Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

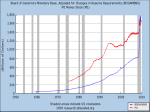

US Fed: the water rate addendum 23 September 2014 Economics US Fed: the water rate addendum DBS Group Research 23 September 2014 • Three QE programs have made the Fed funds rate obsolete as a policy rate • Banks are sitting on $2800bn of excess reserves that they are free to deploy – or add to – any day they wish • The only way to control whether banks move funds into or out of this reserve poos is to raise or lower the rate paid on them – the water rate • The official name for the water rate is “interest rate paid on excess reserves”. Either way, it’s the new policy rate • Congress may not like paying banks for ‘doing nothing’ but they got paid even more when they held Treasuries instead of Fed deposits In “US Fed: the water rate” (16Sep) we discussed why the Fed funds rate has become irrelevant as a policy tool and will likely be replaced by the “interest rate on excess reserves” or what we call the water rate, for short. The repo/reverse repo rate(s) will support the new policy rate as it supported Fed funds in the past. The message there was that Fed funds had been made obsolete by the failure of QE to “inject liquidity” into the economy as was hoped and as traditionally occurs when the central bank conducts open market operations / buys bonds. For the most part, Fed ‘injections’ continue to sit idle on bank balance sheets in the form of excess reserves. The magnitude of these reserves ($2800bn at last count) and the fact that banks are free to tap them – or add to them – any day they wish, means that the rate paid on excess reserves is the only one that matters when it comes to monetary stimulus / constraint. US Fed – balance sheet (liability side) QE3 Sep12 - Oct14 US$bn 4,500 All those QE ‘injections’ went nowhere but into the Fed’s basement in the form of excess reserves 4,000 QE1 Dec08-Mar10 3,500 QE2 Nov10-Jun11 3,000 2,500 Excess bank reserves at the Fed 2,000 1,500 Deposits and capital 1,000 Currency in circulation 500 0 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 David Carbon • (65) 6878-9548 • [email protected] 1 US Fed: the water rate addendum More formally That the Fed ‘injected’ $3.5 trillion into the economy through its QE programs is one of the most enduring conventional wisdoms of the past five years. But it is a myth: nothing was injected into the economy, the stock market, foreign emerging markets or anywhere else. In “The water rate” we explained why this is so using simple language and a simple model where the Fed purchased its bonds solely from banks. While many appreciate the simplicity, some have asked for a more precise / technical treatment that, additionally, includes QE purchases from the public rather than banks alone. This addendum attempts to address these issues. Explicit balance sheet examples are offered and asset / bond purchases are extended to individuals. None of the conclusions about injections and/or the need for a new policy rate are altered. However, in the initial paper we hypothesized that Congress might become upset with a new policy rate that pays interest on excess reserves and rewards banks for ‘doing nothing’. On further reflection, discussed below, it is clear these payments are simply received in lieu of what would have been earned on their Treasury holdings had they not been sold to the Fed. Whether Congress recognizes this fact or not remains to be seen. Monetary injections – the good old days The best place to start with ‘liquidity injections’ is how they used to work. Called ‘open market operations’, the central bank would buy a bond and the effects would ripple through the economy in circular fashion until the money supply had grown by perhaps 10x and loans had grown by 9x. This ‘money multiplier’ was the essence of the fractional reserve system and explains why any banking system today is, to a greater or lesser extent, a ‘house of cards’. 