Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

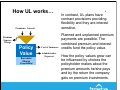

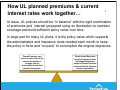

UL PRODUCTS BASICS PLC.9319.07.13 This presentation contains general educational information about Universal Life products and is not intended to promote any products or services offered by Protective Life Insurance Company. In General… 2 There are two major categories of insurance products, Term and Permanent. Universal Life insurance and Whole Life insurance are both types of permanent insurance. Because Universal Life insurance is a variation of Whole life insurance, it helps to begin with an understanding of Whole Life insurance. Let’s review key facets of Whole Life… 3 Traditional whole life plans have fixed, pre-set premiums and values. Often premiums are level. But, if premiums do change, the timing and amounts of the changes are “scheduled” and spelled-out in the contract. Cash values usually increase, gradually and predictably, over time. More about traditional whole life… 4 Similar to a “budget plan” for your electric bills—the premiums charged for a level premium whole life plan are an “average” of the insurance and administrative costs over the “lifetime” of the policy. With a level premium whole life plan— premiums paid in early years are more than what is needed to provide the coverage at younger ages when death is less likely. In later years, premiums are less than what is needed to provide the coverage at older ages when death is more likely. Finally, with traditional whole life… 5 Premiums are predetermined, as are the policy values. Since all facets of the plan are “fixed” at issue, policy values are based on a modest rate of interest. If the company is able to invest premiums at a higher interest rate when financial markets are rising, policy values on these plans do not benefit. There are (usually) no opportunities for the whole life policyholder to change premium amounts or influence the cash values or coverage amounts after buying the policy. As long as the original, fixed premiums are paid when due, the coverage can remain in effect. Even if the company gains a higher return than originally predicted on premiums invested, the policyholder does not (typically) benefit. How UL works… Premiums Interest Premium Expense Charge Policy Value Surrender Charge (if applicable) Cost of Insurance Administrative Expenses 6 In contrast, UL plans have contract provisions providing flexibility and they are interest sensitive. Planned and unplanned premium payments are possible. The combined premium and interest credits fund the policy value. How the policy values grow can be influenced by choices the policyholder makes about the premium amounts he/she pays and by the return the company gets on premium investments. How UL works… 7 Generally, companies pay higher interest on UL plans when premium investment returns are higher and lower interest rates when those returns are lower. That is what is meant by “interest sensitive”. Some newer UL plans have a “lapse protection feature” which, in some ways, makes a UL plan operate more like a fixed premium, whole life plan. Without such a feature in effect, UL plans stay in force based on having enough policy value each month to pay insurance and administrative expenses. How UL works… 8 Because premiums are flexible with UL plans, a policyholder can choose to pay more premiums in, than are necessary for just the death benefit coverage. This enables him/her to take advantage of higher interest rate credits -available when financial market investment rates are on the rise. That is what truly makes UL plans special — the fact that policy values are interest sensitive. The interest sensitive facet of UL plans can also make them more affordable than traditional whole life plans with comparable death benefits. The flexibility and interest-sensitive components of UL plans make it important to monitor how the plan is performing using the Annual Report sent around the policy’s anniversary date. In particular this is true when interest rates are consistently lower than originally projected and/or when premiums paid are less than originally projected. How UL planned premiums & current interest rates work together… 9 At issue, UL policies should be “in balance” with the right combination of premiums and interest (projected using an illustration) to maintain coverage and build sufficient policy value over time. In large part for many UL plans, it is the policy value which supports the administrative and insurance costs needed each month to keep the policy in force and “on pace” to accomplish the original objectives. Planned Premiums were chosen at issue, based on the amount and duration of coverage, plus any accumulation of cash value desired in future years. Current Interest Rates were set by the Company at issue and helped determine the amount of Planned Premiums needed to meet the objectives and plan requirements. How UL planned premiums & current interest rates work together… For some UL plans, if current interest rates go up and remain higher than projected at issue, it may be possible to lower or skip premiums and still maintain coverage and meet other policy objectives. 10 How UL planned premiums & current interest rates work together… 11 For some plans, if current interest rates go down and remain lower than projected at issue, it may be necessary to increase or supplement planned premiums to maintain coverage and still meet the original policy objectives. Some UL plans may be less affected by changes in interest rates… 12 Some UL plans have a “safety net” in the form of a lapse protection feature. For those plans, as long as the protection is in effect -- fluctuations in interest rates alone do not endanger the coverage. Timeliness of required premiums is critical, however. And, whenever the lapse protection is not in effect, policy value becomes just as important a factor as with other UL plans. Current Interest Rates Planned Premiums Lapse Protection Loans and Partial Surrenders affect policy stability and values… 13 When policy value is the basis for a UL plan staying in force, without overfunding or interest rates consistently higher than originally projected -- loans or partial surrenders destabilize the policy. Policy Value Policy Value Loans and Partial Surrenders affect policy stability and values… 14 For policies without lapse protection in effect, loans and partial surrenders directly reduce the useable Policy Value available to pay on-going monthly expenses. If there is unpaid loan interest in any year, values deplete faster as the loan is increased to pay it. Whenever policy values show a pattern of declining over multiple months/years—it means more is coming out for expenses than is offset by premium and interest credits. A policy in this state may, quickly or eventually, lapse unless one of the following occurs: (1) the policyholder makes sufficiently large unplanned premium deposit(s) (2) the policyholder sufficiently increases planned premiums (3) the policyholder reduces/repays an outstanding loan (4) the company raises interest rates substantially. UL basic concepts recap… • • • • • • • • 15 Traditional whole life plans have “fixed” components – and are not interest sensitive. UL plans are flexible and interest sensitive -- newer versions may include a lapse protection feature. Interest sensitivity helps when interest rates are on the rise, allowing lower or skipped premiums, faster cash value growth and fewer ill effects from loans/partial withdrawals. Declining interest rates can make UL plans more vulnerable to lapsing, sometimes necessitating an increase in premiums. Loans, unpaid loan interest and partial withdrawals make UL plans more vulnerable to lapsing – sometimes necessitating an increase in premiums. A combination of lower interest rates and loans/partial withdrawals definitely increases the possible need for increased premiums to avoid a lapse of coverage. UL plans’ flexible and interest sensitive nature make them an affordable and appealing whole life coverage option – for both consumers and insurance companies. Monitoring the status of a UL plan is particularly important whenever there are periods of declining interest rates and when premium deposits decrease or values are withdrawn.