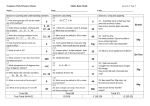

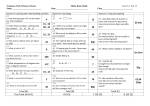

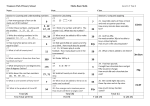

Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Commodity Money Inflation: Theory and Evidence from France in 1350-1436 Nathan Sussman The Hebrew University of Jerusalem Joseph Zeira The Hebrew University of Jerusalem and CEPR August 2000 Abstract This paper presents a theory of inflation in an economy with commodity money and supports it by evidence from the inflationary episodes in France during the fourteenth and fifteenth centuries. The paper shows that commodity money can be inflated similarly to fiat money through repeated debasements, which act like devaluation. Furthermore, as with fiat money, demand for commodity money falls with inflation. Unlike fiat money, at high rates of inflation the demand for commodity money becomes insensitive to inflation, since commodity money has intrinsic value in addition to transactions, and thus losses from inflation are bounded. Finally, we show that an anticipated stabilization reduces the demand for commodity money, which is opposite to the effect of an anticipated standard stabilization on the demand for fiat money. All the results of the model are supported by the data. JEL Classification: E31, N13 Keywords: Inflation, commodity money, debasements, seignorage, stabilization. Mailing Address: Nathan Sussman Department of Economics Hebrew University of Jerusalem Mt. Scopus Jerusalem 91905 Israel E-mail: [email protected] Commodity Money Inflation: Theory and Evidence from France in 1350-1436 1. Introduction This paper describes and analyzes inflation in an economy with commodity money, and compares it with fiat money inflation. The results are derived from a simple model of commodity money and are supported by historical data on money and prices in Medieval France, in the years 1350-1436. We show that there is much similarity between inflation of commodity money and that of fiat money. First, commodity money can be inflated by debasing the currency and inflation can be quite high. Second, the demand for commodity money falls as inflation rises. We also find two dissimilarities between the two types of money. The first is that due to the intrinsic value of commodity money, its inflationary losses are bounded. As a result, when the rate inflation is high, the demand for money becomes insensitive to inflation. The second dissimilarity is that under commodity money the demand for money falls with anticipation for stabilization, while it increases under fiat money. The paper first shows how repeated debasements lead to inflation, which can be rather high. In each new debasement the ruler issues a new coin with a lower content of the precious commodity, which is silver in our historical example. The new coin enters into circulation, the quantity of money increases and prices rise. The ruler gains from such debasement since he collects seignorage from coins minted and reminted. The main intuition behind this result is that the units of commodity money are coins and not silver, and coins can have different contents of silver and thus different values. We therefore assume that coins circulate by tale rather than by 1 weight. This assumption is supported by our data from France in 1350-1436. The data show that debasements were frequent and substantial, that rates of inflation were quite high and sometimes even very high, and that the volumes of minting and reminting and of seignorage during debasements were substantial.1 The paper then analyzes the demand for commodity money. Inflation erodes the value of money and operates as a tax on money holdings. Hence, if the public expects higher inflation the demand for money is reduced. But losses to holders of commodity money are bounded when inflation is high. This is due to the alternative use of commodity money, which can be used to create new coins by reminting, and even be converted, although at some cost, to silver. As a result, the demand for commodity money in high inflation becomes insensitive to the rate of inflation. Although we do not have observations on the demand for money in medieval France, we do have data on minting volumes by the royal mints. The model enables us to relate the demand for money to the volume of minting, in various stages of the inflationary process. This enables us to perform empirical tests of the prediction of the model. Our empirical analysis indeed shows that the negative effect of the rate of inflation on the demand for money is strong at low rates of inflation and much weaker at high rates of inflation. Next we discuss the effect of an anticipated stabilization. A standard stabilization of fiat money inflation consists mainly of stopping monetary expansion. Hence, anticipating such stabilization reduces future expected costs of holding money and therefore increases the demand for money. Under commodity money stabilization requires issuing new coins with higher content of silver, since the process of inflation 1 Rolnick, Velde and Weber (1996) question this assumption and claim that coins did not circulate by tale. We discuss this issue extensively in the paper. 2 has previously reduced the silver content of older coins by too much. During the historical period we examine, many inflationary episodes ended with stabilizations and always the silver content of coins increased at stabilization. Hence, in stabilization old coins become either completely useless or go through silver extraction, which is a very costly activity. Hence, stabilization is costly for money holders, and anticipation of such stabilization reduces the demand for money rather than increases it. This result is also supported by the data from French mints. We find that the demand for money decreased prior to major anticipated stabilizations. We estimate the probability of stabilization under rational learning and show that this probability had a negative effect on the demand for money. It is important to note that this finding is related not only to our theory of inflation, but is also evidence for rational learning by the public on the probability of stabilization, which is an interesting result in itself. This paper extends the existing literature on commodity money and connects it to the mainstream literature on money and inflation. Recent important contributions to the theory of commodity money are Li (1995), Sargent and Smith (1997), and Velde, Weber and Wright (1997). These papers analyze the theory of commodity money, of the types of coins in circulation and of debasements. Our paper offers three important additions to this literature. First, it extends the analysis to a situation of repeated debasements, namely of inflation, which to our best knowledge has never been done before. Second, it turns from issues such as Gresham’s Law to the more applied and more quantitative issue of the demand for money during inflation. That leads to our third contribution to the literature, namely an empirical analysis of minting during inflation, which supports the main results of our model.2 Our paper is also related to 2 Extending the analysis to issues of inflation comes at the cost of simplification. Instead of using search or cash-in-advance models as the above papers, we use a model with utility from money. 