Document

... 80% for property purchase). • The current funding structure has an average duration of 1.8 y, which does not allow banks to offer fixedrate mortgages. • The Peruvian financial system has to look for other long-term funding ...

... 80% for property purchase). • The current funding structure has an average duration of 1.8 y, which does not allow banks to offer fixedrate mortgages. • The Peruvian financial system has to look for other long-term funding ...

Mortgage backed securities

... 7.3 Market Risk The market risk is the risk that the price of the security may fluctuate over time. For the Mortgage backed securities (MBS) prepayment risk and market risk are closely linked. Interest rates movements have greater impacts on MBS than traditional fixed-income investments, because the ...

... 7.3 Market Risk The market risk is the risk that the price of the security may fluctuate over time. For the Mortgage backed securities (MBS) prepayment risk and market risk are closely linked. Interest rates movements have greater impacts on MBS than traditional fixed-income investments, because the ...

Financing Options for Your Small Business Guide

... Export Working Capital Program (EWCP) SBA provides lenders with up to a 90% guaranty on export loans as a credit enhancement, so that the lenders will make the necessary export working capital available. The SBA delivers its export loan program through a network of SBA Senior International Credit Of ...

... Export Working Capital Program (EWCP) SBA provides lenders with up to a 90% guaranty on export loans as a credit enhancement, so that the lenders will make the necessary export working capital available. The SBA delivers its export loan program through a network of SBA Senior International Credit Of ...

BANK INTEREST RATE MARGINS

... on all loans and investments (including non-accrual loans) and the average interest rate paid on deposits (including zero-interest deposit accounts) and other interest-bearing liabilities. On their Australian domestic business, it is estimated that average net spreads for the major bank groups2 were ...

... on all loans and investments (including non-accrual loans) and the average interest rate paid on deposits (including zero-interest deposit accounts) and other interest-bearing liabilities. On their Australian domestic business, it is estimated that average net spreads for the major bank groups2 were ...

PRACTICE ONLY

... than you otherwise think it is worth, due to the financing offer? (a) Zero, by definition. (b) $26,497 (c) $79,854 (d) $98,412 21. Again considering the same seller loan offer as in the previous question, suppose you face a 35% marginal income tax rate and so does the marginal investor in the debt m ...

... than you otherwise think it is worth, due to the financing offer? (a) Zero, by definition. (b) $26,497 (c) $79,854 (d) $98,412 21. Again considering the same seller loan offer as in the previous question, suppose you face a 35% marginal income tax rate and so does the marginal investor in the debt m ...

Green - American Council on Consumer Interests

... loans that affected their ability to pay for their homes. Financial ratio results indicated housing was the largest item affecting the household balance sheet of participants. In addition, findings also indicated that many consumers made attempts to communicate with their mortgage lenders and were d ...

... loans that affected their ability to pay for their homes. Financial ratio results indicated housing was the largest item affecting the household balance sheet of participants. In addition, findings also indicated that many consumers made attempts to communicate with their mortgage lenders and were d ...

PowerPoint-presentasjon

... reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly, results could differ materially from those set out in the forwardlooking statements as a result of various factors. Important factors that may c ...

... reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly, results could differ materially from those set out in the forwardlooking statements as a result of various factors. Important factors that may c ...

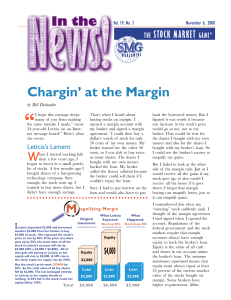

Chargin` at the Margin

... buy stock. For example, Leticia wanted to buy $4,000 worth of stock on margin. She first had to deposit $2,000 of equity (cash) before her broker would loan her the other $2,000. In a sense, the margin is like a minimum down payment. The Federal Reserve sets this minimum, which today requires invest ...

... buy stock. For example, Leticia wanted to buy $4,000 worth of stock on margin. She first had to deposit $2,000 of equity (cash) before her broker would loan her the other $2,000. In a sense, the margin is like a minimum down payment. The Federal Reserve sets this minimum, which today requires invest ...

New MAP Guide CNA Ordering Process

... HUD issued the Draft MAP Guide on February 28, 2015. Based upon comments made by HUD at the Eastern Lenders Conference, we can expect the “Final” version of the MAP Guide to be issued prior to Labor Day. With this anticipated release timeframe, we would expect lenders to consider preparing applicati ...

... HUD issued the Draft MAP Guide on February 28, 2015. Based upon comments made by HUD at the Eastern Lenders Conference, we can expect the “Final” version of the MAP Guide to be issued prior to Labor Day. With this anticipated release timeframe, we would expect lenders to consider preparing applicati ...

PSSA 1.8 Percent and Simple Interest PSSA PREP

... The cost of a school lunch went up from $1.60 to $1.85. What was the percent of increase in the cost of a school lunch? ...

... The cost of a school lunch went up from $1.60 to $1.85. What was the percent of increase in the cost of a school lunch? ...

Chapter 17 An Introduction to the Process of Real Estate Finance

... have run about .5% to 1.5% for short term investments and 1.5% to 4% for longer term investments over the last few decades ...

... have run about .5% to 1.5% for short term investments and 1.5% to 4% for longer term investments over the last few decades ...