Eurosystem Monetary Targeting: Lessons from U.S. Data ¤ Glenn D. Rudebusch

... models. For example, Smets [37] surveys the central bank models from 12 di¤erent countries (including 6 of the countries in the euro area) and notes: In most of the central banks’ macroeconometric models the transmission mechanism of monetary policy is modelled as an interest rate transmission proce ...

... models. For example, Smets [37] surveys the central bank models from 12 di¤erent countries (including 6 of the countries in the euro area) and notes: In most of the central banks’ macroeconometric models the transmission mechanism of monetary policy is modelled as an interest rate transmission proce ...

A Monetary Explanation of the Great Stagflation

... March, the price of crude oil has jumped to almost $26 a barrel, up from less than $10 last December and its highest since the Gulf war in 1991. This near-tripling of oil prices evokes scary memories of the 1973 oil shock, when prices quadrupled, and 1979-80, when they also almost tripled. Both prev ...

... March, the price of crude oil has jumped to almost $26 a barrel, up from less than $10 last December and its highest since the Gulf war in 1991. This near-tripling of oil prices evokes scary memories of the 1973 oil shock, when prices quadrupled, and 1979-80, when they also almost tripled. Both prev ...

Inflation in Developing Asia: Demand-Pull or Cost-Push?

... and become an excuse for inaction against inflation. The central objective of this paper is to examine the validity of the cost-push diagnosis of inflation through rigorous empirical analysis. The fundamental question addressed here is whether developing Asia’s inflation is really a case of cost-pus ...

... and become an excuse for inaction against inflation. The central objective of this paper is to examine the validity of the cost-push diagnosis of inflation through rigorous empirical analysis. The fundamental question addressed here is whether developing Asia’s inflation is really a case of cost-pus ...

NBER WORKING PAPER SERIES Christopher J. Erceg Christopher Gust

... tion of consumption under our benchmark calibration (so that putting a larger weight on the former, as occurs with greater openness, increases the interest-sensitivity of the economy). Overall, although openness does exert some effect on the responses of domestic inflation, output, and real interes ...

... tion of consumption under our benchmark calibration (so that putting a larger weight on the former, as occurs with greater openness, increases the interest-sensitivity of the economy). Overall, although openness does exert some effect on the responses of domestic inflation, output, and real interes ...

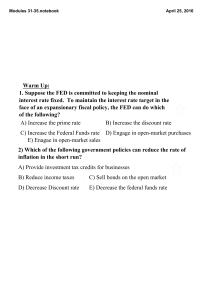

modules 31 to 35

... 1) Draw a short run and long run phillip's curve graph. Label all axes. Label equilibrum at the natural rate of unemployment point A. 2) Label point B. If the government decreases taxes, where is point B in the Phillip's curve graph. 3) Using point A as the starting point, label point C if Oil pr ...

... 1) Draw a short run and long run phillip's curve graph. Label all axes. Label equilibrum at the natural rate of unemployment point A. 2) Label point B. If the government decreases taxes, where is point B in the Phillip's curve graph. 3) Using point A as the starting point, label point C if Oil pr ...

The Effects of Monetary Policy in a Multi-Sector

... Introduction “From Keynes on, there was wide agreement that some imperfections played an essential role in fluctuations. Nominal rigidities, played one explicit and central role in most formalizations. They were crucial to explaining why and how changes in money and other shifts in the demand for go ...

... Introduction “From Keynes on, there was wide agreement that some imperfections played an essential role in fluctuations. Nominal rigidities, played one explicit and central role in most formalizations. They were crucial to explaining why and how changes in money and other shifts in the demand for go ...

Forward Guidance and Macroeconomic Outcomes Since the Financial Crisis ∗ Jeffrey R. Campbell

... economy communicated on announcement days. While further empirical scrutiny of this hypothesis is warranted, at this stage the evidence does not seem to disqualify using a NK framework to analyze the effects of forward guidance. Our ultimate goal is to assess whether the FOMC improved economic perfo ...