3 other historical accounts of debasements. The closest is Sussman (1993) which deals with the same historical episode, but there are many other historical episodes of inflating commodity money by debasement, not only in France. A number of studies examine similar episodes in early periods of modern Europe.3 The paper is organized as follows. It begins with historical background, then discusses the theory, and finally presents the empirical results. Section 2 describes the historical episode and the debasement process. Sections 3-6 present the theory of commodity money inflation. Section 3 outlines the model, section 4 analyses minting and prices, Section 5 studies inflation dynamics under debasements, and Section 6 studies the effect of expected stabilization. Section 7 presents the data and descriptive statistics, and Section 8 describes the method and presents the results of the empirical analysis. Section 9 concludes. 2. Historical background During the French economic and commercial expansion of the thirteenth century, there was a growing demand for a common medium of exchange to facilitate commercial transactions. That development coincided with rulers’ efforts to reaffirm their sovereignty by controlling the currency and raising seignorage revenues. They achieved these objectives by establishing mints that charged seignorage for coining private bullion into royal coins. By the end of the thirteenth century these mints were gradually replacing private mints. The royal mint system expanded throughout the fourteenth century and by 1415 there were 24 mints operating in France, requiring a relatively sophisticated 3 See Bordo (1986) for a survey, Gould (1970) for the Tudor debasement, Kindleberger (1991) for debasements during the 30 years war; Miskimin (1984) for France; Motomura (1994) for Spain and 4 monitoring mechanism. A mint master operated each local mint. The central administration encouraged the mint master to produce coins by paying him a given percentage of the coins he struck. It also appointed royal officials to monitor the various activities of this economic enterprise. Moreover, it required the mint to submit random samples of coins for inspection in Paris. As a further reflection of the influence and central control of the Parisian administration, the regional mint accounts were written in the French of the court, whereas all other local fiscal accounts were written in Latin or local dialects. This relatively well-organized and well-monitored mint system gave the crown an instrument capable of effectively carrying out its monetary policy. Mints combined pure metal with base alloys to produce an alloy of a given fineness and then cut it into coins. The coins' face value, denominated according to prevailing unit of account, was not stamped on them but rather assigned by the crown. The prevailing accounting system in France was the tournois system, based on the denier tournois, the penny of Tours. In this system twelve deniers equaled one sou, and twenty sous made up one livre. The livre tournois was the numeraire in the French economy by which all commodities, silver and gold included, were valued. Royal mints produced the following three types of coins: 1) full bodied gold coins of denominations greater than one livre usually, 2) silver coins of 50 to 100 percent fineness valued at fifteen, ten (the most popular), five and three deniers, and 3) petty coins, containing less than 20 percent silver, valued at two, one and one half denier. The money supply was generated primarily through minting of private bullion. The monetary authority offered to exchange, at the ‘mint price’, any amount of bullion (or foreign coins) in return for royal coins. Besides minting fresh bullion, the mint Pamuk (1997) for the Ottoman empire. 5 would also ‘remint’ older coins. Reminting occurred both in periods of ‘debasements’ and during currency reforms. A debasement was an act by the monetary authority of lowering the silver content of the livre tournois, usually by issuing a new coin with the same face value, but with smaller content of silver. As a result people could make arbitrage profits from reminting their old coins into new ones, even if some of the coins are paid to the ruler as seignorage. Also, recoinage was carried out, usually by decree, during currency reforms. These reforms took place after periods of repeated debasements or in response to the physical deterioration of the currency. We therefore refer to them in the paper in the more modern term stabilization. The objectives of medieval monetary authorities were similar to those of their modern successors. Ordinarily, the monetary authority was concerned with managing the money supply by responding to fluctuations in market prices of precious metals, and by dealing with problems arising from wear and tear of coins in circulation. It also addressed other concerns such as monitoring the mints, combating counterfeit and maintaining the quality of royal coins through legislative and enforcement measures. In periods of fiscal crisis the crown had an additional objective, namely to increase seignorage revenues. This was achieved by debasing the currency, usually by reducing the content of silver in the new coins issued. Hence, debasements generated inflation by increasing the nominal value of bullion, as in modern devaluations. It also increased the money supply through greater minting and reminting. During a prolonged period of debasements, reminting increased significantly, as the mint price rose frequently and induced reminting of older coins. This provided the crown with seignorage revenues at times when inflationary expectations reduced the incentive to sell fresh bullion to the mint. 6 One issue that emerges here is the circulation together of coins with various levels of fineness. Reminting reduced the scope of this phenomenon but as long as people did not remint all their coins, but only those with highest content of silver, there was more than one coin in circulation. Could people distinguish between these different coins? The answer is that they could, but only by help of experts, namely this information was costly. While increases in face value or weight of coins were transparent, changes in fineness were difficult to detect, as no information was released to the public whether the change in mint price was due to change in fineness or to seignorage rate or to both. In order to find fineness one needed to assay the coins, which was an expert’s job. We have historical evidence to the existence of moneychangers in medieval Europe, who specialized in coin evaluation and exchange. They were usually expert goldsmiths, either government agents or private entrepreneurs. Surviving archival documents inform us about their operations. "Changers manuals," that served as professional textbooks, describe in detail the procedures for essaying and evaluating coins. Changers account books shed light on their actual activity and indirectly on coin circulation in the regions they operated in. Surviving accounts show that the changers were fully aware of the debasement process since they catalogued, in detail, the coins from the various issues and determined their exchange rates with foreign and with full bodied older coins. It is therefore plausible that changers were amongst the first to observe debasement of coinage and that they acted as middlemen between the public and the mint. Costly information can explain both how different coins could circulate together on the one hand and how people could know which coins to remint on the other hand. If information is costly it is purchased only when the benefit is sufficiently 7 high. Thus individuals did not go to an expert before each transaction at the marketplace and hence coins circulated by tale in the goods markets. But people did go to an expert after a debasement to check which coins to remint. The main period of fiscal crisis and debasement we explore in this paper is during the Hundred Years War. The war between England and France, which