Consolidated financial statements

... 16.1 Income for the period – Equity holders of Air France-KLM per share ........................................ - 43 16.2 Non-dilutive instruments ................................................................................................................... - 43 16.3 Instruments issued after t ...

... 16.1 Income for the period – Equity holders of Air France-KLM per share ........................................ - 43 16.2 Non-dilutive instruments ................................................................................................................... - 43 16.3 Instruments issued after t ...

Chapter 3

... Explain what a journal is and how it helps in the recording process. Explain what a ledger is and how it helps in the recording process. Explain what posting is and how it helps in the recording process. Explain the purposes of a trial balance. ...

... Explain what a journal is and how it helps in the recording process. Explain what a ledger is and how it helps in the recording process. Explain what posting is and how it helps in the recording process. Explain the purposes of a trial balance. ...

Bitcoin Comes of Age

... Miners who produce new bitcoin and merchant processors who accumulate bitcoin and disburse dollars would prefer to actually deliver their bitcoin to settle their hedges; meanwhile, consumer on‐ramps like Circle Financial would prefer to receive bitcoin on settlement to be able to deliver it to t ...

... Miners who produce new bitcoin and merchant processors who accumulate bitcoin and disburse dollars would prefer to actually deliver their bitcoin to settle their hedges; meanwhile, consumer on‐ramps like Circle Financial would prefer to receive bitcoin on settlement to be able to deliver it to t ...

0000950123-10-015388 - Gentex Investor Relations

... (Do not check if a smaller reporting company) ...

... (Do not check if a smaller reporting company) ...

CHAPTER FOUR Cash Accounting, Accrual Accounting

... However, this calculation discounts the cash flows from the debt with an 8% discount rate rather than the 10% rate for the debt. Discount the free cash flows (before debt flows) at 8% yields the $174.44 calculated in part (a). Then take off the present value of the debt flows discounted at 10%. You ...

... However, this calculation discounts the cash flows from the debt with an 8% discount rate rather than the 10% rate for the debt. Discount the free cash flows (before debt flows) at 8% yields the $174.44 calculated in part (a). Then take off the present value of the debt flows discounted at 10%. You ...

Management & Engineering Study on Non-financial Value of Tourism Listed Companies

... of investment, environmental restoration and so on. Environmental capacity is the maximum load of pollutants in a given environment, there the natural ecological structure and normal function is not compromised, in premise that the quality of human environment does not decline. When the tourist acti ...

... of investment, environmental restoration and so on. Environmental capacity is the maximum load of pollutants in a given environment, there the natural ecological structure and normal function is not compromised, in premise that the quality of human environment does not decline. When the tourist acti ...

Chapter #3 Practice Q`s

... Under the accrual basis of accounting a. cash must be received before revenue is recognized. b. net income is calculated by matching cash outflows against cash inflows. c. events that change a company's financial statements are recognized in the period they occur rather than in the period in which c ...

... Under the accrual basis of accounting a. cash must be received before revenue is recognized. b. net income is calculated by matching cash outflows against cash inflows. c. events that change a company's financial statements are recognized in the period they occur rather than in the period in which c ...

Distinguishing Liabilities from Equity (Topic 480).

... and not the individual views of the members or the organizations with which they are affiliated. The organization and operating procedures of the Committee are outlined in Appendix A to this letter. We do not believe the Board should move forward with Part I of the proposed ASU at this time. Rather, ...

... and not the individual views of the members or the organizations with which they are affiliated. The organization and operating procedures of the Committee are outlined in Appendix A to this letter. We do not believe the Board should move forward with Part I of the proposed ASU at this time. Rather, ...

practiceqs_chapter3

... Under the accrual basis of accounting a. cash must be received before revenue is recognized. b. net income is calculated by matching cash outflows against cash inflows. c. events that change a company's financial statements are recognized in the period they occur rather than in the period in which c ...

... Under the accrual basis of accounting a. cash must be received before revenue is recognized. b. net income is calculated by matching cash outflows against cash inflows. c. events that change a company's financial statements are recognized in the period they occur rather than in the period in which c ...

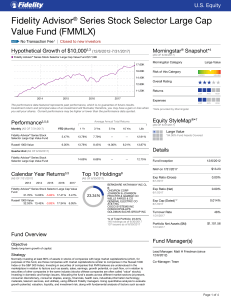

Fidelity Advisor® Series Stock Selector Large Cap Value Fund

... 6. Percent Rank in Category is the fund's total-return percentile rank relative to all funds that have the same Morningstar Category. The highest (or most favorable) percentile rank is 1 and the lowest (or least favorable) percentile rank is 100. The top-performing fund in a category will always rec ...

... 6. Percent Rank in Category is the fund's total-return percentile rank relative to all funds that have the same Morningstar Category. The highest (or most favorable) percentile rank is 1 and the lowest (or least favorable) percentile rank is 100. The top-performing fund in a category will always rec ...

Asset Valuation in Workably Competitive Markets

... of new assets, whether those assets represent additional capacity to supply or are replacements for old assets that have come to the end of their economic lives. This avoids ‘asset handover’ problems, since questions about the implications of the notion of workable/effective competition are restrict ...

... of new assets, whether those assets represent additional capacity to supply or are replacements for old assets that have come to the end of their economic lives. This avoids ‘asset handover’ problems, since questions about the implications of the notion of workable/effective competition are restrict ...

Corporate Finance

... o Twice as large as equity and bond markets combined The total market value (based on positive side): less than $3 trln ...

... o Twice as large as equity and bond markets combined The total market value (based on positive side): less than $3 trln ...

stock price reactions to securities fraud class actions

... while motions to dismiss are pending, thereby depriving plaintiffs of access to the sources most likely to provide the facts necessary to plead fraud with particularity. The goal of the Reform Act is to provide a more rigorous screen for sorting meritorious from non-meritorious cases through the mec ...

... while motions to dismiss are pending, thereby depriving plaintiffs of access to the sources most likely to provide the facts necessary to plead fraud with particularity. The goal of the Reform Act is to provide a more rigorous screen for sorting meritorious from non-meritorious cases through the mec ...

Principles-of-Financial-Accounting-11th-Edition

... misconception about what debit and credit really mean. Tell students who work in a bank to reverse what they have learned about debits and credits. Finally, explain the beauty of the double-entry system. Students need to know that transactions are not recorded in T accounts in practice, but T accoun ...

... misconception about what debit and credit really mean. Tell students who work in a bank to reverse what they have learned about debits and credits. Finally, explain the beauty of the double-entry system. Students need to know that transactions are not recorded in T accounts in practice, but T accoun ...

On over Diversification in Operation Strategies

... buyers' market, the market spectrum has changed from the regional to the global, and the customer demand has moved from mass to individualized requirement. After such a series of changes, it is easy for corporations to get into over diversification even though they diversify suitably before. For exa ...

... buyers' market, the market spectrum has changed from the regional to the global, and the customer demand has moved from mass to individualized requirement. After such a series of changes, it is easy for corporations to get into over diversification even though they diversify suitably before. For exa ...

XEROX CORP (Form: 11-K, