Servicing and Foreclosure Fraud

... Servicing and Foreclosure Fraud: Describe Fraud Schemes Involving Default and Loss Mitigation In April 2006, Mrs. Rice filed for bankruptcy claiming the home, co-owned by Mr. Rice and her, as her primary asset. During the pendency of the bankruptcy, the home was foreclosed upon by one of her lender ...

... Servicing and Foreclosure Fraud: Describe Fraud Schemes Involving Default and Loss Mitigation In April 2006, Mrs. Rice filed for bankruptcy claiming the home, co-owned by Mr. Rice and her, as her primary asset. During the pendency of the bankruptcy, the home was foreclosed upon by one of her lender ...

New Trends in Mortgage Fraud - National Crime Prevention Council

... including adjustable interest rates and prepayment penalties, which increased costs for borrowers. ...

... including adjustable interest rates and prepayment penalties, which increased costs for borrowers. ...

Cooking the Books Workbook - Association of Certified Fraud

... • Requiring buyers to deposit extra money in escrow accounts if they refuse to use an affiliated lender. • Coercing buyers into using a designated lender with the threat of withdrawing a seller’s credit toward closing costs. Manufactured Housing Dealer Manufactured housing is now considered real pro ...

... • Requiring buyers to deposit extra money in escrow accounts if they refuse to use an affiliated lender. • Coercing buyers into using a designated lender with the threat of withdrawing a seller’s credit toward closing costs. Manufactured Housing Dealer Manufactured housing is now considered real pro ...

National Foreclosure Settlement

... within the higher credit percentage. A higher property value is also more likely to cause a requested modification to fail the NPV test. The borrower should consider contesting an unreasonably high property valuation and should provide support for a lower value. If yes, Exhibit I applies, and the de ...

... within the higher credit percentage. A higher property value is also more likely to cause a requested modification to fail the NPV test. The borrower should consider contesting an unreasonably high property valuation and should provide support for a lower value. If yes, Exhibit I applies, and the de ...

PPT

... • In Kreglinger v New Patagonia Meat & Cold Storage Co [1914] AC 25 the New Patagonia Meat & Cold Storage Co Ltd carried on a business of preserving meat. Kreglinger carried on business as wool brokers and agreed to lend to New Patagonia the sum of £10,000.00 for a period of 5 years with a proviso t ...

... • In Kreglinger v New Patagonia Meat & Cold Storage Co [1914] AC 25 the New Patagonia Meat & Cold Storage Co Ltd carried on a business of preserving meat. Kreglinger carried on business as wool brokers and agreed to lend to New Patagonia the sum of £10,000.00 for a period of 5 years with a proviso t ...

Eight Steps to Your New Front Door

... appraised value (or sales price if it is lower) of the property. For example, a $100,000 home with an $80,000 mortgage has an LTV of 80 percent. Lock-In Period: The guarantee of an interest rate for a specified period of time by a lender, including loan term and points, if any, to be paid at closing ...

... appraised value (or sales price if it is lower) of the property. For example, a $100,000 home with an $80,000 mortgage has an LTV of 80 percent. Lock-In Period: The guarantee of an interest rate for a specified period of time by a lender, including loan term and points, if any, to be paid at closing ...

Mortgage Loans

... Annual Percentage Rate (APR) — The cost of credit expressed as a yearly rate. This includes any finance charges and additional fees. Application Fee — A fee to cover the costs of processing the application, documentation and verification. Arbitration Clause — A provision in the contract that states ...

... Annual Percentage Rate (APR) — The cost of credit expressed as a yearly rate. This includes any finance charges and additional fees. Application Fee — A fee to cover the costs of processing the application, documentation and verification. Arbitration Clause — A provision in the contract that states ...

The Renewable Heat Incentive: a reformed and refocused scheme

... As with solar panels, lenders will want to ensure that leases meet their requirements; in particular lenders will want to know that no security of tenure arises. Since there is no standard form lease these are likely to be considered on a case by case basis at present, which is time consuming and re ...

... As with solar panels, lenders will want to ensure that leases meet their requirements; in particular lenders will want to know that no security of tenure arises. Since there is no standard form lease these are likely to be considered on a case by case basis at present, which is time consuming and re ...

6218 - Fannie Mae

... shall not commingle its assets or funds with those of any other Person unless such assets or funds can easily be segregated and identified in the ordinary course of business from those of any other Person; ...

... shall not commingle its assets or funds with those of any other Person unless such assets or funds can easily be segregated and identified in the ordinary course of business from those of any other Person; ...

REO Resources - Florida Realtors

... clear the inventory from their books. Due to this pricing, many properties receive multiple offers before it is even placed in the MLS, so it is very possible that the offer was presented, but not accepted. It is recommended you counsel your buyer about your opinion of the actual value of the proper ...

... clear the inventory from their books. Due to this pricing, many properties receive multiple offers before it is even placed in the MLS, so it is very possible that the offer was presented, but not accepted. It is recommended you counsel your buyer about your opinion of the actual value of the proper ...