began in the 1330s and lasted with intervals until 1452, placed a heavy burden on government finance. The fiscal resources at the disposal of the French monarchy were designed to cover its regular expenses. Financing a war required additional resources on a grand scale. The French crown resorted to raising seignorage revenues by means of debasing the royal coinage primarily because seignorage was part of the traditional feudal rights of the king. As such, the crown did not require the consent of the representative assemblies for levying this tax. Other taxes were always contested, hard to obtain and required extensive and lengthy bargaining to secure. Moreover, the collection costs involving seignorage revenues were small and the flow of funds to the treasury timely. The extent of debasement depended on the (mis)fortunes of war and on the political bargaining power of the king. The Hundred Years War witnessed two periods of extensive debasements: 1337-1360 and 1418-1436. The first was associated with the outbreak of the war, the major French defeats at Crecy and Poitiers (when King Jean II was captured by the English and held for ransom) and the onset of the Black Death. The second period followed the defeat at Agincourt and the civil war between the Armagnac and Burgundian factions. 3. The Model Consider a small open economy in a discrete time framework. There are three goods in the economy. The first is an aggregate consumption good. It is produced by labor 8 only and each unit of labor produces 1 unit of the physical good during each period. The consumption good is assumed to be tradable. The second good is silver in the form of bullion, which are also internationally traded. Silver can be lent or borrowed in the world’s capital market at a world interest rate, which is assumed to be fixed and equal to r. International price of the consumption good in terms of silver is 1. The third good is money in the form of coins, which contain silver. Money is non-traded internationally, but is the only legal tender within the economy. The price of silver in terms of money is denoted Pt. Money is issued by mints, who offer Qt coins for 1 unit of silver in period t. We call Qt the ‘mint price’. The proportion of silver in coins, which are issued in period t, is ft, which we call ‘fineness.’ We assume that all coins have the same weight h, where 1 is the weight of one unit of silver.4 The overall amount of coins that can be made of one unit of silver is 1/hft, but consumers who bring silver for minting get fewer coins, since the government extracts seignorage from any minting by the mint. We denote the rate of seignorage in period t by st. Hence: (1) Qt = 1 (1 − s t ) . hf t In this paper we consider situations where Qt is increased by the government, by reduction of fineness. Such an increase is called ‘debasement’. More precisely, we consider situations of repeated debasements for a long period of time, during which the mint price rises significantly. Mints issue new coins in exchange not only of silver bullions, but also in exchange of old coins. Here we should distinguish between two cases. The first case occurs during debasements, where the coins brought to the mint are turned to coins 4 Historically not all coins had the same weight, but we assume it for the sake of simplicity. 9 with lower fineness. We call this ‘reminting’. The second case occurs in a stabilization, which follows a long period of successive debasements. In this case coins are turned into coins with higher fineness, and we call it ‘recoinage.’ Of course, the two types of exchange require different technologies, as reminting only requires adding cheap metal to coins, while recoinage requires extraction of silver from old coins before issuing new ones. Hence, recoinage is more costly than reminting. We formally assume that recoinage costs x per one unit of extracted silver. We next lay out the informational assumptions of the model. First, we assume, for the sake of tractability, that mints operate at the beginning of each period before trade in goods takes place, namely before payments by money are made. Our main assumption is that all coins look alike for ordinary folks and cannot be distinguished without help of experts, who are called ‘money changers.’ Such help is costly. To simplify things we assume the following cost structure: in each period an individual can obtain one evaluation of his coins for free, but additional evaluations are infinitely costly. As a result, an individual chooses one time in each period to evaluate his coins. We also assume that during a period many transactions take place and coins circulate many times. As a result individuals cannot keep track of the composition of coins they use and hold. Hence, their optimal strategy is to check coins at the beginning of each period, in order to decide which coins should be reminted, which coins should be turned into silver and which should be kept in circulation. During the period, when goods are continuously traded, the set of coins changes, the information is lost and all coins look alike. Hence, as a result of the law of large numbers, by the end of each period the composition of coins held by each individual is the same as the economy-wide composition. 10 We would like to further discuss our informational assumption that coins with different fineness could not be distinguished in ordinary daily transactions, but only by ‘money changers’. In other words coins circulated by tale and not by weight, or not by intrinsic value. This is a rather strong assumption, as pointed by Rolnick, Velde and Weber (1996), since it means that agents repeatedly remint their old coins and thus lose seignorage on these coins. We have three historical findings that support this assumption. The first is the evidence on inflation in commodity prices during debasement episodes, as documented in Sussman (1993). This means that coins were used as numeraire in their face value, and commodities were not priced by silver, even in times of repeated debasements. The second finding is that the volume of minting and reminting was high during periods of debasements, as shown later in the paper, and so was the volume of seignorage. Since it is not likely that mints coined only new bullion, it is reasonable that much of their activity was reminting. The latter conclusion is also supported by evidence from coin hoards of the time. These show that during stable periods the public held a variety of coins from many vintages, but hoards from periods of debasements contain mostly the newest vintages and almost no ‘old’ coins. This is evidence for circulation by tale and not by weight, since agents would not mind holding old coins if they had circulated by weight. We next describe individuals in the model economy. There is a continuum of size one of consumers with infinite life horizon. Each supplies one unit of labor in each period and thus produces 1 unit of good. For the sake of simplicity they are assumed to be risk neutral. They derive utility from consumption and from money holdings. This model therefore follows the tradition of money in the utility function, which began with Sidrauski (1967), and follows the open economy version in Obstfeld and Rogoff (1996, Ch. 8). Utility of individuals in time 0 is: 11 ∞ m U = ∑ (1 + ρ ) −t c t + v t , t =0 Pt (2) where mt is the amount of money (coins) held by the individual at the beginning of period t, after all transactions at the mint are completed, and v is concave. For the sake of simplicity we assume that the subjective discount rate is equal to the interest rate, i.e. ρ = r. The government imposes no taxes and finances its activity by