1) When those most likely to produce the outcome insured against

... Question Status: Previous Edition Because young males have a much higher rate of accidents on average than young females, automobile insurers will be likely to charge young males higher insurance premiums than young females, all else equal. encourage young males to purchase collision insurance polic ...

... Question Status: Previous Edition Because young males have a much higher rate of accidents on average than young females, automobile insurers will be likely to charge young males higher insurance premiums than young females, all else equal. encourage young males to purchase collision insurance polic ...

Africa insurance trends

... catastrophes that are creating challenges but also new opportunities for sophisticated underwriting models and risk transfer; 4. The rising economic significance of emerging high growth economies like Nigeria and Kenya. South Africa’s, economy on the other hand, is stagnating at a time when it shoul ...

... catastrophes that are creating challenges but also new opportunities for sophisticated underwriting models and risk transfer; 4. The rising economic significance of emerging high growth economies like Nigeria and Kenya. South Africa’s, economy on the other hand, is stagnating at a time when it shoul ...

DETERMINANTS OF THE DEMAND FOR LIFE INSURANCE

... Interesting is the fact that nearly all authors, who investigated the life insurance demand, related to the theoretical framework developed by Yaari (1965) as to initial point. Rudolf Enz (2000) argued in his paper that models with constant income elasticity of life insurance demand are artificial ...

... Interesting is the fact that nearly all authors, who investigated the life insurance demand, related to the theoretical framework developed by Yaari (1965) as to initial point. Rudolf Enz (2000) argued in his paper that models with constant income elasticity of life insurance demand are artificial ...

RELATIONSHIP BETWEEN MACROECONOMIC VARIABLES AND

... The purpose of this study was to determine the relationship between macroeconomic variables and financial performance of Insurance Companies in Kenya. The financial performance measures of companies in Insurance industry used was the Return on Assets (ROA) which was regressed against the macroeconom ...

... The purpose of this study was to determine the relationship between macroeconomic variables and financial performance of Insurance Companies in Kenya. The financial performance measures of companies in Insurance industry used was the Return on Assets (ROA) which was regressed against the macroeconom ...

F2017C00060 F2017C00060

... As an exception to the requirements in AASB 9, an insurer need not separate, and measure at fair value, a policyholder’s option to surrender an insurance contract for a fixed amount (or for an amount based on a fixed amount and an interest rate), even if the exercise price differs from the carrying ...

... As an exception to the requirements in AASB 9, an insurer need not separate, and measure at fair value, a policyholder’s option to surrender an insurance contract for a fixed amount (or for an amount based on a fixed amount and an interest rate), even if the exercise price differs from the carrying ...

Islamic Micro-Insurance * Micro-Takaful: Basic Exposition

... entrepreneurs to undertake high return activities, of course with higher risk than they would be in the absence of insurance. Risk and Insurance: Risk and uncertainty are fundamental facts of life. All human activities are subject to risk, which may lead to financial or physical losses to him. Every ...

... entrepreneurs to undertake high return activities, of course with higher risk than they would be in the absence of insurance. Risk and Insurance: Risk and uncertainty are fundamental facts of life. All human activities are subject to risk, which may lead to financial or physical losses to him. Every ...

chapter - ii life insurance - basics and global trends

... have unlimited insurable interest in their own lives. A husband and wife have unlimited insurable interest on each other’s lives. Similarly, insurable interest can be present in close family relationships such as parents – children. Beyond such close relationships, insurable interest exists in finan ...

... have unlimited insurable interest in their own lives. A husband and wife have unlimited insurable interest on each other’s lives. Similarly, insurable interest can be present in close family relationships such as parents – children. Beyond such close relationships, insurable interest exists in finan ...

The Cost of Financial Frictions for Life Insurers

... (i.e., embedded put options) turned out to be unprofitable. Second, statutory reserve regulation in the United States allowed life insurers to record far less than a dollar of reserve per dollar of future insurance liability around December 2008. This allowed life insurers to generate accounting profi ...

... (i.e., embedded put options) turned out to be unprofitable. Second, statutory reserve regulation in the United States allowed life insurers to record far less than a dollar of reserve per dollar of future insurance liability around December 2008. This allowed life insurers to generate accounting profi ...