SUBCHAPTER 03M – MORTGAGE LENDING SECTION .0100

... for corporate licensees, the identity of the licensee's owners, officers, directors, qualifying individual, branch manager(s), or control persons. "Material" when used in connection with facts or information provided to a borrower, means facts or information that a reasonable person knows, or should ...

... for corporate licensees, the identity of the licensee's owners, officers, directors, qualifying individual, branch manager(s), or control persons. "Material" when used in connection with facts or information provided to a borrower, means facts or information that a reasonable person knows, or should ...

Frequently Asked Questions

... What happens in the event of the termination of my employment with the College for any other reason than retirement? Your note(s) shall, at the option of the College, immediately become due and payable after notice is provided to you. (Termination does not include a leave of absence taken with the a ...

... What happens in the event of the termination of my employment with the College for any other reason than retirement? Your note(s) shall, at the option of the College, immediately become due and payable after notice is provided to you. (Termination does not include a leave of absence taken with the a ...

Discharge of a guarantee

... guarantor’s prior consent to such dealings between the lender and the borrower. So long as the wording of these clauses covers the exact dealings which occur, the guarantee will remain valid. But, in practice, lenders err on the side of caution and obtain the guarantor’s express consent at the time ...

... guarantor’s prior consent to such dealings between the lender and the borrower. So long as the wording of these clauses covers the exact dealings which occur, the guarantee will remain valid. But, in practice, lenders err on the side of caution and obtain the guarantor’s express consent at the time ...

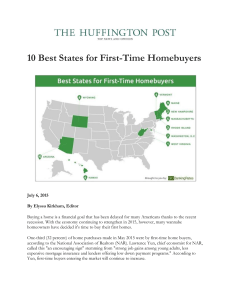

10 Best States for First-Time Homebuyers

... Rhode Island had the largest amount of growth in first-time home buyers; its rate of this type of borrower nearly doubled -- up by 97.1 percent -- from 2003 to 2013. Foreclosures are also fairly low at 0.06 percent, only slightly higher than New Hampshire's 0.05 percent. Rhode Island also has a wide ...

... Rhode Island had the largest amount of growth in first-time home buyers; its rate of this type of borrower nearly doubled -- up by 97.1 percent -- from 2003 to 2013. Foreclosures are also fairly low at 0.06 percent, only slightly higher than New Hampshire's 0.05 percent. Rhode Island also has a wide ...

25 KB - National Homelessness Advice Service

... targeted funding to the independent advice sector, Preventing Repossession Funding provided directly to local authorities, encouraging lender forbearance options and enhanced the Homelessness Code of Guidance ( to ensure local authorities did not automatically find households intentionally homeless ...

... targeted funding to the independent advice sector, Preventing Repossession Funding provided directly to local authorities, encouraging lender forbearance options and enhanced the Homelessness Code of Guidance ( to ensure local authorities did not automatically find households intentionally homeless ...

Reverse Mortgage Tax Exemption Affidavit

... NOTE: All mortgagors must be 60 years of age. If the property is held by senior over 60 as to a life estate interest only and the remainder interest(s) are held by anyone under age 60, the mortgage tax must be paid. However in 2007 the Tax Department confirmed that if the loan was a federal reverse ...

... NOTE: All mortgagors must be 60 years of age. If the property is held by senior over 60 as to a life estate interest only and the remainder interest(s) are held by anyone under age 60, the mortgage tax must be paid. However in 2007 the Tax Department confirmed that if the loan was a federal reverse ...

2005 Survey - Freddie Mac Home

... – Do not feel entirely comfortable talking – Do not find banks intimidating to their banks about personal finances – Strongly agree that their banks treat – Find prioritizing their bills difficult (and ...

... – Do not feel entirely comfortable talking – Do not find banks intimidating to their banks about personal finances – Strongly agree that their banks treat – Find prioritizing their bills difficult (and ...

Money Adviser Pack Update – Summary of main changes

... order issued against their property are not excluded from HMS, nor do they need agreement from their charging order creditor to enter the scheme. Where payments are being made in respect of the charging order, these should be reviewed as part of the holistic money advice offered and factored into th ...

... order issued against their property are not excluded from HMS, nor do they need agreement from their charging order creditor to enter the scheme. Where payments are being made in respect of the charging order, these should be reviewed as part of the holistic money advice offered and factored into th ...

PDF - Allen Tate Mortgage

... A report from a credit bureau containing detailed information about an individual’s credit history and activity. Credit score A numerical score, based on an individual’s credit history, that reflects a borrower’s credit worthiness. The most widely used credit score is called FICO (Fair Isaac Co.) De ...

... A report from a credit bureau containing detailed information about an individual’s credit history and activity. Credit score A numerical score, based on an individual’s credit history, that reflects a borrower’s credit worthiness. The most widely used credit score is called FICO (Fair Isaac Co.) De ...

