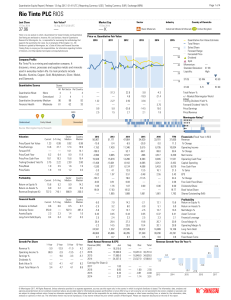

Rio Tinto PLC RIOS

... estimate of the per share dollar amount that a company’s equity is worth today. Morningstar calculates the Quantitative Fair Value Estimate using a statistical model derived from the Fair Value Estimate Morningstar’s equity analysts assign to companies. Please go to http://global.morningstar.com/equ ...

... estimate of the per share dollar amount that a company’s equity is worth today. Morningstar calculates the Quantitative Fair Value Estimate using a statistical model derived from the Fair Value Estimate Morningstar’s equity analysts assign to companies. Please go to http://global.morningstar.com/equ ...

Credit Scores, Reports, and Getting Ahead in

... scores. There is no public data available, for instance, that speaks to the optimal level of mortgage price fluctuation across different levels of risk. Put differently, the price-point where higher prices for mortgage borrowers with low credit scores becomes pricegouging rather than just cost-cover ...

... scores. There is no public data available, for instance, that speaks to the optimal level of mortgage price fluctuation across different levels of risk. Put differently, the price-point where higher prices for mortgage borrowers with low credit scores becomes pricegouging rather than just cost-cover ...

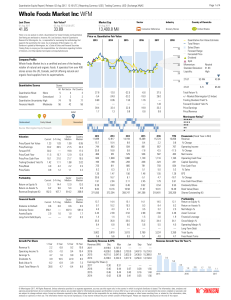

Whole Foods Market Inc WFM

... estimate of the per share dollar amount that a company’s equity is worth today. Morningstar calculates the Quantitative Fair Value Estimate using a statistical model derived from the Fair Value Estimate Morningstar’s equity analysts assign to companies. Please go to http://global.morningstar.com/equ ...

... estimate of the per share dollar amount that a company’s equity is worth today. Morningstar calculates the Quantitative Fair Value Estimate using a statistical model derived from the Fair Value Estimate Morningstar’s equity analysts assign to companies. Please go to http://global.morningstar.com/equ ...

Privatizing Fannie and Freddie: Be Careful What

... level required for SIFIs. Their line of credit with Treasury would provide about 5% capitalization and their current guarantee fee of 63 basis points would provide 3%, assuming the 10% after-tax return on equity that SIFIs are earning today. To cover the cost of the additional 2% capital needed, the ...

... level required for SIFIs. Their line of credit with Treasury would provide about 5% capitalization and their current guarantee fee of 63 basis points would provide 3%, assuming the 10% after-tax return on equity that SIFIs are earning today. To cover the cost of the additional 2% capital needed, the ...

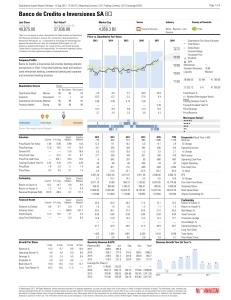

Banco de Credito e Inversiones SA BCI

... estimate of the per share dollar amount that a company’s equity is worth today. Morningstar calculates the Quantitative Fair Value Estimate using a statistical model derived from the Fair Value Estimate Morningstar’s equity analysts assign to companies. Please go to http://global.morningstar.com/equ ...

... estimate of the per share dollar amount that a company’s equity is worth today. Morningstar calculates the Quantitative Fair Value Estimate using a statistical model derived from the Fair Value Estimate Morningstar’s equity analysts assign to companies. Please go to http://global.morningstar.com/equ ...

China Marine Food Group Ltd CMFO

... estimate of the per share dollar amount that a company’s equity is worth today. Morningstar calculates the Quantitative Fair Value Estimate using a statistical model derived from the Fair Value Estimate Morningstar’s equity analysts assign to companies. Please go to http://global.morningstar.com/equ ...

... estimate of the per share dollar amount that a company’s equity is worth today. Morningstar calculates the Quantitative Fair Value Estimate using a statistical model derived from the Fair Value Estimate Morningstar’s equity analysts assign to companies. Please go to http://global.morningstar.com/equ ...

printmgr file - Morgan Stanley

... • Code of Ethics and Business Conduct; • Code of Conduct; and • Integrity Hotline Information. Morgan Stanley’s Code of Ethics and Business Conduct applies to all directors, officers and employees, including our Chief Executive Officer, Chief Financial Officer and Deputy Chief Financial Officer. We ...

... • Code of Ethics and Business Conduct; • Code of Conduct; and • Integrity Hotline Information. Morgan Stanley’s Code of Ethics and Business Conduct applies to all directors, officers and employees, including our Chief Executive Officer, Chief Financial Officer and Deputy Chief Financial Officer. We ...

GLOBAL INSIGHT

... In the U.S., RBC Wealth Management operates as a division of RBC Capital Markets, LLC. In Canada, RBC Wealth Management includes, without limitation, RBC Dominion Securities Inc., which is a foreign affiliate of RBC Capital Markets, LLC. This report has been prepared by RBC Capital Markets, LLC whic ...

