CPA PassMaster Questions–Auditing 4 Export Date: 10/30/08

... Choice "a" is incorrect. If fictitious transactions in the revenue cycle are recorded, then the impact on revenues and receivables would be the same; either both would be overstated (the most likely case) or both would be understated. Choice "b" is incorrect. Even the lack of effective internal cont ...

... Choice "a" is incorrect. If fictitious transactions in the revenue cycle are recorded, then the impact on revenues and receivables would be the same; either both would be overstated (the most likely case) or both would be understated. Choice "b" is incorrect. Even the lack of effective internal cont ...

Revised Guidance Statement GS 009: Auditing SMSFs

... The SISA, subsection 35C(1), requires SMSFs to be audited each financial year by an approved SMSF auditor (the auditor),4 who is required to complete both the financial audit and the compliance engagement and sign the auditor’s report before a SMSF may submit its Annual Return.5 The auditor reports ...

... The SISA, subsection 35C(1), requires SMSFs to be audited each financial year by an approved SMSF auditor (the auditor),4 who is required to complete both the financial audit and the compliance engagement and sign the auditor’s report before a SMSF may submit its Annual Return.5 The auditor reports ...

APPTICATION OF THE AUDIT PROCESS TO OTHER CYCTES

... transactions for the acquisition and payment cycle receive a considerable amount of attention, especially when the client has effective internal controls. Tests of controls and substantive tests of transactions for the acquisition and payment cycle are divided into two broad areas: 1. Tests of acqui ...

... transactions for the acquisition and payment cycle receive a considerable amount of attention, especially when the client has effective internal controls. Tests of controls and substantive tests of transactions for the acquisition and payment cycle are divided into two broad areas: 1. Tests of acqui ...

Auditing for Fraud Detection - Professional Education Services

... Financial auditors assess control risk in general and specific terms to design other audit procedures, while fraud examiners habitually "think like a crook'' to imagine ways controls could be subverted for fraudulent purposes. Financial auditors use a concept of materiality (dollar size big enough t ...

... Financial auditors assess control risk in general and specific terms to design other audit procedures, while fraud examiners habitually "think like a crook'' to imagine ways controls could be subverted for fraudulent purposes. Financial auditors use a concept of materiality (dollar size big enough t ...

Substantive Tests of Transactions and Balances

... effective means of auditing the financial report of a small business. It is especially efficient if the auditor designs effective analytical tests for those specific audit objectives, such as statement of financial performance, account classification and those related to the completeness assertion, ...

... effective means of auditing the financial report of a small business. It is especially efficient if the auditor designs effective analytical tests for those specific audit objectives, such as statement of financial performance, account classification and those related to the completeness assertion, ...

User guide to Standing Direction 1

... Certification takes place annually from July to September each year. An overview of the annual certification process can be found within this section. ...

... Certification takes place annually from July to September each year. An overview of the annual certification process can be found within this section. ...

ORRS 2011 (Text)

... Members can affect the timing of the publication of data which can have a knock-on impact on the ability of Members to use the data. Requirement: Members are required to provide data that meets the requirements of the ORX data quality dimensions 1-5 plus accuracy. Members are expected to conduct an ...

... Members can affect the timing of the publication of data which can have a knock-on impact on the ability of Members to use the data. Requirement: Members are required to provide data that meets the requirements of the ORX data quality dimensions 1-5 plus accuracy. Members are expected to conduct an ...

Approved form - Australian Prudential Regulation Authority

... My audit has been conducted in accordance with Australian Auditing Standards5. These Standards require that I comply with relevant ethical requirements relating to audit engagements and plan and perform the audit to obtain reasonable assurance as to whether the financial statements are free of mater ...

... My audit has been conducted in accordance with Australian Auditing Standards5. These Standards require that I comply with relevant ethical requirements relating to audit engagements and plan and perform the audit to obtain reasonable assurance as to whether the financial statements are free of mater ...

Blanchard_Reinsurance_2012.xlsx

... 1. There are no separate written or oral agreements between the reporting entity and assuming reinsurer 2. Every reinsurance contract is documented for which risk transfer is not reasonably self-evident and details the transactions economic intent 3. Reporting entity complies with all requirements s ...

... 1. There are no separate written or oral agreements between the reporting entity and assuming reinsurer 2. Every reinsurance contract is documented for which risk transfer is not reasonably self-evident and details the transactions economic intent 3. Reporting entity complies with all requirements s ...

The Evolution of the Financial Intermediary Controls and

... Some omnibus accounts may contain only a specific type of subaccount. For example, an omnibus account may be opened to aggregate all individual investor accounts that have the same dividend reinvestment option, or may be used by the intermediary to manage different lines of business. In the retireme ...

... Some omnibus accounts may contain only a specific type of subaccount. For example, an omnibus account may be opened to aggregate all individual investor accounts that have the same dividend reinvestment option, or may be used by the intermediary to manage different lines of business. In the retireme ...

ISA 520 Analytical procedures

... margin percentages as a means of confirming a revenue figure may provide less ...

... margin percentages as a means of confirming a revenue figure may provide less ...

A GUIDE TO STATUTORY AUDIT PROCEDURES ON EXPECTED

... the assessment of the design and operating effectiveness of the relevant controls on the accounting estimate process, ...

... the assessment of the design and operating effectiveness of the relevant controls on the accounting estimate process, ...

Implementation Tool for Auditors

... perceived opportunities to commit fraud may be common across industries (e.g., engaging in side agreements, barter transactions, subjective estimates), it is also important to consider entity-specific perceived opportunities (e.g., strength of control environment, payment methods (e.g., cash payment ...