seignorage only. In each period it sets both fineness ft and a seignorage rate st from minting new coins and uses the seignorage revenues to finance its expenditures. We assume that these expenditures are imports from abroad and hence the government must extract the silver from the revenues domestic coins. The silver value of these revenues is therefore: gt = hstntft(1-x) where nt is the amount of minting and reminting, namely of production of new coins. An alternative assumption, that the government uses its seignorage revenues for domestic purchases rather than imports would not change the main results of the paper. Historically, the crown used seignorage income for both types of purchases, but we need to set some assumptions in order to close the model.5 Finally, the government can also stabilize the currency. A stabilization consists of replacing the old coins with new ones, which have higher fineness, namely reduce the mint price Q and fix it at the new lower level thereafter. We assume that all markets are perfectly competitive and that expectations are rational. We first analyze a process of debasements and inflation, assuming all future policies to be fully known in advance. In the next stage we add a possible stabilization and allow for uncertainty with respect to the timing of the stabilization, which ends the process of debasements. 12 4. Minting Decisions and Prices We begin our analysis of equilibrium dynamics by looking at minting, reminting and extraction decisions of agents. Remember that this decision is taken in the beginning of the period, after the consumer takes the stock of money to the expert and learns what coins he has. First, as long as the price of silver, which is also the price of the consumption good Pt, is less than the mint price Qt, there is incentive for more minting and the quantity of money increases. Second, reminting occurs for all coins with sufficiently high fineness, namely if it can increase the number of coins. Formally, all coins with fineness f such that (3) hfQt = f (1 − st ) ≥ 1 ft are reminted. Note that fineness is non-increasing over time, namely f t ≤ f t −1 for all t, and the inequality is strict when a debasement occurs. Hence, all coins from periods prior to τ(t), where fτ(t)(1-st) < ft and fτ(t)-1(1-st) ≥ ft, are reminted in t, and fτ(t) is the highest fineness held by agents. Consumers can also bring coins to the mint to exchange with silver, as long as the value of extracted silver exceeds the number of coins used. Hence, they extract the silver from coins of fineness fu if (4) Pt ≥ 1 1 . hf u 1 − x The supply of money can therefore be described by a step function, as in figure 1. The amount of money mt,r is the amount after reminting and before bullion minting or extraction take place. This amount does not depend on the price Pt, since reminting does not depend on price, as seen in equation (3). The demand for money is the 5 The crown indeed listed in its accounts the silver value of its seignorage revenues. 13 demand of consumers only, as the government imports only. The demand for money is proportional to the price level Pt and is presented in Figure 1 by a ray from the origin. The equilibrium, which determines the equilibrium price level and the equilibrium quantity of money is determined by the intersection of the supply step function and the demand for money. The equilibrium price must, therefore, be within the following range: 1 1 1 ≥ Pt ≥ Qt = (1 − s t ) . hf t 1 − x hf t (5) Figure 1 presents three possible equilibria. If the demand for money is small, as in D’, coins are transformed to silver by extraction and mt=m’. If the demand for money is large, as in D’’, bullions are minted into coins and mt=m’’. If the demand for money is D, there is neither silver extraction nor silver minting and mt=mt,r. Consider next the effect of debasement on equilibrium. A debasement introduces a new coin with lower fineness. Hence it raises Qt and shifts some of the supply curve upward. If the new fineness is low enough, so that ft falls below fτ(t-1)(1-st), there is reminting, which shifts the whole supply curve to the right as well, as it makes the upper step in the supply curve wider. Hence, a debasement tends to raise the price. Clearly, there can be a debasement, which leaves the price unchanged, if there is no reminting and if the previous price exceeds the new mint price. But if debasements are repeated, they finally raise prices, since the equilibrium price exceeds the mint price. Thus, repeated debasements lead to inflation, which is analyzed in the next section. When the authorities declare stabilization, all coins must be reminted and hence the supply of money becomes infinitely elastic at the new mint price Qt. As a result, the equilibrium price, in the case of stabilization, is equal to the mint price Qt. 14 5. Debasements and Inflation In this section we consider the case of repeated debasements at a fixed rate π. Consider the following monetary policy: the government collects seignorage at a fixed rate, namely st = s, and it debases the currency every period at a fixed rate π, i.e. (6) Qt f = t −1 = 1 + π Qt −1 ft for all t.6 If the rate of debasement is fixed, there is a fixed number of types of coins in circulation, which we denote by T. Every period a new coin is introduced and the oldest coin is reminted. T is bounded by the following inequalities, which are derived from (3): (7) 1 ≤ (1 + π ) T −1 (1 − s ) < 1 . 1+π We next show that after a few debasements the price Pt becomes equal to the mint price Qt. To see this note that the monetary dynamics are: (8) mt = mt −1 + nt −T [(1 + π ) T (1 − s ) − 1] + Qt et , where nt is the amount of coins minted in time t and et is the amount of bullion minted into coins in t. If there is no minting of new bullion, we get from (8): mt ≤ mt −1 [(1 + π ) T (1 − s )] and the term in brackets is smaller than 1+π according to (7). Hence, if there is no minting of new silver, the quantity of money grows at a rate lower than 1+π. This cannot last long and hence after a few debasements there must be minting of new 6 Historically, the debasement episodes consisted not only of reduction in fineness, but often of increased seignorage rates as well. In the theoretical part of the paper we treat inflation and seignorage rates as independent. We return to this issue in the empirical part of the paper in Section 8. 15 silver. Note that silver is minted only if the equilibrium price equals the mint price, as shown in Figure 1, and hence: (9) Pt = Qt , and this equality holds from then on. The intuition behind this result is simple. Since the government uses the silver it gets as seignorage outside the economy, it reduces the silver contents of coins continuously. Hence, consumers need to mint new bullion, which they would not have done had the price of silver exceeded the mint price.7 In the rest of the section we focus on the steady state equilibrium. As we have seen the rate of inflation at the steady state is π and the price is equal to the mint price. We differentiate between two cases. In the first there is more than one type of coins in circulation, i.e. T>1. In this case reminting is partial. In the second case the rate of inflation is high so there is only one coin in circulation, i.e. T=1. In this case all former coins are reminted. 5.1. Debasements with Partial Reminting We next describe the steady state distribution of types of coins when the number of types T is greater than 1.8 The quantity of coins of fineness ft-u for all 0 ≤ u ≤ T-1 is the quantity of coins minted in period t-u, and is equal to (10) n t − u = mt π (1 + π ) −u , 1 + π − (1 + π )1−T where mt is the aggregate amount of money, which we derive next. Note that the distribution of coins as described in (10) is both economy-wide and also holds for any individual by end of trading period, due to high circulation of coins. 