23 September 2014 Table 1: Typical money / loan expansion in fractional reserve banking system Step 0: starting point Bank A Assets Reserves Required Excess Loans 10 10 0 100 Deposits 100 Capital 10 Total 110 Total 110 Step 1: Fed buys $50UST from client who holds acct at Bank A Bank A Assets Bank A now has $45 of excess reserves which it is free to loan out. Since excess reserves pay almost no interest and the economy is doing well, the bank lends out the entire $45 of excess reserves. This is shown in Step 2. On the asset side, bank loans rise by $45. On the liability side, deposits also rise by $45. This reflects the fact that the borrower dispenses his loan as intended and whoever receives those funds deposits them with their bank. Although Bank A thought it had loaned out all its excess reserves, the new deposits mean it once again has surplus reserves that may be lent out. Loans are once again extended. Deposits are once again received. With a 10% required reserve ratio, this process continues until deposits expand Liabilities Reserves Required Excess Loans 60 15 45 100 Deposits 150 Capital 10 Total 160 Total 160 Step 2: Bank lends out excess reserves Bank A Assets Liabilities Reserves Required Excess Loans 60 19.5 40.5 145 Deposits 195 Capital 10 Total 205 Total 205 The process is illustrated in Table 1. Bank A represents the banking system overall and its initial balance sheet is shown in Step 0. On the liability side, the bank has $100 of deposits and $10 of capital. On the asset side, it holds $10 of required reserves and $100 of loans. The reserve requirement is assumed to be 10% of deposits. Total assets equal total liabilities. In Step 1, the Fed purchases a $50 Treasury bond from a private citizen who we’ll call Bob. It pays for the bond by crediting the reserves of Bank A by $50. Bank A credits Bob’s deposits by the same amount. Liabilities Steps 3, 4 etc etc… Final equilibrium: excess reserves are exhausted by lending Bank A Assets Liabilities Reserves Required Excess Loans 60 60 0 550 Deposits 600 Capital 10 Total 610 Total 610 Total change due to $50 Fed UST purchase Bank A Assets Liabilities Reserves Required Excess Loans +50 +50 0 +450 Deposits Total +500 Total Capital +500 0 +500 2 US Fed: the water rate addendum 23 September 2014 by 10x and loans expand by 9x the initial bond purchase. In this example, a $50 bond purchase by the central bank has led to a $450 increase in loans and $500 increase in deposits. Total reserves have risen by $50. Excess reserves have returned to zero. Everything that can be lent out has been lent out. Failure to launch 1.0 One may note that in the ‘successful’ loan creation example above, the central bank did not have to purchase the $50 bond from the bank in order for bank reserves to rise. Although the bond was purchased from a private citizen, banks’ reserves still grew by $50 and loans grew by 9 times that. In a similar manner, as we’ll see below, it will make no difference whom the bond is purchased from when loan creation fails – when banks do not lend out their excess reserves. In this ‘failure’ scenario, consider first a Fed bond purchase from a bank. Changes in the balance sheet are clear and make it easy to assess other scenarios. Initially, Bank A holds assets and liabilities of $110. The liability side is the same as before. On the asset side, it holds $10 of reserves, as required. Other assets include $50 each of loans and Treasuries. The Fed then purchases $50 of Treasury bonds from Bank A, paying for them with $50 of reserves. Reserves rise by $50. Securities holdings fall by $50. Assets and liabilities remain unchanged at $110. Importantly, Bank A extends no new