... perceived opportunities to commit fraud may be common across industries (e.g., engaging in side agreements, barter transactions, subjective estimates), it is also important to consider entity-specific perceived opportunities (e.g., strength of control environment, payment methods (e.g., cash payment ...

Breaking the Cycle of Fraud - Financial Executives International

... Finally, this report compiles and analyzes survey results conducted of financial executives, managers, and staff to identify and evaluate the measures being followed by their companies to mitigate the risk of fraud. In addition, participants provided recommendations to improve fraud avoidance and d ...

... Finally, this report compiles and analyzes survey results conducted of financial executives, managers, and staff to identify and evaluate the measures being followed by their companies to mitigate the risk of fraud. In addition, participants provided recommendations to improve fraud avoidance and d ...

EFFECTS OF INTERNAL CONTROLS ON REVENUE COLLECTION

... increased collected revenue. The research was conducted using both qualitative and quantitative approaches. Questionnaires were used on a population of 38 respondents in gathering primary data for the study. The data collected was then analyzed and findings have revealed that the five components of ...

... increased collected revenue. The research was conducted using both qualitative and quantitative approaches. Questionnaires were used on a population of 38 respondents in gathering primary data for the study. The data collected was then analyzed and findings have revealed that the five components of ...

table of contents - Caritas University

... ‘system’ of internal control extends beyond those matters which relate directly to the functions of the accounting and financial department. ...

... ‘system’ of internal control extends beyond those matters which relate directly to the functions of the accounting and financial department. ...

FREE Sample Here

... 33. An auditor discovers a likely fraud during an audit but concludes that the effect of the fraud is not sufficiently material to affect the audit opinion. The auditor should A. Disclose the fraud to the appropriate level of the client's management B. Disclose the fraud to appropriate authorities e ...

... 33. An auditor discovers a likely fraud during an audit but concludes that the effect of the fraud is not sufficiently material to affect the audit opinion. The auditor should A. Disclose the fraud to the appropriate level of the client's management B. Disclose the fraud to appropriate authorities e ...

documentation of the entity and its environment

... Are there estimates in the financial statements that are significant? ___ Yes ___ No If yes, identify the estimates and describe the process by which estimates are made: ________________________________________________________________________ _________________________________________________________ ...

... Are there estimates in the financial statements that are significant? ___ Yes ___ No If yes, identify the estimates and describe the process by which estimates are made: ________________________________________________________________________ _________________________________________________________ ...

Comprehensive Case A.1 – Enron

... estimate, the estimate can be considered more reliable and competent. Although this valuation procedure can be costly to the client, the reliability of the estimate is far more valuable to users that are dependent upon an unbiased and objective MTM estimate. An example of a control procedure designe ...

... estimate, the estimate can be considered more reliable and competent. Although this valuation procedure can be costly to the client, the reliability of the estimate is far more valuable to users that are dependent upon an unbiased and objective MTM estimate. An example of a control procedure designe ...

Leading Practice Examples of Audit Committee Reporting

... differences, country-specific regulations, and distance between international locations and corporate headquarters, the inherent risk level is increased. Audit Summary This review focused on: • Understanding policies and procedures in-place related to in-scope processes; • Evaluating the control env ...

... differences, country-specific regulations, and distance between international locations and corporate headquarters, the inherent risk level is increased. Audit Summary This review focused on: • Understanding policies and procedures in-place related to in-scope processes; • Evaluating the control env ...

Assignment 1 is compulsory and due

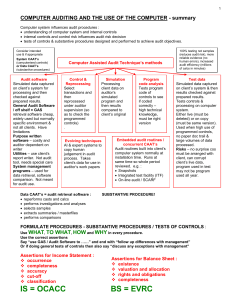

... and follow up differences with management GAS substantive procedures purchases (BS) – use audit software to : extract a sample of purchase invoices and inspect that they are made out to the entity and that the items purchases appear on the entity’s inventory list and aren’t fictitious extract a ...

... and follow up differences with management GAS substantive procedures purchases (BS) – use audit software to : extract a sample of purchase invoices and inspect that they are made out to the entity and that the items purchases appear on the entity’s inventory list and aren’t fictitious extract a ...

internal-auditing-instructional-material

... 3. Either the auditors’ report on the entity’s financial statement or a separate report shall contain a statement of positive assurance on those items of compliance tested and negative assurance on those items not tested. It shall also include material instances of non compliance and instances or in ...

... 3. Either the auditors’ report on the entity’s financial statement or a separate report shall contain a statement of positive assurance on those items of compliance tested and negative assurance on those items not tested. It shall also include material instances of non compliance and instances or in ...

Answers

... framework to be applied in the preparation of the financial statements is acceptable. In considering this the auditor should assess the nature of the entity, the nature and purpose of the financial statements and whether law or regulations prescribes the applicable reporting framework. In addition t ...

... framework to be applied in the preparation of the financial statements is acceptable. In considering this the auditor should assess the nature of the entity, the nature and purpose of the financial statements and whether law or regulations prescribes the applicable reporting framework. In addition t ...

download

... examples of control activities contained in this guide are not presented as all-inclusive or exhaustive of all the specific controls appropriate in each department or unit. Over time, controls may be expected to change to reflect changes in our operating environment. An effective control system prov ...

... examples of control activities contained in this guide are not presented as all-inclusive or exhaustive of all the specific controls appropriate in each department or unit. Over time, controls may be expected to change to reflect changes in our operating environment. An effective control system prov ...