... economy communicated on announcement days. While further empirical scrutiny of this hypothesis is warranted, at this stage the evidence does not seem to disqualify using a NK framework to analyze the effects of forward guidance. Our ultimate goal is to assess whether the FOMC improved economic perfo ...

Gerald P. Dwyer Jr.

... officials, regardless of whether they are elected or appointed. In addition, the political process can commit policy in the sense that certain policies become impossible or, to be more precise, high-cost alternatives. Constitutional restrictions are one explicit way of constraining behavior. If effi ...

... officials, regardless of whether they are elected or appointed. In addition, the political process can commit policy in the sense that certain policies become impossible or, to be more precise, high-cost alternatives. Constitutional restrictions are one explicit way of constraining behavior. If effi ...

The Macroeconomic Effects of Large-Scale Asset Purchase Programs

... The form of asset market segmentation that we use in this paper implies that the longterm interest rate matters for aggregate demand distinctly from the expectation of shortterm rates. In this world, even if the short-term rate is constrained by the zero lower bound (ZLB) for a long period of time, ...

... The form of asset market segmentation that we use in this paper implies that the longterm interest rate matters for aggregate demand distinctly from the expectation of shortterm rates. In this world, even if the short-term rate is constrained by the zero lower bound (ZLB) for a long period of time, ...

Monthly Bulletin April 2014

... 2.1 The role of central bank communication There are two important ingredients for the effective steering by a central bank of expectations about future monetary policy: clarity regarding the central bank’s objective, and clarity about the monetary policy strategy it adopts to achieve that objective ...

... 2.1 The role of central bank communication There are two important ingredients for the effective steering by a central bank of expectations about future monetary policy: clarity regarding the central bank’s objective, and clarity about the monetary policy strategy it adopts to achieve that objective ...

3 estimation of the impact of single monetary policy on - Hal-SHS

... January 1st, 1999 is now a key date in modern history. Indeed, it points the transition to the third phase of the Maastricht’s Treaty signed in 1992: founding of the Economic and Monetary Union and creation of a single currency, the Euro, within this zone. The change from national monetary policies ...

... January 1st, 1999 is now a key date in modern history. Indeed, it points the transition to the third phase of the Maastricht’s Treaty signed in 1992: founding of the Economic and Monetary Union and creation of a single currency, the Euro, within this zone. The change from national monetary policies ...

Economics: Explore and Apply 1/e by Ayers and Collinge Chapter 8

... 2. Describe how full-employment output can change. 3. Explain why the price level does not matter in the long run. 4. Interpret and apply the aggregate ...

... 2. Describe how full-employment output can change. 3. Explain why the price level does not matter in the long run. 4. Interpret and apply the aggregate ...

The impact of monetary policy on particular sectors of the economy

... monetary policy decisions are formulated and implemented. Nevertheless, it is possible to identify a set of broad frameworks that have been used by emerging market and other economies. We begin by evaluating these options, in terms of their durability and effectiveness in achieving monetary policy o ...

... monetary policy decisions are formulated and implemented. Nevertheless, it is possible to identify a set of broad frameworks that have been used by emerging market and other economies. We begin by evaluating these options, in terms of their durability and effectiveness in achieving monetary policy o ...

Document

... Result from graph: Increasing MS causes P to rise. How does this work? Short version: At the initial P, an increase in MS causes excess supply of money. People get rid of their excess money by spending it on g&s or by loaning it to others, who spend it. Result: increased demand for goods. But ...

... Result from graph: Increasing MS causes P to rise. How does this work? Short version: At the initial P, an increase in MS causes excess supply of money. People get rid of their excess money by spending it on g&s or by loaning it to others, who spend it. Result: increased demand for goods. But ...