7 We should stress here that even if the government uses its seignorage revenues within the country and as a result the equilibrium price is not always equal to the mint price, the main results of the model do not change at all. 8 It can be shown that the distribution of coins converges to this steady state distribution. 16 The individual maximizes utility (2) with respect to the budget constraints. We next calculate the marginal benefit and marginal cost of holding money in order to find the demand for money. The marginal utility of real money balances is v′(mt / Pt ) . In calculating the marginal cost of money the individual takes into consideration that some coins will remain in circulation in next period and some will be reminted, thus having different rates of return. Since the individual has no control over the distribution of coins he will hold by end of period, he can only calculate the expected marginal cost of holding money, based on the distribution (10). The marginal real cost of holding coins, that will not be reminted next period, is due to inflation and loss of interest, namely: (11) 1− 1 1 . 1+ r 1+π The marginal cost of holding coins, which will be reminted next period, is lower, since reminting increases the number of coins, and is equal to: (12) 1− 1 (1 + π ) T (1 − s ) , 1+ r 1+π which is smaller than (11) due to (7). Given the distribution of coin types (10) we get that the expected marginal cost of money is: (13) 1− 1 1 1 − (1 + π )1−T + π (1 − s ) . 1+ r 1+π 1 − (1 + π ) −T Equating the marginal cost and marginal benefit of money yields the equilibrium real balances in the economy, since only consumers hold money: (14) m v ′ t Pt 1 1 1 − (1 + π )1−T + π (1 − s ) = 1 − . 1+ r 1+π 1 − (1 + π ) −T This equation shows that in equilibrium real balances (the demand for money) depend both on the rate of inflation and on the rate of seignorage. Furthermore, the number of 17 coins in circulation T is an endogenous variable, which depends on these two variables as well. In order to see how real balances depend on π and s in the reduced form, consider the rates of debasement, at which the number of coins changes and falls from T+1 to T. This rate is determined by the condition: (1 + π ) T (1 − s ) = 1 . At this rate the marginal costs of all types of coins are equal and given by (11). Hence, the equilibrium real balances are described by: m v ′ t Pt (15) r + π + rπ = . (1 + r )(1 + π ) We, therefore, conclude that real balances depend negatively on the rate of inflation as long as more than one type of coins circulates. While equations (14) and (15) determine the equilibrium stock of money, our data from Medieval France consists only of flows of minting, as reported by the various mints. Luckily, our model enables us to easily find the flow of minting, which depends on the demand for money and on the distribution of coin types. The amount of minting n is therefore given by: (16) nt mt π = . 1−T Pt 1 + π − (1 + π ) Pt From this equation we see that inflation affects minting in three channels. First, the overall demand for money m/P falls with inflation. Second, higher inflation reduces the value of old coins more rapidly and that increases minting as shown in the first term in the RHS of (16). This exerts a positive effect of inflation on minting. Third, higher inflation reduces the number of coin types in circulation T and that also affects minting positively. In order to consider the three effects together, consider again the rate of inflation at which the number of coins falls from T+1 to T. At this rate minting is equal to: 18 nt 1 π mt = . Pt s 1 + π Pt (17) Hence, inflation affects minting in two ways: positively by reducing the number of types of coins in circulation and negatively by reducing the demand for money. The overall effect depends on the elasticity of the demand for money with respect to π. Minting is negatively affected by π if this elasticity is greater than 1/(1+π).9 Minting is also affect by the rate of seignorage, which has a negative effect. 5.2. Debasements with Full Reminting We next examine the case where inflation is so high, that all the old coins are reminted and there is only one coin in circulation, i.e. T=1. This case holds when (1 + π )(1 − s ) > 1 . (18) In this case the marginal cost of money is given by (12), since all coins are reminted, and is equal to: 1− 1− s . 1+ r Equating the marginal cost with the marginal benefit of money yields: (19) m v ′ t Pt r+s = . 1+ r Hence, the demand for money in this case does not depend on the rate of inflation but on the rate of seignorage only. This is a very surprising result, and it is unique for inflation in commodity money. More precisely, it is a result of the intrinsic value of coins, namely of their silver content, in addition to their transaction value. When the rate of inflation is high, holders of commodity money can avoid some of the inflation tax by reminting. In 9 In our historical episode the effect of inflation on minting is negative, as shown in Section 8. 19 doing so they reduce their losses to the fixed seignorage only. As a result they can hold more money and their demand becomes insensitive to the inflation rate. Note that this strategy is not possible under fiat money. The rate of inflation at which individuals begin to remint all their coins and at which the demand for money depends only on the rate of seignorage is (20) π* = s . 1− s When inflation exceeds π* and full reminting prevails, the real amount of minting is equal to real balances described in (19), since all coins are new. Hence, when inflation exceeds π* the amount of minting also depends on the rate of seignorage and not on the rate of inflation. Section 8 presents some empirical evidence that supports this theoretical result. 6. Debasements and Stabilization In section 5 we describe a debasement process that goes on forever. This is a helpful but not very realistic simplification. Rulers could not debase the currency forever by bringing fineness as close as possible to zero, since at very low levels fineness becomes indistinguishable from zero and commodity money loses all its value. This level could not be reached and the public knew it as well. Indeed, our historical records show that periods of repeated debasement, which reduced fineness to very low levels, ended in stabilizations. Since such stabilization was anticipated it affected the demand for money. In this section we add the effect of this anticipation to the analysis and bring it closer to reality. We assume as above that there is a fixed rate of debasement π and a fixed rate of seignorage s, and that the rate of debasement is so high that agents remint all coins every period. We assume that the probability of 20 stabilization is positive, and denote this probability in period t by zt. Later on, we make this probability endogenous as well. We solve the model in two stages, after and before the stabilization takes place. We first calculate the optimal value of utility from the stabilization on, when the economy returns to full certainty and to full price stability. If stabilization occurs in period t, then optimal utility V S depends on the accumulated amount of silver bullion bt-1 and on the amount of real balances held, and is equal to (21) m 1+ r m 1+ r + bt −1 (1 + r ) + t −1 (1 − s )(1 − x) − l * + V S bt −1 , t −1 = v(l*) Pt −1 r Pt −1 r where l* is the amount of real balances after stabilization, which is determined by (22) v ′(l*) = r . 