Common clauses and stipulations in loan agreements

... of the clauses as described below, the parties should check the wording of each particular clause before concluding a contract. In addition, the clauses may lead to different legal consequences under each underlying jurisdiction. The cross-collateral clause. Under a cross-collateral clause, the lend ...

... of the clauses as described below, the parties should check the wording of each particular clause before concluding a contract. In addition, the clauses may lead to different legal consequences under each underlying jurisdiction. The cross-collateral clause. Under a cross-collateral clause, the lend ...

The Freedom Recovery Plan

... The Plan is designed to promote accelerated settlement, between borrower and lender, of impaired mortgages (as such impairment is described below). Settlements under the Plan would involve homeowner/borrowers, with impaired mortgage loans, voluntarily surrendering to their mortgagees the deeds to th ...

... The Plan is designed to promote accelerated settlement, between borrower and lender, of impaired mortgages (as such impairment is described below). Settlements under the Plan would involve homeowner/borrowers, with impaired mortgage loans, voluntarily surrendering to their mortgagees the deeds to th ...

a predator in america`s midst: a look at predatory lending

... A subprime mortgage loan is a risk, both for the lender and the borrower. The borrower risks the inability to pay every month, due to the terms of the subprime mortgage, while the lender risks losing a substantial amount of money if he must foreclose on a property where the amount owed will be great ...

... A subprime mortgage loan is a risk, both for the lender and the borrower. The borrower risks the inability to pay every month, due to the terms of the subprime mortgage, while the lender risks losing a substantial amount of money if he must foreclose on a property where the amount owed will be great ...

CEMA LOAN FAQ - Adams Law Group LLC

... 192,153.35. So that's why the shortcut works, because the more direct way to derive the tax savings is with the pub, which is referred to as the old money. Question: How does the process work exactly? Answer: The mortgage tax is asseessed at the time a mortgage is recorded. In most refinance transac ...

... 192,153.35. So that's why the shortcut works, because the more direct way to derive the tax savings is with the pub, which is referred to as the old money. Question: How does the process work exactly? Answer: The mortgage tax is asseessed at the time a mortgage is recorded. In most refinance transac ...

Why you need to shop around for a mortgage

... The survey found that 47 per cent of borrowers who purchased a home in 2013 considered only one mortgage lender. The number was slightly lower, at 44.5 per cent, for firsttime homebuyers. ...

... The survey found that 47 per cent of borrowers who purchased a home in 2013 considered only one mortgage lender. The number was slightly lower, at 44.5 per cent, for firsttime homebuyers. ...

Complete Transcript

... that a bank which had lent them money to buy a property for them to live in could take possession of it the next day". And there is a very famous statement about this in the case of Four Maids Ltd v Dudley Marshall Properties as per the slide. "The mortgagee may go into possession before the ink is ...

... that a bank which had lent them money to buy a property for them to live in could take possession of it the next day". And there is a very famous statement about this in the case of Four Maids Ltd v Dudley Marshall Properties as per the slide. "The mortgagee may go into possession before the ink is ...

Foreclosure

Foreclosure is a legal process in which a lender attempts to recover the balance of a loan from a borrower who has stopped making payments to the lender by forcing the sale of the asset used as the collateral for the loan.Formally, a mortgage lender (mortgagee), or other lienholder, obtains a termination of a mortgage borrower (mortgagor)'s equitable right of redemption, either by court order or by operation of law (after following a specific statutory procedure).Usually a lender obtains a security interest from a borrower who mortgages or pledges an asset like a house to secure the loan. If the borrower defaults and the lender tries to repossess the property, courts of equity can grant the borrower the equitable right of redemption if the borrower repays the debt. While this equitable right exists, it is a cloud on title and the lender cannot be sure that they can successfully repossess the property. Therefore, through the process of foreclosure, the lender seeks to foreclose (in plain English, immediately terminate) the equitable right of redemption and take both legal and equitable title to the property in fee simple. Other lien holders can also foreclose the owner's right of redemption for other debts, such as for overdue taxes, unpaid contractors' bills or overdue homeowners' association dues or assessments.The foreclosure process as applied to residential mortgage loans is a bank or other secured creditor selling or repossessing a parcel of real property after the owner has failed to comply with an agreement between the lender and borrower called a ""mortgage"" or ""deed of trust."" Commonly, the violation of the mortgage is a default in payment of a promissory note, secured by a lien on the property. When the process is complete, the lender can sell the property and keep the proceeds to pay off its mortgage and any legal costs, and it is typically said that ""the lender has foreclosed its mortgage or lien."" If the promissory note was made with a recourse clause then if the sale does not bring enough to pay the existing balance of principal and fees the mortgagee can file a claim for a deficiency judgment. In many states in the United States, items included to calculate the amount of a deficiency judgment include the loan principal, accrued interest and attorney fees less the amount the lender bid at the foreclosure sale.