Chapter 5 Merchandising Operations

... of Goods Sold account. In the case of a return, the cost of the merchandise is transferred from Cost of Goods Sold back to Merchandise Inventory. • Sales of Merchandise on Credit: Two entries are necessary. Record the sale as a debit to Accounts Receivable. Update the Cost of Goods sold by tra ...

... of Goods Sold account. In the case of a return, the cost of the merchandise is transferred from Cost of Goods Sold back to Merchandise Inventory. • Sales of Merchandise on Credit: Two entries are necessary. Record the sale as a debit to Accounts Receivable. Update the Cost of Goods sold by tra ...

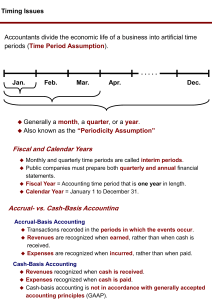

Fiscal and Calendar Years Accrual- vs. Cash

... Revenues earned but not yet received in cash or recorded. Accrued Expenses. Expenses incurred but not yet paid in cash or recorded. ...

... Revenues earned but not yet received in cash or recorded. Accrued Expenses. Expenses incurred but not yet paid in cash or recorded. ...

Chapter 2: Business Processes and Accounting

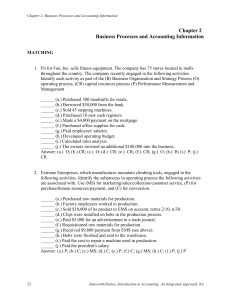

... _____ 1. Activities that involve obtaining the cash or other resources as means to pay for long-term assets, to repay borrowed funds, and provide a return to owners. _____ 2. The set of policies and procedures that promotes operational efficiency, accurate accounting information, and compliance with ...

... _____ 1. Activities that involve obtaining the cash or other resources as means to pay for long-term assets, to repay borrowed funds, and provide a return to owners. _____ 2. The set of policies and procedures that promotes operational efficiency, accurate accounting information, and compliance with ...

Internal Control

... about the achievement of an entity’s objectives with regard to reliability of financial reporting, effectiveness and efficiency of operations, and compliance with applicable laws and regulations. ...

... about the achievement of an entity’s objectives with regard to reliability of financial reporting, effectiveness and efficiency of operations, and compliance with applicable laws and regulations. ...

CHAPTER 4 Outline

... Accrued expenses - expenses incurred but not yet paid in cash or recorded. an adjusting entry for accrued expenses results in a debit or an increase to an expense account and a credit or an increase to a liability account. an adjusting entry for accruals (accrued revenues or accrued expenses) wi ...

... Accrued expenses - expenses incurred but not yet paid in cash or recorded. an adjusting entry for accrued expenses results in a debit or an increase to an expense account and a credit or an increase to a liability account. an adjusting entry for accruals (accrued revenues or accrued expenses) wi ...

Principles of Accounting I

... such as cash, land, accounts receivable, etc. Also there are various kinds of liability accounts such as accounts payable, taxes payable, etc. For our purposes now there are just two categories of owner’s equity accounts: (Capital) Paid In Capital and Retained Earnings. Note that revenue increases r ...

... such as cash, land, accounts receivable, etc. Also there are various kinds of liability accounts such as accounts payable, taxes payable, etc. For our purposes now there are just two categories of owner’s equity accounts: (Capital) Paid In Capital and Retained Earnings. Note that revenue increases r ...

TRUE/FALSE. Write `T` if the statement is true and `F` if the statement

... 54) Merchandising consists of buying and selling products. ...

... 54) Merchandising consists of buying and selling products. ...

merchandising company

... Subtract total expenses from total revenues Two reasons for using the single-step format: 1) Company does not realize any type of profit ...

... Subtract total expenses from total revenues Two reasons for using the single-step format: 1) Company does not realize any type of profit ...

Financial Statements Basics - Duke`s Fuqua School of Business

... liabilities plus equity. We can ensure this balance by making sure that whenever we add (or subtract) an asset from the balance sheet, we add (subtract) something else to make sure we stay in balance. Journal entries achieve this by showing (usually in the top lines, and those not indented) the “deb ...

... liabilities plus equity. We can ensure this balance by making sure that whenever we add (or subtract) an asset from the balance sheet, we add (subtract) something else to make sure we stay in balance. Journal entries achieve this by showing (usually in the top lines, and those not indented) the “deb ...

Accounting Principles, 5e

... Distinguish between under- and overapplied manufacturing overhead. Underapplied manufacturing overhead Overhead assigned to work in process is less than the overhead ...

... Distinguish between under- and overapplied manufacturing overhead. Underapplied manufacturing overhead Overhead assigned to work in process is less than the overhead ...

Test 1 Answers

... Identify the letter of the choice that best completes the statement or answers the question. _D_ ...

... Identify the letter of the choice that best completes the statement or answers the question. _D_ ...

FRANKLIN ELECTRIC CO., INC. AUDIT COMMITTEE CHARTER

... In fulfilling their responsibilities hereunder, it is recognized that members of the Committee are not full-time employees of the Company and are not, and do not represent themselves to be, accountants or auditors by profession or experts in the fields of accounting or auditing, including in respect ...

... In fulfilling their responsibilities hereunder, it is recognized that members of the Committee are not full-time employees of the Company and are not, and do not represent themselves to be, accountants or auditors by profession or experts in the fields of accounting or auditing, including in respect ...