1+ r Denote by V the optimal value of utility prior to the stabilization in period t. Then the Bellman equation is: (23) m m V bt −1 , t −1 = max ct + v t Pt −1 Pt z t +1 S mt + V bt , Pt 1+ r 1 − z t +1 mt + V bt , Pt 1+ r under the constraint: (24) ct = 1 + mt −1 m (1 + π )(1 − s ) + bt −1 (1 + r ) − bt − t . Pt Pt Before we derive the first order conditions, note that due to the envelope theorem, the partial derivatives of V are (25) Vb = 1 + r and Vl = Pt −1 (1 + π )(1 − s ) . Pt The first order conditions of (23) are, therefore: 21 (26) 1= 1 − z t +1 z t +1 Vb , (1 + r ) + 1+ r 1+ r which indeed fits (25), and: (27) z 1 − z t +1 Pt m v ′ = 1 − t +1 (1 − s )(1 − x) − (1 + π )(1 − s ) . 1+ r 1 + r Pt +1 P Hence, the demand for money falls as the probability of stabilization rises. We next turn to find the rate of inflation. We prove that if the seignorage rate is high enough, which has been the case in our historical episodes, price equals the mint price Qt. The equilibrium price is affected by opposite demand and supply effects. On the one hand demand for money is reduced as probability of stabilization increases. On the other hand, if there is no minting of new bullion, money supply grows by (1 + π )(1 − s ) − 1 according to (8), which is much lower than the rate of debasement π. Hence, if the rate of seignorage s is sufficiently high there is always minting of new bullion and the equilibrium price equals the mint price.10 Hence, the rate of inflation is equal to π. Substituting in (27) yields: (28) m v ′ t Pt r + s + (1 − s ) xz t +1 = . 1+ r Hence, the demand for money depends both on the rate of seignorage and on the probability of stabilization. This probability has a negative effect on the demand for money, since agents wish to minimize the cost of recoinage, of converting debased coins to good coins. We next try to describe how the probability of stabilization evolves over time, using a Bayesian learning process under very simple assumptions. Assume that the public only knows that the process of debasement cannot go on to zero fineness, and 22 there is a minimum level of fineness f*. If the economy is expected to reach this fineness in period T*, and there has been no stabilization until t, the probability of stabilization is uniform, namely it is (29) z t +1 = 1 . T * −t Fineness falls at a rate π, and hence the time until T* can be deduced from f * = f T * = f t (1 + π ) − (T *− t ) . Hence, the probability of stabilization is (30) z t +1 = 1 log(1 + π ) . = T * −t log f t − log f * The probability of stabilization, therefore, depends negatively on fineness. The lower fineness is, the higher is the probability that the process of debasements ends soon. This probability also depends positively on the rate of debasement. Finally note that since only one coin circulates the amount of minting is equal to the amount of money: nt = mt. Hence, minting depends negatively on the rate of seignorage and negatively on the probability of stabilization. As debasement continues, anticipation of stabilization rises, and hence minting is reduced. This is also an explanation to the puzzle raised by Rolnick, Velde and Weber (1996), who find the amount of minting to be too small given the rates of inflation in such situations. 7. Data and Descriptive Statistics The data used in this paper is derived largely from original mint accounts found in the national French archives and in the regional archive of the Isere at Grenoble11. These 10 Note that without this assumption the price would be higher than the mint price but the qualitative results of the model would remain the same. This is therefore only a simplifying assumption. 11 For greater detail see Sussman (1997). 23 periodical accounts were submitted by the mints to the central monetary administration in Paris and contained information about the characteristics of the coins produced, the quantity minted, the costs, the seignorage revenues and the net profit of the mint. Due to losses, fires and wars the extent of coverage of the documents is not complete. We have data only for some of the mints and in many cases there are gaps in the data for certain years. Notwithstanding, the data we have allows us to assemble a data set that covers the major periods of debasements during the 1350s and between 1415 and 1422 from 12 mints of varying importance and geographical locations. It is important to note that the data does not come in fixed periods of time but rather in periods with varying lengths, since the frequency of submitting mint accounts to the auditors in Paris was not uniform. The accounts cover periods as short as one day to periods as long as fifteen months, and the average length of account is one month. Accounting periods varied between mints and over time. Under normal circumstances accounts were submitted every six months or annually. However, during the debasement period, the accounts were submitted more frequently. This phenomenon reflects the tighter fiscal control over the mints, which had to submit the accounts and the profits on a more timely basis. Moreover, the accounts were usually closed, under royal directive, following changes in any of the characteristics of the coinage. In periods of debasement the changes were frequent and therefore the accounts cover shorter periods. A further complication arises from the fact that royal orders reached mints with varying delays, due to the large distances between the mints and Paris, due to problems of travel in war zones and due to necessity to sometimes pass through provincial administrative centers. 24 Although the data is in varying lengths of time, they cover continuos periods of time for the 12 mints. Hence, they enable us to calculate the main variables and how they evolve over time. The variables that are relevant for the model are mint prices, rates of inflation, seignorage rates, and amounts of minting. The data are pooled and allow us to draw some generalizations and to test the hypothesis derived from our model. We first present some descriptive features of the data on French debasements in the years 1330-1436. The first debasement period was characterized by repeated cycles of debasement and revaluation. The period from 1337 to 1354 witnessed 34 mild debasement cycles with relatively long periods of stable money (figure 2). The period from 1354 to 1360 saw 51 rapid debasement cycles that reached hyperinflationary magnitudes in 1360 (figure 3). The average increase in the nominal value of silver during such a cycle was 200 percent and the average duration of a debasement cycle was 400 days. The largest debasement cycle increased silver price by 600 percent, and lasted only 116 days. The smallest cycle increased price by 66 percent. The shortest debasement cycle was 33 days during which the nominal value of silver increased by a 100 percent. The period from 1417 to 1422 was characterized by a prolonged process of debasement during which the nominal value of silver was increased by 3500 percent without any attempt to stabilize the currency (figure 4), milder debasements (average of 80 percent per cycle) followed until 1436 (figure 5). This description of the dynamics of silver prices in this period shows that indeed the government could inflate commodity money in high rates. The debasements resulted in substantial minting and large government revenues. While complete data for all the mints operating in France is lacking, the data we found at the French archives allows us to assess the quantitative aspects of 25 these debasement episodes. Figure 6 shows the mint outputs of four major French mints. The total mint output for the four mints in 1355 was about 