loans. In this example, the Fed ‘injected’ $50 of reserves into Bank A. Bank A ‘injected’ them back into the Fed in the form of excess reserves. All that has occurred is an asset swap: the public now holds reserves at the Fed instead of Treasuries. If those Treasuries had been 3-month T-bills, then one shortterm government liability would simply have been swapped for another. Few would expect this to have any impact on the economy. The Fed of course has aimed to purchase longer-term Treasuries from the public. Although there is still no net ‘injection’ into the economy, the hope is that longerterm interest rates would fall modestly and this would have a stimulative impact. The extent of that impact remains subject to debate. The liquidity ‘injected into the economy’ is not subject to debate: it is zero. Table 2: Fed buys $50 UST from bank banks fail to lend excess reserves Starting point Bank A Assets Liabilities Reserves Required Excess Loans Securities 10 10 0 50 50 Deposits 100 Capital 10 Total 110 Total 110 Fed buys $50UST from bank Bank A Assets Liabilities Reserves Required Excess Loans Securities 60 10 50 50 0 Deposits 100 Capital 10 Total 110 Total 110 Total changes due to Fed purchase Bank A Assets Reserves Required Excess Loans Securities Total Liabilities +50 0 +50 0 -50 0 Deposits 0 Capital 0 Total 0 Failure to launch 1.1 Put Bob back into the calculus above and nothing material changes. The Fed now buys $50 of UST from Bob. The Fed credits Bank A with $50 of reserves and the bank credits Bob’s deposit account for $50. Assets and liabilities of Bank A rise by $50. Again though, for one reason or another, the bank refuses to lend out its excess reserves, holding them instead with the Fed. Loans remain unchanged. Once again there has been no net injection of liquidity into the economy. An asset swap has taken place as before, except now it has occurred between the Fed and Bob, rather than between the Fed and Bank A. As before, the public now holds $50 of deposits at the Fed, earning 25 basis points per year. The Fed now owns a $50 government security, earning whatever it earns. Out of these earnings, the Fed pays Bank A 25 basis points per year for its reserves held there. Bank A passes this to Bob, less its usual fees. Bank in the middle Some general principles should be clear. Through its QE/Open market operations, the central bank determines the quantity of total reserves in the banking system. Reserves are created irrespective of whether the central bank purchases a bond from a bank or a private citizen. Banks and banks alone, however, determine how many of those reserves sit idle at the Fed [1]. If banks do not lend the excess reserves that the Fed creates for them, there is no net injection of liquidity into the system. 3 US Fed: the water rate addendum 23 September 2014 Again, this is irrespective of whether a bank or private citizen sold the bond to the Fed. The bottom line is clear: the Fed lays out the water bowl, the banks decide whether and how much to drink from it. The water rate The easiest way to control whether banks move funds into or out of this reserve pool is to raise or lower the rate paid on them – the water rate Since December 2008, banks’ excess reserves have grown to $2800bn from zero. As in the examples above, banks are free to lend them out any day they wish. They are also free to do the opposite – to add to them if they thought that would be profitable. The easiest way to control whether banks move funds into or out of this reserve pool is to raise or lower the rate paid on them – the water rate [2]. For example, if the Fed felt they were lending too freely into economy, it could raise the water rate. This would ripple across the rest of the economy because banks are free to sell their existing assets – like government securities