Source: State of Michigan, Emergency Financial Manager/Emergency Manager Appointment History. Contacts Eric Robbins, Regional Manager, DIR Chicago [email protected] 312-382-7545 Rob Vilim, Senior Financial Analyst, DIR Chicago [email protected] 312-382-6547 Miguel Hasty, Senior Financial Analyst, DIR Chicago [email protected] 312-382-7581 Stefan Spong, Economic Analyst, DIR Chicago [email protected] 312-382-7582 Tyler Hienkel, Economic Assistant, DIR Chicago [email protected] 312-382-6808 16