Financial Policy Adopted - 030612

... Commonwealth of Virginia's Library and Archives Public Records Management. ...

... Commonwealth of Virginia's Library and Archives Public Records Management. ...

Basics of Economics - Официальный сервер Международного

... certainly, and perhaps more complicated things like business, inflation and unemployment. The science of economics studies all of these, but many more things as well. Perhaps you think that economics is all about the decisions that governments and business managers take. In fact, economics study the ...

... certainly, and perhaps more complicated things like business, inflation and unemployment. The science of economics studies all of these, but many more things as well. Perhaps you think that economics is all about the decisions that governments and business managers take. In fact, economics study the ...

Controlling Cash

... because it is easily concealed. • B. Cash is not readily identifiable and this makes it a likely target for thieves. • C. Cash may be more desirable than other company assets because it can be quickly spent to acquire other things of value. ...

... because it is easily concealed. • B. Cash is not readily identifiable and this makes it a likely target for thieves. • C. Cash may be more desirable than other company assets because it can be quickly spent to acquire other things of value. ...

Instructor`s Manual Chapter 2-7e

... Set up an income statement using the structure and format as shown in Exhibit 2-2, then solve for missing amounts. Calculation sequence: (1) $76,000 - $12,000 = $64,000 income before taxes. (2) $64,000 - $16,000 = $48,000 net income. (3) $76,000 + $44,000 = $120,000 gross profit. (4) $120,000 + $80, ...

... Set up an income statement using the structure and format as shown in Exhibit 2-2, then solve for missing amounts. Calculation sequence: (1) $76,000 - $12,000 = $64,000 income before taxes. (2) $64,000 - $16,000 = $48,000 net income. (3) $76,000 + $44,000 = $120,000 gross profit. (4) $120,000 + $80, ...

Chapter 18 Notes File - National Trail Local School District

... **Only purchases of merchandise on account are journalized in the purchases journal. --Items not recorded in the Purchases Journal: supplies, equipment, services. STEPS: Recording an entry in a purchases journal. 1. Write the date 2. Write the vendor name in the Account Credited column 3. Write the ...

... **Only purchases of merchandise on account are journalized in the purchases journal. --Items not recorded in the Purchases Journal: supplies, equipment, services. STEPS: Recording an entry in a purchases journal. 1. Write the date 2. Write the vendor name in the Account Credited column 3. Write the ...

section 300 financial management policies

... FINANCIAL MANUAL Table of Contents SECTION 100 INTRODUCTION 101 Purpose of Manual .........................................................................................................6 103 Scope and Organization .................................................................................... ...

... FINANCIAL MANUAL Table of Contents SECTION 100 INTRODUCTION 101 Purpose of Manual .........................................................................................................6 103 Scope and Organization .................................................................................... ...

Regulatory and Laws - examprofessional.com

... 50. You will not find this information anywhere else. So please review this section very carefully and ask questions if you do not understand this. 51. Here are some very specific examples of common areas that always go off track: 1. Labor hours over Budget – Your staffing coordinator is not staffin ...

... 50. You will not find this information anywhere else. So please review this section very carefully and ask questions if you do not understand this. 51. Here are some very specific examples of common areas that always go off track: 1. Labor hours over Budget – Your staffing coordinator is not staffin ...

SMS203 - National Open University of Nigeria

... Every proprietor of a business has invested money in his business. This money is used to buy goods and services which he intends to sell at a later date and, very often, to buy the premises, fixtures, machinery, etc. required to carry on the business. The amount of money which he invests in his busi ...

... Every proprietor of a business has invested money in his business. This money is used to buy goods and services which he intends to sell at a later date and, very often, to buy the premises, fixtures, machinery, etc. required to carry on the business. The amount of money which he invests in his busi ...

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

... the interim periods presented are not necessarily indicative of results to be expected for the fiscal year. In the opinion of management, the information contained herein reflects all adjustments necessary to make the results of operations for the interim periods a fair statement of such operations. ...

... the interim periods presented are not necessarily indicative of results to be expected for the fiscal year. In the opinion of management, the information contained herein reflects all adjustments necessary to make the results of operations for the interim periods a fair statement of such operations. ...

ch03

... Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written consent of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The ...

... Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written consent of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The ...

Free Sample

... 82. The controller for Tires and More, Inc. has recorded the following transactions during the month: the owner established the business with a $20,000 investment on the 1st of the month; the company recorded $36,000 of revenue for tires and services provided during the month; and expenses of $22,00 ...

... 82. The controller for Tires and More, Inc. has recorded the following transactions during the month: the owner established the business with a $20,000 investment on the 1st of the month; the company recorded $36,000 of revenue for tires and services provided during the month; and expenses of $22,00 ...

Preview Sample 1

... 82. The controller for Tires and More, Inc. has recorded the following transactions during the month: the owner established the business with a $20,000 investment on the 1st of the month; the company recorded $36,000 of revenue for tires and services provided during the month; and expenses of $22,00 ...

... 82. The controller for Tires and More, Inc. has recorded the following transactions during the month: the owner established the business with a $20,000 investment on the 1st of the month; the company recorded $36,000 of revenue for tires and services provided during the month; and expenses of $22,00 ...

National Income and Environmental Accounting

... measurement of physical flows and environmental assets (we won’t discuss environmentallyrelated economic activity in this chapter, but will discuss some of these issues in Chapter 14). Beyond the SEEA recommendations, other approaches seek to either adjust existing measures of national accounting, o ...