or, indeed, loans to businesses – and deposit the payments as excess reserves at the Fed. The reverse would also apply. Thus, the broader constellation of interest rates prevailing in the economy could be raised or lowered by altering the water rate. Exit Fed funds Why can’t Fed funds serve this purpose any more? Two main reasons: First, because the Fed funds rate is a market rate and there is no market any more. Fed funds is the rate at which banks lend to one another when they have too many or too few reserves at the Fed at the end of the day. No one has too few any more. Everyone has too many. The only way for the Fed to balance supply and demand would be to effect quantitative changes in bank reserves – to alter / unwind its three QE programs. The water rate – the rate paid on excess reserves – is not a market rate; it is dictated autonomously by the Fed. That’s a technical consideration, if an important one. The bigger reason why Fed funds won’t do the trick any more is simply the bigger numbers involved – a $2800bn pool of reserves is difficult to control indirectly. Why fool around with indirect controls anyway? If this giant pool of excess reserves is what matters to the economy – and in terms of monetary policy, it is – then it only makes sense to control the pool directly. Hence the water rate becomes the new policy rate. Congress and subsidies In our 16Sep note, we hypothesized that politicians might become upset with paying banks 2% or 3% per year on $2800bn of reserves sitting risk-free in the Fed’s basement. At a 3% interest rate, this would amount to the Fed paying banks $84bn each and every year for ‘doing nothing’. While Congress may still get upset, the balance sheet examples above make it clear that such emotions would be unwarranted. QE amounts to an asset swap – the Fed receives a Treasury and a bank (or private citizen) receives a deposit at the Fed. The Fed pays the bank with the earnings from its Treasury bond. The bank (or private citizen) receives only what he/she would have received before the bond was swapped. Probably a bit less in fact. There’s no free lunch, apparently, even when it comes to the QE ‘printing press’. Which is why QE hasn’t kicked up growth or inflation in the five years that the program has been in place. Notes [1] Plainly, loan demand / the strength of the economy is important too. [2] The other way of course would be for the Fed to conduct open market operations / buy and sell bonds / unwind its QE programs. This will no doubt be part of a longer-term monetary policy / strategy. But for shorter-term policy, controlling the interest rate would be far simpler and smoother. 4 US Fed: the water rate addendum 23 September 2014 Sources: Data for all charts and tables are from CEIC Data, Bloomberg and DBS Group Research (forecasts and transformations). 5 US Fed: the water rate addendum 23 September 2014 GDP & inflation forecasts GDP growth, % YoY CPI inflation, % YoY 2011 2012 2013 2014f 2015f 2011 2012 2013 2014f 2015f US Japan Eurozone 1.6 -0.5 1.6 2.3 1.4 -0.7 2.2 1.5 -0.4 2.1 1.2 0.6 2.6 1.0 0.9 3.1 -0.3 2.7 2.1 0.0 2.5 1.5 0.4 1.3 1.7 2.9 0.5 1.9 1.5 0.8 Indonesia Malaysia Philippines Singapore Thailand Vietnam 6.5 5.1 3.6 6.0 0.1 5.9 6.2 5.6 6.8 1.9 6.4 5.0 5.8 4.7 7.2 3.9 2.9 5.4 5.4 5.9 6.4 3.0 1.6 5.4 5.9 5.2 6.4 3.6 4.0 5.7 5.3 3.2 4.7 5.2 3.8 18.6 4.0 1.7 3.2 4.6 3.0 9.3 6.4 2.1 2.9 2.4 2.2 6.6 6.0 3.0 4.4 1.5 2.1 4.8 5.8 3.2 4.1 2.8 3.3 5.8 China Hong Kong Taiwan Korea 9.3 4.9 4.2 3.7 7.7 1.5 1.5 2.3 7.7 2.9 2.1 3.0 7.5 2.6 3.5 3.5 7.5 3.0 3.7 3.8 5.4 5.3 1.4 4.0 2.6 4.1 1.9 2.2 2.6 4.3 0.8 1.3 2.7 4.4 1.4 1.5 3.2 4.0 1.3 2.5 India* 6.7 4.5 4.7 6.1 6.6 9.0 7.4 9.5 8.1 7.0 * India data & forecasts refer to fiscal years beginning April; prior to 2013. Source: CEIC and DBS Research Policy & exchange rate forecasts