75,000 marcs of pure silver (20 tons) whereas the annual average of total minting in France in non debasement years was 5,000 marcs. The revenues secured by the government were also impressive: according to Maurice Rey, the 1419 seignorage revenues amounted to six times ordinary royal revenues. Figures 7, 8 and 9 show, respectively, minting levels and seignorage revenues at the mints of Rouen, Montpelier and the Dauphine mints (Cremieu, Mirabel and Romans). The figures illustrate the high share of seignorage revenues out of total minting. It is interesting to compare the experience of Rouen (Figure 7) and Montpelier and (Figure 8). In 1356, following the capture of King Jean by the English at Poitiers, the Estates of Languedoc (southern France) voted to suspend debasement whereas the mints of the North continued to debase the currency. In response, mint outputs and seignorage revenues in Montpelier started to decline, while at Rouen they reached an all time high. In the theoretical section of the paper we identify the price of silver with commodity price. We further add assumptions that make the rate of inflation equal to the rate of debasement, the rate of increase of mint price. It is interesting to examine whether historical data can justify these assumptions. Unfortunately, high quality price data for France are lacking. Nevertheless, reproducing in Table 1 data reported by Sussman (1993) for the Dauphine, we see that grain prices followed the course of mint prices whereas the price of gold followed the price of silver. 8. Empirical Analysis Our model describes how the demand for commodity money and the amount of minting are related to three main variables: the rate of inflation, the rate of seignorage 26 and the anticipated probability of stabilization, and how this relationship changes at different levels of inflation. Since we do not have data on the quantities of money but rather on the amounts of minting, we use this data to test the main conclusions of the model. Namely we examine how minting depends on the rate of inflation, on the rate of seignorage and on the probability of stabilization. Before we describe the empirical analysis in detail we address the issue of the correlation between the seignorage rate and the rate of inflation. We know from our records that as inflation increased so did the rate of seignorage, as the ruler tried to extract greater income from debasements. There is a clear positive correlation between the rate of decline of fineness and the rise in seignorage rate. We have calculated these correlations for various mints and they are not so high, namely less than 0.5. Hence, the two variables, inflation and seignorage are related but can still be used as explanatory variables in regression analysis. Our empirical analysis has two parts. In the first part we examine a basic equation, of minting as a function of the rate of inflation and the rate of seignorage, and excluding for the meanwhile the probability of stabilization. We estimate this basic equation considering two cases, that of low inflation and partial reminting and that of high inflation and full reminting. Our hypothesis is that the effect of the rate of inflation is weaker at higher rates of inflation. In the second part of the analysis we estimate a measure of the expected probability of stabilization based on the model and add this measure to the minting equation as a third variable. Our hypothesis in this case is that minting is negatively related to the probability of stabilization. Our regression estimates are based on a panel of data pooled from 12 mints that includes the debasements episodes described above. As discussed above, due to the varying lengths of mint accounts, the quantities of minting are from periods of 27 time of different lengths. In order to account for that and to normalize the minting data we added the length of the account period as an additional explanatory variable to the regressions. The results of the first part of the analysis are presented in Table 2. Regressions I and II in this table confirm the main hypothesis of our model, as described by equation (18). We find that minting is negatively affected by both the seignorage rate and the annual inflation rate. We then proceed to test whether the effects of inflation and seignorage differ under low and high inflation rates. We examine the effect of inflation on minting at rates below and above 50%. Remember that according to equation (23) reminting is full above π* = s/(1-s). During the period when inflation was bellow 50% the average seignorage rate was 27% with a maximum of 50% which roughly corresponds to the inflation rate calculated from the model. When inflation exceeded 50% the seignorage rate was higher at 37% on average and with a maximum rate of 75%! Indeed, equations III and IV in Table 2 show that the effect of inflation is much larger and more significant than the effect of seignorage in levels of inflation below 50 percent. However, as shown in equations V and VI in Table 2, at higher inflation rates - around 100% - with complete reminting, we find that the effect of the seignorage rate dominates that of inflation, and that the effect of inflation even becomes zero and insignificant. In the second part of our empirical analysis we add a third explanatory variable, namely the probability of stabilization. Following is an explanation of how this probability is estimated. In every period t we know the actual duration until stabilization, i.e. t − t , where t is the actual date of stabilization. Expected duration until stabilization is equal to (T*-t)/2 under the assumption of uniform distribution, but it is also equal to the expectation of t − t . Hence, we can write: 28 (31) t −t = log f t − log f * T * −t + ε t ,t = + ε t ,t . 2 2 log(1 + π t ) We therefore estimate a regression of the actual time to stabilization on two explanatory variables: the logarithms of fineness and of the rate of inflation. The estimated equation yields the probability of stabilization as a function of these two variables. This regression is presented in Table 3 and it indeed shows that the time to stabilization decreases with inflation and increases with fineness. Therefore, the probability of stabilization rises with inflation and is negatively related to fineness. After estimating the probability of stabilization as described above, we add this probability as an explanatory variable to the minting equation. This is presented in Table 4, which shows that this probability has a significant negative effect on minting, beyond that of the seignorage rate and of inflation. Note that this result is in contrast to the effect of expected stabilization in an economy with fiat money, in which anticipated stabilization increases the demand for money. Here it reduces it. As mentioned above, this result can resolve what Rolnick, Velde and Weber (1996) present as an empirical puzzle. They claim that the amount of minting during debasements is too small to justify circulation by tale. We show that if we take into consideration the probability of stabilization, it can account for smaller demand for commodity money and for less minting during the last phases of debasement episodes. 