Recovery and Resolution Planning for Systemically Important Insurers:

... market and the ability of third parties to obtain insurance in a timely fashion and on reasonable terms. For example, certain commercial insurance lines require specialised underwriting skills and are dominated by a small number of firms with high market shares. If one of those firms were to fail an ...

... market and the ability of third parties to obtain insurance in a timely fashion and on reasonable terms. For example, certain commercial insurance lines require specialised underwriting skills and are dominated by a small number of firms with high market shares. If one of those firms were to fail an ...

Assignment 10

... • Reinsurance – “insurance for insurers” • Reinsurance is the transfer from one insurer (primary insurer) to another (the reinsurer) of some of the financial consequences covered by the primary insured’s policies • Transfer of liability – the reinsured, the ceding company, the cedent, the direct ins ...

... • Reinsurance – “insurance for insurers” • Reinsurance is the transfer from one insurer (primary insurer) to another (the reinsurer) of some of the financial consequences covered by the primary insured’s policies • Transfer of liability – the reinsured, the ceding company, the cedent, the direct ins ...

Nr. 111 The Differential Factors Influencing Saving through Life

... long term saving, but also can pay the benefits covering losses under contract resulting from personal risks’ happening. In economic transition towards market orientation, putting emphasis on saving through life insurers in China has a more realistic implication. China need a great amount of constru ...

... long term saving, but also can pay the benefits covering losses under contract resulting from personal risks’ happening. In economic transition towards market orientation, putting emphasis on saving through life insurers in China has a more realistic implication. China need a great amount of constru ...

the relationship between insurance industry and banking sector in

... observed to increase at different levels lately. At the capital level, mutual holding between the banks and insurance companies, especially the establishment of bankowned insurance companies, are becoming prevalent. At the business level, based on the development of bancassurance, the expansion of c ...

... observed to increase at different levels lately. At the capital level, mutual holding between the banks and insurance companies, especially the establishment of bankowned insurance companies, are becoming prevalent. At the business level, based on the development of bancassurance, the expansion of c ...

Corporate Risks and Property Insurance: Evidence From the

... corporate spending on property insurance lines such as coverage on physical assets (PBOC, 1998).2 As at the end of 1998, 25 insurance companies were operating in China, of which four were state-owned insurers, nine were stock companies, three were international-Chinese joint ventures, and nine were ...

... corporate spending on property insurance lines such as coverage on physical assets (PBOC, 1998).2 As at the end of 1998, 25 insurance companies were operating in China, of which four were state-owned insurers, nine were stock companies, three were international-Chinese joint ventures, and nine were ...

What is Lender`s Mortgage insurance (“LMI”)

... ICA believes the recommendations of the HIH Royal Commission as they relate to taxes on insurance, should be implemented by all Australian Governments. For the first home buyer, implementation of these proposals will significantly reduce ongoing costs associated with first homeownership while also h ...

... ICA believes the recommendations of the HIH Royal Commission as they relate to taxes on insurance, should be implemented by all Australian Governments. For the first home buyer, implementation of these proposals will significantly reduce ongoing costs associated with first homeownership while also h ...

Insurance market report 2015

... While growth in group life insurance in the occupational pensions sector came mostly from savings premiums used for topping up retirement assets, growth in both individual life insurance sectors can be attri buted to product innovations. In general, however, the decline in market interest rates to ...

... While growth in group life insurance in the occupational pensions sector came mostly from savings premiums used for topping up retirement assets, growth in both individual life insurance sectors can be attri buted to product innovations. In general, however, the decline in market interest rates to ...

The Analysis of Formation Mechanism of Regional

... Because of the different natural and geographical conditions among regions, the types and risk loss displayed by the agricultural risk among regions vary greatly, and especially the natural risk and its loss degree have distinct regional features. China has a vast area of agricultural production, ma ...

... Because of the different natural and geographical conditions among regions, the types and risk loss displayed by the agricultural risk among regions vary greatly, and especially the natural risk and its loss degree have distinct regional features. China has a vast area of agricultural production, ma ...

terrorism risk insurance act of 2002: a primer

... TRIA set up a risk-sharing partnership between the federal government and the insurance industry. Insurers are required to offer terrorism coverage for voluntary purchase by businesses. In turn, the federal government agrees to initially absorb a portion of the cost of large attacks. It may recoup i ...

