Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

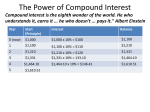

Chapter 1: Lesson 2 Activity TEACHER’S MATERIAL Interesting Interest 1/4 ACTIVITY MATERIALS Individual Activity handout; calculator 15 MINUTES OBJECTIVE Students will compare the growth of money invested with simple interest to the growth of money invested with compound interest STANDARDS Spending and Saving Standard 1: Develop a plan for spending and saving. • Explain why saving is a prerequisite to investing. Investing Standard 1: Explain how investing may build wealth and help meet financial goals. • Given a rate of return and number or years, calculate the future value of a lump-sum investment. PROCEDURE 1. Distribute the activity handout and point out the simple interest and compound interest information. 2. Instruct students to follow the directions and complete the activity. SIMPLE INTEREST Simple interest is a quick way to compute interest on a principal investment—the total amount of money invested. This is the mathematical formula to figure simple interest: I = prt I is simple interest, p is the principal amount, r is the interest rate, and t is the number of years. So, simple interest is calculated by multiplying the principal by the interest rate by the total number of years. This formula provides the interest earned over the number of years input into the formula. You would then add that figure to the initial principal amount. Foundations in Personal Finance: Middle School Edition Chapter 1 Chapter 1: Lesson 2 Activity TEACHER’S MATERIAL Interesting Interest 2/4 For example, a $100 principal investment at a simple annual interest rate of 10% would earn $10 per year. Over five years, your investment would look like this: $100 to start $110 after one year $120 after two years $130 after three years $140 after four years $150 after five years If you kept this going, how much would you have after: Six years? $ 160 Seven years? $ 170 Eight years? $ 180 Nine years? $ 190 Ten years? $ 200 COMPOUND INTEREST Compound interest is a mathematical explosion that can help you make a lot of money. Each year, the compounded interest impacts the total amount in the investment—both the principal and the interest each year. That’s great news because you are also earning interest on your interest! This is the mathematical formula for compound interest: FV = PV(1+r/m)mt FV is the future value with compound interest, PV is the present value based on the principal amount, r is the interest rate expressed as a decimal, m is the number of times per year the interest is compounded (monthly, annually, etc.), and t is the number of years/ periods you leave the money invested. This formula provides the actual future value. Foundations in Personal Finance: Middle School Edition Chapter 1 Chapter 1: Lesson 2 Activity TEACHER’S MATERIAL Interesting Interest 3/4 Using the same $100 principal investment and the same 10% interest rate as the simple interest example, watch how monthly compounded interest impacts your investment: $100 to start $110 after one year $122 after two years $135 after three years $149 after four years $165 after five years For this example, you are trying to determine Future Value (FV). PV = $100 (the initial investment) r = .10 (10% interest) m = 12 (monthly compounding) t = this will change to compute each year So, the equation will look like this for the first five years: $110 after one year: FV = 100(1+.10/12)12×1 $122 after two years: FV = 100(1+.10/12)12×2 $135 after three years: FV = 100(1+.10/12)12×3 $149 after four years: FV = 100(1+.10/12)12×4 $164 after five years: FV = 100(1+.10/12)12×5 This is best worked with a scientific calculator which allows you to input the correct formula. Notes The figure in the parentheses will remain the same (1+.10/12); for simplicity, you can use the following figure: 1.008333. The exponential number (mt) will need to be calculated separately and then inserted into the equation. For the first five years, the numbers will be 12, 24, 36, 48, 60; then for years 6–10, the numbers will be 72, 84, 96, 108, 120. The equation for year five looks like this FV=100(1.008333)60 and can be simplified as 1.00833360 × 100. Foundations in Personal Finance: Middle School Edition Chapter 1 Chapter 1: Lesson 2 Activity TEACHER’S MATERIAL Interesting Interest 4/4 If you kept this going, how much would you have after: Six years? $ 182 Seven years? $ 201 Eight years? $ 222 Nine years? $ 245 Ten years? $ 271 Do you see how that works? So, after five years, you would have an additional $14 with compound interest instead of simple interest. Now, an extra $14 may not seem like a big deal. But if you go out twenty years, it would be $300 with simple interest but $732 with compound interest. Pretty impressive, right? And it looks even better if you start with $1,000 or more. Try it out and see. Foundations in Personal Finance: Middle School Edition Chapter 1 Student Name: Date: Chapter 1: Lesson 2 Activity Interesting Interest 1/3 SIMPLE INTEREST Simple interest is a quick way to compute interest on a principal investment—the total amount of money invested. This is the mathematical formula to figure simple interest: I = prt I is simple interest, p is the principal amount, r is the interest rate, and t is the number of years. So, simple interest is calculated by multiplying the principal by the interest rate by the total number of years. This formula provides the interest earned over the number of years input into the formula. You would then add that figure to the initial principal amount. For example, a $100 principal investment at a simple annual interest rate of 10% would earn $10 per year. Over five years, your investment would look like this: $100 to start $110 after one year $120 after two years $130 after three years $140 after four years $150 after five years If you kept this going, how much would you have after: Six years? $ Seven years? $ Eight years? $ Nine years? $ Ten years? $ Foundations in Personal Finance: Middle School Edition Chapter 1 Chapter 1: Lesson 2 Activity Interesting Interest 2/3 COMPOUND INTEREST Compound interest is a mathematical explosion that can help you make a lot of money. Each year, the compounded interest impacts the total amount in the investment—both the principal and the interest each year. That’s great news because you are also earning interest on your interest! This is the mathematical formula for compound interest: FV = PV(1+r/m)mt FV is the future value with compound interest, PV is the present value based on the principal amount, r is the interest rate expressed as a decimal, m is the number of times per year the interest is compounded (monthly, annually, etc.), and t is the number of years/ periods you leave the money invested. This formula provides the actual future value. Using the same $100 principal investment and the same 10% interest rate as the simple interest example, watch how monthly compounded interest impacts your investment: $100 to start $110 after one year $122 after two years $135 after three years $149 after four years $165 after five years For this example, you are trying to determine Future Value (FV). PV = $100 (the initial investment) r = .10 (10% interest) m = 12 (monthly compounding) t = this will change to compute each year So, the equation will look like this for the first five years: $110 after one year: FV = 100(1+.10/12)12×1 $122 after two years: FV = 100(1+.10/12)12×2 $135 after three years: FV = 100(1+.10/12)12×3 $149 after four years: FV = 100(1+.10/12)12×4 $164 after five years: FV = 100(1+.10/12)12×5 This is best worked with a scientific calculator which allows you to input the correct formula. Foundations in Personal Finance: Middle School Edition Chapter 1 Chapter 1: Lesson 2 Activity Interesting Interest 3/3 Notes The figure in the parentheses will remain the same (1+.10/12); for simplicity, you can use the following figure: 1.008333. The exponential number (mt) will need to be calculated separately and then inserted into the equation. For the first five years, the numbers will be 12, 24, 36, 48, 60; then for years 6–10, the numbers will be 72, 84, 96, 108, 120. The equation for year five looks like this FV = 100(1.008333)60 and can be simplified as 1.00833360 × 100. If you kept this going, how much would you have after: Six years? $ Seven years? $ Eight years? $ Nine years? $ Ten years? $ Do you see how that works? So, after five years, you would have an additional $14 with compound interest instead of simple interest. Now, an extra $14 may not seem like a big deal. But if you go out twenty years, it would be $300 with simple interest but $732 with compound interest. Pretty impressive, right? And it looks even better if you start with $1,000 or more. Try it out and see. Foundations in Personal Finance: Middle School Edition Chapter 1