Policy interest rates, eop Exchange rates, eop current 4Q14 1Q15 2Q15 3Q15 current 4Q14 1Q15 2Q15 3Q15 US Japan Eurozone 0.25 0.10 0.05 0.25 0.10 0.05 0.25 0.10 0.05 0.25 0.10 0.05 0.25 0.10 0.05 … 108.8 1.285 … 105 1.28 … 106 1.27 … 108 1.26 … 109 1.25 Indonesia Malaysia Philippines Singapore Thailand Vietnam^ 7.50 3.25 4.00 n.a. 2.00 6.50 7.50 3.25 4.00 n.a. 2.00 6.50 7.50 3.50 4.00 n.a. 2.00 6.50 7.50 3.50 4.00 n.a. 2.00 6.50 7.50 3.50 4.25 n.a. 2.25 6.50 11,989 3.25 44.5 1.27 32.2 21,205 11,750 3.20 43.3 1.26 32.3 21,200 11,750 3.18 43.1 1.25 32.1 21,200 11,750 3.17 42.9 1.24 32.0 21,200 11,750 3.16 42.7 1.23 31.9 21,200 China* Hong Kong Taiwan Korea 6.00 n.a. 1.88 2.25 6.00 n.a. 1.88 2.25 6.00 n.a. 2.00 2.25 6.00 n.a. 2.13 2.50 6.00 n.a. 2.25 2.75 6.14 7.75 30.2 1039 6.10 7.76 29.6 1025 6.07 7.76 29.5 1020 6.04 7.76 29.4 1015 6.01 7.76 29.3 1010 India 8.00 8.00 8.00 8.00 8.00 60.9 61.3 61.6 61.9 62.3 ^ prime rate; * 1-yr lending rate Market prices Policy rate Current (%) US Japan Eurozone 10Y bond yield Current 1wk chg (%) (bps) FX Current 1wk chg (%) Index Equities Current 1wk chg (%) 0.25 0.10 0.05 2.56 0.54 1.01 -3 -4 -6 84.7 108.8 1.285 0.5 -1.5 -0.9 S&P 500 Topix Eurostoxx 1,994 1,331 3,096 0.5 1.3 0.9 Indonesia Malaysia Philippines Singapore Thailand 7.50 3.25 4.00 Ccy policy 2.00 8.22 3.94 4.38 2.50 3.67 -8 -5 -2 -5 0 11977 3.25 44.5 1.267 32.2 -0.1 -0.6 -0.6 -0.6 -0.1 JCI KLCI PCI FSSTI SET 5,220 1,846 7,280 3,297 1,590 1.5 -0.5 1.1 -0.5 0.7 China Hong Kong Taiwan Korea 6.00 Ccy policy 1.88 2.25 … 2.28 1.73 2.99 … 22 -2 -5 6.14 7.75 30.2 1039 0.0 0.0 -0.5 -0.1 S'hai Comp HSI TWSE Kospi 2,290 23,955 9,135 2,039 -2.1 -1.6 -0.9 0.2 8.46 -4 60.9 0.4 Sensex 27,207 1.5 India Source: Bloomberg 8.00 6 US Fed: the water rate addendum 23 September 2014 Recent Research US: the water rate addendum 23 Sep 14 SG: On liquidity and property 30 May 14 IN: Forging global ties 19 Sep 14 TH: more downgrades 23 May 14 US Fed: the water rate 16 Sep 14 SG: SGD – unappreciated 22 May 14 Qtrly Economics-Markets-Strategy 4Q14 11 Sep 14 India elections: Quick review 16 May 14 IN: Market too dovish 25 Aug 14 IN: Four key post-election priorities 9 May 14 KR: Housing recovery 21 Aug 14 Asia: Gamechangers 5 May 14 IN: Increasing resilience 20 Aug 14 CN: Consumption opportunities in the rebalancing process 28 Apr 14 SG: Competitiveness matters 23 Apr 14 EZ: Time to bite the QE bullet? 22 Apr 14 ID: The to-do list 21 Apr 14 TW-CN services trade: 4 questions 17 Apr 14 CNH: “Through-train” coming 15 Apr 14 Asia cyclical dashboard: praise Europe! 11 Apr 14 IN: Assessing the El Nino threat 11 Apr 14 US: Unfrozen, just 10 Apr 14 ID: Beyond 2014 8 Aug 14 CN: SOE reform challenges 6 Aug 14 Asia cyclical dashboard: EU disappoints 25 Jul 14 US: The inflation non-problem 23 Jul 14 SG: Downgraded 23 Jul 14 KR: Unleashing services 17 Jul 14 US: The search for a new policy rate 14 Jul 14 India Budget: hits and misses 11 Jul 14 UST: 10Y yields downside limited 8 Jul 14 3 Jul 14 CN: Defaults, liberalization and new market benchmarks 8 Apr 14 India budget: setting its sights longer ID: Fiscal prudence still warranted 2 Jul 14 KR: Decoding ‘474’ 1 Apr 14 JP: Abe’s reform plan, V2.0 MY: Foot on the brake Qtrly: Economics-Markets-Strategy 3Q14 27 Jun 14 PH: Bond yields to continue north 31 Mar 14 27 June 14 IN: Election is about the economy, not just markets 28 Mar 14 ID: Consumption doubts unfounded 27 Mar 14 CNH: Fructifying trade finance activities 25 Mar 14 KR: Rate hikes not priced in 17 Mar 14 Qtrly: Economics-Markets-Strategy 2Q14 13 Mar 14 12 Jun 14 CNH: Offshore loans set to grow 4 Jun 14 JP: Looking beyond the volatility 30 May 14 CN: In search of a new consensus 30 May 14 Disclaimer: The information herein is published by DBS Bank Ltd (the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. 7