9. Summary and Conclusions In this paper we show that inflation and even high inflation is possible under a commodity money regime. Inflation can exist in such a regime because people prefer to use coins rather than the commodity itself. Thus, if the commodity (silver) content in coins is reduced continuously, inflation occurs. The possibility of high inflation due 29 to debasements is shown not only in a model, but also demonstrated by a hundred years of frequent debasements in medieval France. Therefore the historical commodity money regime was quite similar to the more modern fiat money regime and for a similar reason, namely that people prefer money for transactions over other assets. Despite this basic similarity between commodity money and fiat money, we observe two main differences between the two. Under commodity money the demand for money falls less when inflation becomes high. This is because coins still retain some intrinsic alternative value and can be used for reminting. Another important difference is with respect to demand for money when stabilization is anticipated. While under fiat money this increases the demand for money, under commodity money such a stabilization requires coin holders to recoin their money at a substantial cost, thereby reducing the demand for money when stabilization is anticipated. We test for these two results using data found in French archives and are able to corroborate them. Though we do not have direct data on the demand for money, but rather on minting, we show that minting behaves as indicated by our model, namely that it declines with inflation in low inflation environment and becomes less affected by inflation when the rates are high. Furthermore, we are able to show that minting declines with the increase in the probability of expected stabilization. Our model, findings and conclusions are not limited to France during the Hundred Years War. There were numerous periods of debasements in Europe in the early modern period, in the Low Countries, Spain, England, in Italian city states, in Germany and in the Ottoman Empire. Though French data are perhaps the most extensive and of the highest quality, we believe that our approach can be used to explain similar episodes in other countries and over a large period of time, characterized by the use of commodity money. 30 In this paper we assume that agents demand royal coins and trade them at face value. It could be interesting to question this very assumption itself. Is it due to the public good aspect of royal coinage? Are there economies of scale in their use? Why do people use coins at face value even when inflation is very high and seignorage rate is high as well? These are questions, which we do not address, but they are raised by our story and they are relevant for understanding the role of money not only in the past but in the present as well. 31 References Bordo, Michael D., “Money, Deflation and Seignorage in the Fifteenth Century: A Review Essay” Journal of Monetary Economics; 18(3), November 1986, pages 337-46. Gould, John D., The Great Debasement (Oxford, 1970). Kindleberger, Charles P. “The Economic Crisis of 1619 to 1623,” Journal of Economic History; 51(1), March 1991, pages 149-75. Li, Yiting, “Commodity Money under Private Information,” Journal of Monetary Economics, 36(3), December 1995, pages 573-92. Miskimin, Harry A., Money and Power in Fifteenth Century France (New Haven, 1984). Motomura, Akira, “The Best and Worst of Currencies: Seignorage and Currency Policy in Spain, 1597-1650,” Journal of Economic History; 54(1), March 1994, pages 104-27. Obstfeld, Maurice, and Kenneth Rogoff, Foundations of International Macroeconomics, MIT Press, Cambridge MA, 1996. Pamuk, Sevket, “In the Absence of Domestic Currency: Debased European Coinage in the Seventeenth-Century Ottoman Empire” Journal of Economic History; 57(2), June 1997, pages 345-66. Rolnick, Arthur J.; Velde, François R.; Weber, Warren E, “The Debasement Puzzle: An Essay on Medieval Monetary History” Journal of Economic History; 56(4), December 1996, pages 789-808. Sargent, Thomas J., and Bruce D. Smith, “Coinage, Debasements, and Gresham’s Laws,” Economic Theory, 10 (1997), pages 198-226. Sidrauski, Miguel, “Rational Choice and Patterns of Growth in a Monetary 32 Economy,” American Economic Review, 57, May 1967, pages 534-544. Sussman, Nathan, “Debasements, Royal Revenues, and Inflation in France during the Hundred Years' War, 1415-1422” Journal of Economic History; 53(1), March 1993, pages 44-70. Velde, François R., Warren E. Weber, and Randall Wright, “A Model of Commodity Money, With Applications to Gresham’s Law and the Debasement Puzzle,” Federal Reserve Bank of Minneapolis, Research Department Staff Report 215, July 1997. 33 Table 1 Annual Price Changes In The Dauphine, 1418-1422 Year Silver: Mint Par 1418 1419 1420 1421 1422 Cumulative : Gold: Grain: Mint Price Gold Price Wheat Price 50% 33% 50% 167% 200% 13% 56% 43% 75% 100% 22% 45% 88% 100% 233% 50% 40% -40% 100% 200% 2300% 775% 2122% 656% Source: Sussman (1993) 34 Table 2 Dependent variable Method Constant Seignorage rate Inflation Length of account* R2 D.W. N Mint output* Mint output* I Random Effects 5.35 (2.36) -0.77 (-2.55) -0.28 (-3.74) 0.57 (15.82) 0.5 1.62 539 II Common 5.50 (22.68) -1.01 (-3.58) -0.17 (-2.27) 0.52 (13.76) 0.70 1.38 539 Mint output* Mint output* Mint output* Mint output* Inflation < 50% III Fixed effects Inflation < 50% IV Common effect 6.06 (11.38) -0.07 (-0.12) -1.32 (-4.19) 0.55 (7.59) 0.87 1.59 107 Inflation < 100% V Fixed effects Inflation < 100% VI Common effect 5.00 (15.3) -1.76 (-4.85) 0.312 (1.88) 0.53 (12.22) 0.80 1.24 342 -0.94 (-1.57) -0.88 (-2.43) 0.53 (7.06) 0.97 1.96 107 Notes: t-values in parenthesis * - denotes log of variable. All Regressions estimated using GLS procedure with cross section weights. 35 -0.79 (-2.16) 0.07 (0.44) 0.60 (14.6) 0.90 1.57 342 Table 3 Number of days to stabilization Fixed effects -85.26 (-3.78) 238.55 (10.65) 0.47 0.4553 506 Method Inflation* Fineness* R2 D.W. N Notes: t-values in parenthesis * - denotes log of variable. All Regressions estimated using GLS procedure with cross section weights. 36 Table 4 Dependent variable Method Seignorage rate Inflation Expected Stabilization* Length of account* R2 N D.W. Mint output* Mint output* I Fixed Effects -0.72 (-2.11) -0.26 (-3.13) -0.18 (-2.20) 0.57 (15.10) 0.67 488 1.74 II Fixed effects -0.71 (-2.05) -0.29 (-3.78) 0.60 (16.6) 0.641 488 1.71 Notes: t-values in parenthesis Probability of stabilization is the inverse of the expected number of days left to the date of stabilization, as derived from Table 3. * - denotes log of variable. All Regressions estimated using GLS procedure with cross section weights. 37 Pt (1 − x ) −1 hf t D’ D (1 − x ) −1 hf τ ( t ) D’’ S Qt mt,r m’ Figure 1 38 mt m’’ Figure 2 Cumulative debasement rate France: 1337-1354 400% 300% 200% 100% 0% Aug-35 Apr-38 Jan-41 Oct-43 Jul-46 Apr-49 Jan-52 Oct-54 Figure 3 Cumulative debasement rate France 1353-1360 600% 500% 400% 300% 200% 100% 0% May-53 Oct-54 Feb-56 Jun-57 39 Nov-58 Mar-60 Aug-61 Figure 4 Cumulative debasement rate France: 1412-1422 6000% 5000% 4000% 3000% 2000% 1000% 0% Dec-10 Sep-13 Jun-16 Mar-19 Nov-21 Aug-24 Figure 5 Cumulative debasement rate France: 1423-1436 250% 200% 150% 100% 50% 0% Nov-21 Aug-24 May-27 Feb-30 40 Nov-32 Aug-35 Apr-38 Figure 6 Minting volumes: France 1350-1361 in marcs of pure silver 30000 25000 20000 15000 10000 5000 0 1350 1352 Montpellier 1354 1356 Toulouse 1358 Troyes 1360 Rouen Figure 7 Debasement Minting Rouen: 1354-1361 25000 25 20000 20 15000 15 10000 10 5000 5 0 0 1354 1355 1356 1357 Marcs minted net revenues in pure silver 41 1358 1359 1360 1361 Mint Price -livres Figure 8 Debasement Minting Montpellier: 1354-1361 10000 12 11 8000 10 6000 9 8 4000 7 2000 6 0 5 1354 1355 1356 1357 marcs minted net revenues in pure silver 1358 1359 1360 1361 mint price - livres Figure 9 Debasement Minting Dauphine: 1417-1422 30000 80 70 25000 Marcs 50 15000 40 30 10000 Livres tournois 60 20000 20 5000 10 0 0 1417 Mint price - livres 1418 1419 Marcs minted 42 1420 1421 1422 Net revenues in pure silver