... measurement of physical flows and environmental assets (we won’t discuss environmentallyrelated economic activity in this chapter, but will discuss some of these issues in Chapter 14). Beyond the SEEA recommendations, other approaches seek to either adjust existing measures of national accounting, o ...

Pennsylvania Public Library Accounting Manual

... receive $50,000 or less in annual funding from the Commonwealth of Pennsylvania) that do not have full-time bookkeepers or accountants. For this reason, the manual’s main focus is on illustrating basic accounting principles in layman’s terms and instructions for accessing resources online. The manua ...

... receive $50,000 or less in annual funding from the Commonwealth of Pennsylvania) that do not have full-time bookkeepers or accountants. For this reason, the manual’s main focus is on illustrating basic accounting principles in layman’s terms and instructions for accessing resources online. The manua ...

LMC CAPITAL CORP (Form: 10KSB, Received: 03

... of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) been subject to such filing requirements for the past 90 days. Yes [X ] No [ ]. Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulat ...

... of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) been subject to such filing requirements for the past 90 days. Yes [X ] No [ ]. Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulat ...

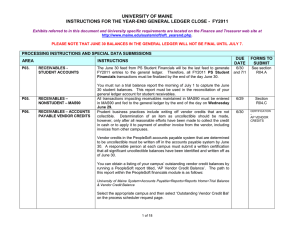

1 - University of Maine

... Financials transactions must be finalized by the end of the day June 30. You must run a trial balance report the morning of July 1 to capture the June 30 student balances. This report must be used in the reconciliation of your general ledger account for student receivables. All transactions impactin ...

... Financials transactions must be finalized by the end of the day June 30. You must run a trial balance report the morning of July 1 to capture the June 30 student balances. This report must be used in the reconciliation of your general ledger account for student receivables. All transactions impactin ...

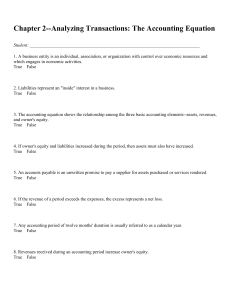

Chapter 2--Analyzing Transactions: The Accounting Equation

... 7. Consists of the three basic accounting elements: assets = liabilities + owner's equity. 8. The concept that nonbusiness assets and liabilities are not included in the business' accounting records. 9. An economic event that has a direct impact on the business. 10. An unwritten promise to pay a sup ...

... 7. Consists of the three basic accounting elements: assets = liabilities + owner's equity. 8. The concept that nonbusiness assets and liabilities are not included in the business' accounting records. 9. An economic event that has a direct impact on the business. 10. An unwritten promise to pay a sup ...

Aue2602 Summary

... company will be able to collect. Also to prevent false credit notes being passed and the money stolen source document design – e.g. numbering, control over blank forms and limited information that can be keyed in etc comparison and reconciliation – must frequently and timeously check : orders ...

... company will be able to collect. Also to prevent false credit notes being passed and the money stolen source document design – e.g. numbering, control over blank forms and limited information that can be keyed in etc comparison and reconciliation – must frequently and timeously check : orders ...

Chapter 7

... translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written consent of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may m ...

... translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written consent of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may m ...

Financial Accounting and Accounting Standards

... LO 1 Explain the revenue recognition principle and the expense recognition principle. ...

... LO 1 Explain the revenue recognition principle and the expense recognition principle. ...

Liabilities and Shareholders` Equity

... transactions. We record other transactions affecting net income for the period in the retained earnings account and then prepare an income statement from these entries. You will find it helpful to label each entry with the type of revenue (for example, sales revenue, interest revenue) and expense (f ...

... transactions. We record other transactions affecting net income for the period in the retained earnings account and then prepare an income statement from these entries. You will find it helpful to label each entry with the type of revenue (for example, sales revenue, interest revenue) and expense (f ...

Write-off of Accounts Receivable

... During 2015, Omega Company had net sales of $11,400,000. Most of the sales were on credit. At the end of 2015, the balance of Accounts Receivable was $1,400,000, and Allowance for Uncollectible Accounts had a debit balance of $48,000. • Omega Company's management uses two methods of estimating uncol ...

... During 2015, Omega Company had net sales of $11,400,000. Most of the sales were on credit. At the end of 2015, the balance of Accounts Receivable was $1,400,000, and Allowance for Uncollectible Accounts had a debit balance of $48,000. • Omega Company's management uses two methods of estimating uncol ...

History of accounting

The history of accounting or accountancy is thousands of years old and can be traced to ancient civilisations.The early development of accounting dates back to ancient Mesopotamia, and is closely related to developments in writing, counting and money and early auditing systems by the ancient Egyptians and Babylonians. By the time of the Emperor Augustus, the Roman government had access to detailed financial information.Some Hindus believe that the Indian Chanakya created a work similar to a financial management book, during the period of the Maurya Empire. His book ""Arthashasthra"" contains few detailed aspects of maintaining books of accounts for a Sovereign State. The Italian Luca Pacioli, recognized as The Father of accounting and bookeeping was the first person to publish a work on double-entry bookkeeping, which then developed in medieval Europe. Accounting began to transition into an organized profession in the nineteenth century, with local professional bodies in England merging to form the Institute of Chartered Accountants in England and Wales in 1880.