Volume 71 No. 2, June 2008 Contents monetary policy

... Global interest rates fell as the Depression intensified, which meant that New Zealand interest rates also tended to fall. However, as in almost every other country, the inflation rate fell further than nominal interest rates did, lifting the real interest rate. And with banks short of funds and con ...

... Global interest rates fell as the Depression intensified, which meant that New Zealand interest rates also tended to fall. However, as in almost every other country, the inflation rate fell further than nominal interest rates did, lifting the real interest rate. And with banks short of funds and con ...

NBER WORKING PAPER SERIES SETTING THE RECORD STRAIGHT ON

... strategy around the world? Does he believe that the distinction between nominal and real interest rates, which had fallen into virtual disuse in U.S. and U.K. monetary policy discussions until the monetarist counterrevolution, is not a central part of contemporary policymaking? And what does he make ...

... strategy around the world? Does he believe that the distinction between nominal and real interest rates, which had fallen into virtual disuse in U.S. and U.K. monetary policy discussions until the monetarist counterrevolution, is not a central part of contemporary policymaking? And what does he make ...

Working Paper 142

... shift in growth rates for some of the variables, e.g. inflation, money growth and asset price inflation, observed in the "Great Inflation" and "Great Moderation" periods which would otherwise affect the identified shocks.5 Another problem we encountered during the analysis, especially for the specif ...

... shift in growth rates for some of the variables, e.g. inflation, money growth and asset price inflation, observed in the "Great Inflation" and "Great Moderation" periods which would otherwise affect the identified shocks.5 Another problem we encountered during the analysis, especially for the specif ...

NBER WORKING PAPER SERIES THE BARNETT CRITIQUE AFTER THREE DECADES:

... resolve the merits of simple-sum versus superlative indexes of money on the basis of goodnessof-fit criteria or have judged money not to be an important variable when a simple-sum measure alone was used in empirical work, the current paper shows that, with a model fully-specified at the level of ta ...

... resolve the merits of simple-sum versus superlative indexes of money on the basis of goodnessof-fit criteria or have judged money not to be an important variable when a simple-sum measure alone was used in empirical work, the current paper shows that, with a model fully-specified at the level of ta ...

Helicopter Money - Global Interdependence Center

... appropriate policy targets, their re-tooling (or the “de-orthodoxing” of their tool kits) and the recalibration of their reaction functions should all be understood in the context of central banks’ struggles to credibly meet their inflation and (in some cases) employment targets. The evidence is sti ...

... appropriate policy targets, their re-tooling (or the “de-orthodoxing” of their tool kits) and the recalibration of their reaction functions should all be understood in the context of central banks’ struggles to credibly meet their inflation and (in some cases) employment targets. The evidence is sti ...

fiscal policy in an expectations driven liquidity trap

... acknowledges financial support from the Centre for Macroeconomics. ...

... acknowledges financial support from the Centre for Macroeconomics. ...

International Debt Deleveraging Luca Fornaro This draft: November 2013 First draft: November 2012

... Gold Block gave up their exchange rate pegs against gold. Almost 80 years later, history seems to be repeating itself. Following the 2007-2008 turmoil in financial markets several advanced economies experienced an abrupt reduction in capital inflows and embarked in a process of private debt delevera ...

... Gold Block gave up their exchange rate pegs against gold. Almost 80 years later, history seems to be repeating itself. Following the 2007-2008 turmoil in financial markets several advanced economies experienced an abrupt reduction in capital inflows and embarked in a process of private debt delevera ...

15.1 the consumer price index

... The average of the prices paid by urban consumers for a fixed market basket of consumer goods and services was 94.4 percent higher in May 2005 than it was on the average during 19821984. In April 2005, the CPI was 194.6. The average of the prices paid by urban consumers for a fixed market basket of ...

... The average of the prices paid by urban consumers for a fixed market basket of consumer goods and services was 94.4 percent higher in May 2005 than it was on the average during 19821984. In April 2005, the CPI was 194.6. The average of the prices paid by urban consumers for a fixed market basket of ...