Chapter 17 - McGraw Hill Higher Education

... using activity-based costs Batch costs are based on likely production levels New planned production levels lead to changes in the number of production batches, and changes in total non-volume activity costs -> new break-even or target profit volume ...

... using activity-based costs Batch costs are based on likely production levels New planned production levels lead to changes in the number of production batches, and changes in total non-volume activity costs -> new break-even or target profit volume ...

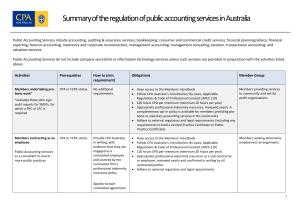

Australia

... partner or equity holder in the future. Members undertaking Public Accounting Services where a PPC is mandatory by regulation (i.e. liquidators). Members wishing to move into public practice. Limited Practice Certificate holders earning over $45,000 gross per calendar year. ...

... partner or equity holder in the future. Members undertaking Public Accounting Services where a PPC is mandatory by regulation (i.e. liquidators). Members wishing to move into public practice. Limited Practice Certificate holders earning over $45,000 gross per calendar year. ...

Financial Accounting, Second Canadian Edition

... Friday) work week, or $400 a day. • Salaries were last paid on October 26 and the next payment of salaries will be November 9. As shown on the calendar on the following slide there are three unpaid work days remain as of October 31. ...

... Friday) work week, or $400 a day. • Salaries were last paid on October 26 and the next payment of salaries will be November 9. As shown on the calendar on the following slide there are three unpaid work days remain as of October 31. ...

Chapter 2 Review of the Accounting Process

... accounts affected by the transaction being recorded. Debits and credits represent increases or decreases to specific accounts, depending on the type of account, as explained earlier. For example, the transactions listed in the illustration above are recorded in general journal format as follows: ...

... accounts affected by the transaction being recorded. Debits and credits represent increases or decreases to specific accounts, depending on the type of account, as explained earlier. For example, the transactions listed in the illustration above are recorded in general journal format as follows: ...

Asset section of the balance sheet

... The Primary Objective of External Financial Reporting is to provide useful economic information about a business to help external parties make sound financial decisions: decision usefulness. The information is necessary for decision makers Most users need the information to project a business’s futu ...

... The Primary Objective of External Financial Reporting is to provide useful economic information about a business to help external parties make sound financial decisions: decision usefulness. The information is necessary for decision makers Most users need the information to project a business’s futu ...

1015 colleen sayther-cunningham xbrl

... solicits comment on the development of data tagging. BACKGROUND: All registrants who file with the Commission are now generally required to file electronically on the Commission's Electronic Data Gathering, Analysis and Retrieval System ("EDGAR")…… As discussed in the accompanying concept release, w ...

... solicits comment on the development of data tagging. BACKGROUND: All registrants who file with the Commission are now generally required to file electronically on the Commission's Electronic Data Gathering, Analysis and Retrieval System ("EDGAR")…… As discussed in the accompanying concept release, w ...

Chapter 1 - Pearson Schools and FE Colleges

... Chapter 1: Introduction to accounting principles Aims of a business ...

... Chapter 1: Introduction to accounting principles Aims of a business ...

Student lecture notes - Pearson Higher Education

... …………………. costs per item, and there is ……………………………………. for the spare capacity which could give a higher contribution per item. Abandonment of a line of business In the short term it is worth continuing if the business makes a ……………………… to fixed costs. If the line of business is abandoned and nothing ...

... …………………. costs per item, and there is ……………………………………. for the spare capacity which could give a higher contribution per item. Abandonment of a line of business In the short term it is worth continuing if the business makes a ……………………… to fixed costs. If the line of business is abandoned and nothing ...

Advanced Accounting, Canadian Edition (Fayerman)

... group one year and not sold by the end of the year, then we need to consider how this affects the following year’s consolidated accounts. • The profit will become realized when the inventory is sold to an external party (in the next financial year). • As inventory is a current asset you should assum ...

... group one year and not sold by the end of the year, then we need to consider how this affects the following year’s consolidated accounts. • The profit will become realized when the inventory is sold to an external party (in the next financial year). • As inventory is a current asset you should assum ...

Certified Hospitality Accountant Executive (CHAE) Review

... What Funds Were Raised by the Sale of Capital Stock What Amount of Dividends Were Paid How Much Was Invested in Long Term Investments The Statement of Cash Flows Required Statement Since 1988 by the FASB Replaces the Statement of Changes in Financial Position ...

... What Funds Were Raised by the Sale of Capital Stock What Amount of Dividends Were Paid How Much Was Invested in Long Term Investments The Statement of Cash Flows Required Statement Since 1988 by the FASB Replaces the Statement of Changes in Financial Position ...

Carry out stock control processes using a computerised system

... Part: partially allocates and despatches selected stock order items ...

... Part: partially allocates and despatches selected stock order items ...

2174 321 syllabus

... 4. Preparation You need to learn much of the material from the textbook, before class. Lectures will assume you have read the material and worked homework problems prior to class. Lectures should be difficult to follow if you are not prepared. Class time will be used to explain concepts and help wit ...

... 4. Preparation You need to learn much of the material from the textbook, before class. Lectures will assume you have read the material and worked homework problems prior to class. Lectures should be difficult to follow if you are not prepared. Class time will be used to explain concepts and help wit ...