... In the U.S., RBC Wealth Management operates as a division of RBC Capital Markets, LLC. In Canada, RBC Wealth Management includes, without limitation, RBC Dominion Securities Inc., which is a foreign affiliate of RBC Capital Markets, LLC. This report has been prepared by RBC Capital Markets, LLC whic ...

Design of Financial Securities: Empirical Evidence from Private-label RMBS Deals

... Some have argued that the equity tranche lost its signaling role during the pre-crisis period because deal sponsors are free to sell them to other entities. Our empirical tests provide evidence contradicting these claims. While we cannot track the ownership of the equity tranche over time directly, ...

... Some have argued that the equity tranche lost its signaling role during the pre-crisis period because deal sponsors are free to sell them to other entities. Our empirical tests provide evidence contradicting these claims. While we cannot track the ownership of the equity tranche over time directly, ...

downstream securities regulation

... produced a securities regulatory regime scattershot with flaws and vulnerabilities. Although previous scholarship, focusing on discrete financial services regulatory issues, has made suggestions for improvement (mutual funds have been a particular interest20), none has suggested a connection among d ...

... produced a securities regulatory regime scattershot with flaws and vulnerabilities. Although previous scholarship, focusing on discrete financial services regulatory issues, has made suggestions for improvement (mutual funds have been a particular interest20), none has suggested a connection among d ...

THE OUTSOURCING OF FINANCIAL REGULATION TO RISK

... in the subprime mortgage market, and this outsourcing of regulation exacerbated the crisis. To understand the crisis, the failure of risk models, and the dangers of regulatory outsourcing, it is helpful to sketch out the system by which mortgages are connected to asset-backed securities, derivatives ...

... in the subprime mortgage market, and this outsourcing of regulation exacerbated the crisis. To understand the crisis, the failure of risk models, and the dangers of regulatory outsourcing, it is helpful to sketch out the system by which mortgages are connected to asset-backed securities, derivatives ...

Methodology And Assumptions: Liquidity

... to meet the ratio test for A/B and at least four of the other supportive characteristics listed below. Few companies qualify for this category. The first three characteristics reference quantitative measures that apply in most industries. In exceptionally stable or volatile industries, however, the ...

... to meet the ratio test for A/B and at least four of the other supportive characteristics listed below. Few companies qualify for this category. The first three characteristics reference quantitative measures that apply in most industries. In exceptionally stable or volatile industries, however, the ...

Private Placement of Securities in Canada

... federal and provincial governments, Canadian municipal governments, Crown corporations and pension funds regulated by the federal or a provincial pension commission; dealers and advisers registered in Canada (other than limited market dealers) automatically qualify as accredited investors; companies ...

... federal and provincial governments, Canadian municipal governments, Crown corporations and pension funds regulated by the federal or a provincial pension commission; dealers and advisers registered in Canada (other than limited market dealers) automatically qualify as accredited investors; companies ...

Crouhy et al. - IME-USP

... default and migration risks. KMVÕs methodology diers somewhat from CreditMetrics as it relies upon the ``Expected Default Frequency'', or EDF, for each issuer, rather than upon the average historical transition frequencies produced by the rating agencies, for each credit class. Both approaches rely ...

... default and migration risks. KMVÕs methodology diers somewhat from CreditMetrics as it relies upon the ``Expected Default Frequency'', or EDF, for each issuer, rather than upon the average historical transition frequencies produced by the rating agencies, for each credit class. Both approaches rely ...

Key Mechanics of Tri-Party Repo Markets

... The GCF Repo Market The GCF (General Collateral Finance) repo market is a blindbrokered interdealer market, meaning that dealers involved in the transactions do not know each other’s identity. GCF trades are arranged by interdealer brokers that preserve the participant’s anonymity. Only securities t ...

... The GCF Repo Market The GCF (General Collateral Finance) repo market is a blindbrokered interdealer market, meaning that dealers involved in the transactions do not know each other’s identity. GCF trades are arranged by interdealer brokers that preserve the participant’s anonymity. Only securities t ...

Reporting Form ARF 210 Liquidity Instruction Guide

... 2.5.1 Adjustment to HQLA2 due to secured lending/borrowing transactions Derived field calculated as the total adjustment to the amount of HQLA2 due to secured lending/borrowing transactions of HQLA2 for the purposes of calculating the cap on HQLA2. 2.5.2 Adjustment to HQLA2 due to collateral swaps T ...

... 2.5.1 Adjustment to HQLA2 due to secured lending/borrowing transactions Derived field calculated as the total adjustment to the amount of HQLA2 due to secured lending/borrowing transactions of HQLA2 for the purposes of calculating the cap on HQLA2. 2.5.2 Adjustment to HQLA2 due to collateral swaps T ...

words

... permitted. The distribution of this prospectus supplement and the accompanying prospectus and the offering or sale of the notes in some jurisdictions may be restricted by law. The notes are offered globally for sale in those jurisdictions in the United States, Europe, Asia and elsewhere where it is ...