... TRIA set up a risk-sharing partnership between the federal government and the insurance industry. Insurers are required to offer terrorism coverage for voluntary purchase by businesses. In turn, the federal government agrees to initially absorb a portion of the cost of large attacks. It may recoup i ...

Report

... function more smoothly by enabling individuals and businesses to take more risk However, it is difficult to argue that insurance is as important as banking, the payments system, or the settlement system Various insurance markets regularly experience availability crises without significantly a ...

... function more smoothly by enabling individuals and businesses to take more risk However, it is difficult to argue that insurance is as important as banking, the payments system, or the settlement system Various insurance markets regularly experience availability crises without significantly a ...

Evaluation of Markets for Financial Responsibility Instruments and

... members also put their capital at risk for the higher frequency primary risk layers, where the risks assumed are most influenced by operating risk controls and procedures. In so doing, RRGs create a layered risk management-based insurance instrument, whereby insureds falling within the RRG are motiv ...

... members also put their capital at risk for the higher frequency primary risk layers, where the risks assumed are most influenced by operating risk controls and procedures. In so doing, RRGs create a layered risk management-based insurance instrument, whereby insureds falling within the RRG are motiv ...

PDF

... losses is captured by a single correlation coefficient. This parameter is crucial for modeling the systemic risk component. Third, we extend the model from a single market to a multi-market setting, where each market represents a different region. The contribution of this paper to the existing liter ...

... losses is captured by a single correlation coefficient. This parameter is crucial for modeling the systemic risk component. Third, we extend the model from a single market to a multi-market setting, where each market represents a different region. The contribution of this paper to the existing liter ...

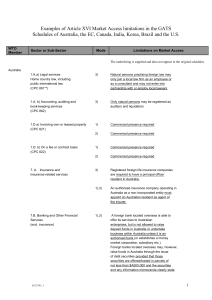

Examples of Article XVI Market Access limitations in GATS Schedules

... A foreign bank located overseas is able to offer its services to Australian enterprises, but is not allowed to raise deposit funds in Australia or undertake business within Australia unless it is an authorised bank (or establishes a money market corporation, subsidiary etc.). Foreign banks located o ...

... A foreign bank located overseas is able to offer its services to Australian enterprises, but is not allowed to raise deposit funds in Australia or undertake business within Australia unless it is an authorised bank (or establishes a money market corporation, subsidiary etc.). Foreign banks located o ...

Review of Lithuania`s Insurance Market

... the market, which does not ensure the interests of policyholders (credit borrowers) and distorts their expectations. The Supervision Service believes that such insurance contracts should be concluded for such a period as to allow to assess the insurance risk and to set the terms and conditions of th ...

... the market, which does not ensure the interests of policyholders (credit borrowers) and distorts their expectations. The Supervision Service believes that such insurance contracts should be concluded for such a period as to allow to assess the insurance risk and to set the terms and conditions of th ...

393 KB - Financial System Inquiry

... financial system A fundamental role of financial institutions and markets is to assist individuals and corporations to manage risk. Financial entities also mobilise savings and allocate them across the spectrum of investment opportunities. The general insurance industry plays a role in this regard b ...

... financial system A fundamental role of financial institutions and markets is to assist individuals and corporations to manage risk. Financial entities also mobilise savings and allocate them across the spectrum of investment opportunities. The general insurance industry plays a role in this regard b ...

Catastrophe Insurance, Capital Markets and

... Principal justification or not, it is clear that private insurance markets are currently having a difficult time providing coverage for catastrophe risk. In California, for example, where earthquake coverage must be offered as an option on homeowner’s policies, companies representing 93% of the home ...

... Principal justification or not, it is clear that private insurance markets are currently having a difficult time providing coverage for catastrophe risk. In California, for example, where earthquake coverage must be offered as an option on homeowner’s policies, companies representing 93% of the home ...

Download Full Article

... community pooling of informal insurance contributions to cover burial costs. Community-based insurance mechanisms surmount the problems of transactions costs and lack of legally enforceable contracts through personal relationships and piggybacking on traditional small-scale financial collection mech ...

... community pooling of informal insurance contributions to cover burial costs. Community-based insurance mechanisms surmount the problems of transactions costs and lack of legally enforceable contracts through personal relationships and piggybacking on traditional small-scale financial collection mech ...