deducting mba education costs

... The General Rules A taxpayer generally may claim a tax credit equal to 20% of the amount spent on education costs. Qualifying education costs include amounts paid after June 30, 1998 for college, graduate school, or vocational training. The maximum amount that qualified is $10,000 per year. Thus, th ...

... The General Rules A taxpayer generally may claim a tax credit equal to 20% of the amount spent on education costs. Qualifying education costs include amounts paid after June 30, 1998 for college, graduate school, or vocational training. The maximum amount that qualified is $10,000 per year. Thus, th ...

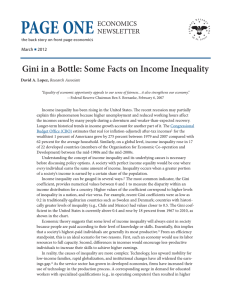

PAGE ONE - St. Louis Fed - Federal Reserve Bank of St. Louis

... wealthiest 1 percent of Americans grew by 275 percent between 1979 and 2007 compared with 62 percent for the average household. Similarly, on a global level, income inequality rose in 17 of 22 developed countries (members of the Organisation for Economic Co-operation and Development) between the mid ...

... wealthiest 1 percent of Americans grew by 275 percent between 1979 and 2007 compared with 62 percent for the average household. Similarly, on a global level, income inequality rose in 17 of 22 developed countries (members of the Organisation for Economic Co-operation and Development) between the mid ...

Georgia and the American Experience

... • The main goal of an entrepreneur is to make profit. Profit is the monetary gain a business owner makes by selling goods or providing services. • The total amount of profit a business makes comes from the following equation: • Total Income – Total expenses = Profit ...

... • The main goal of an entrepreneur is to make profit. Profit is the monetary gain a business owner makes by selling goods or providing services. • The total amount of profit a business makes comes from the following equation: • Total Income – Total expenses = Profit ...

PowerPoint-Notes-Unit-9-Lesson-1-Personal-Finance

... • Saving is really a form of investing. • Investing – Putting money aside in order to receive a greater benefit in the future. • Money can be invested in financial assets such as bank accounts, certificates of deposit, stocks, bonds, and mutual funds. • One of the major benefits of investing is that ...

... • Saving is really a form of investing. • Investing – Putting money aside in order to receive a greater benefit in the future. • Money can be invested in financial assets such as bank accounts, certificates of deposit, stocks, bonds, and mutual funds. • One of the major benefits of investing is that ...