... permitted. The distribution of this prospectus supplement and the accompanying prospectus and the offering or sale of the notes in some jurisdictions may be restricted by law. The notes are offered globally for sale in those jurisdictions in the United States, Europe, Asia and elsewhere where it is ...

FSB Securities Lending and Repos: Market Overview and Financial

... shadow banking system. Section 4 provides an overview of existing regulatory frameworks for securities lending and repos, and section 5 lists a number of financial stability issues posed by these markets. Additional detailed information on the market segments and a survey of relevant literature surv ...

... shadow banking system. Section 4 provides an overview of existing regulatory frameworks for securities lending and repos, and section 5 lists a number of financial stability issues posed by these markets. Additional detailed information on the market segments and a survey of relevant literature surv ...

CONFIDENTIAL PRIVATE PLACEMENT MEMORANDUM

... 18156 Darnell Drive, Olney, MD 20832 Telephone: (301) 570-9100 Facsimile: 240-363-0062 [email protected] ...

... 18156 Darnell Drive, Olney, MD 20832 Telephone: (301) 570-9100 Facsimile: 240-363-0062 [email protected] ...

MICROSOFT CORP (Form: 424B2, Received: 01/31/2017 16:20:44)

... We will have the right at our option to redeem the notes of any series, in whole or in part, at any time or from time to time prior to February 6, 2020 (in the case of the 2020 Notes), January 6, 2022 (in the case of the 2022 Notes), December 6, 2023 (in the case of the 2024 Notes), November 6, 2026 ...

... We will have the right at our option to redeem the notes of any series, in whole or in part, at any time or from time to time prior to February 6, 2020 (in the case of the 2020 Notes), January 6, 2022 (in the case of the 2022 Notes), December 6, 2023 (in the case of the 2024 Notes), November 6, 2026 ...

Turning a Blind Eye: Wall Street Finance of Predatory Lending

... the underwriting criteria of The Winter Group, underwriting criteria are generally not available with respect to the mortgage loans. In many instances the mortgage loans in the statistical mortgage pool were acquired by Terwin Advisors LLC from sources, including mortgage brokers and other non-origi ...

... the underwriting criteria of The Winter Group, underwriting criteria are generally not available with respect to the mortgage loans. In many instances the mortgage loans in the statistical mortgage pool were acquired by Terwin Advisors LLC from sources, including mortgage brokers and other non-origi ...

Disclosure Principles for Public Offerings and Listings

... are actively managed (such as securities issued by investment companies), or that contain assets that do not by their terms convert to cash (such as most collateralized debt obligations). In most jurisdictions, securities regulators regulate the ABS covered by these Principles under a different regu ...

... are actively managed (such as securities issued by investment companies), or that contain assets that do not by their terms convert to cash (such as most collateralized debt obligations). In most jurisdictions, securities regulators regulate the ABS covered by these Principles under a different regu ...

index of defined terms

... has any responsibility for any of the actions of any Authorised Offeror, including compliance by an Authorised Offeror with applicable conduct of business rules or other local regulatory requirements or other securities law requirements in relation to such offer. Any person (an "Investor") intending ...

... has any responsibility for any of the actions of any Authorised Offeror, including compliance by an Authorised Offeror with applicable conduct of business rules or other local regulatory requirements or other securities law requirements in relation to such offer. Any person (an "Investor") intending ...

APPLE INC (Form: 424B2, Received: 11/04/2014 06:07:42)

... We are not, and the underwriters are not, making an offer of the notes in any jurisdiction where the offer or sale is not permitted. The distribution of this prospectus supplement and the accompanying prospectus and the offering or sale of the notes in some jurisdictions may be restricted by law. Th ...

... We are not, and the underwriters are not, making an offer of the notes in any jurisdiction where the offer or sale is not permitted. The distribution of this prospectus supplement and the accompanying prospectus and the offering or sale of the notes in some jurisdictions may be restricted by law. Th ...

Credit rating agencies and the subprime crisis

Credit rating agencies (CRAs) — firms which rate debt instruments/securities according to the debtor's ability to pay lenders back — played a significant role at various stages in the American subprime mortgage crisis of 2007-2008 that led to the Great Recession of 2008-2009. The new, complex securities of ""structured finance"" used to finance subprime mortgages could not have been sold without ratings by the ""Big Three"" rating agencies — Moody's Investors Service, Standard & Poor's, and Fitch Ratings. A large section of the debt securities market — many money markets and pension funds — were restricted in their bylaws to holding only the safest securities — i.e securities the rating agencies designated ""triple-A"". The pools of debt the agencies gave their highest ratings to included over three trillion dollars of loans to homebuyers with bad credit and undocumented incomes through 2007. Hundreds of billions of dollars' worth of these triple-A securities were downgraded to ""junk"" status by 2010, and the writedowns and losses came to over half a trillion dollars.This led ""to the collapse or disappearance"" in 2008-9 of three major investment banks (Bear Stearns, Lehman Brothers, and Merrill Lynch), and the federal governments buying of $700 billion of bad debt from distressed financial institutions.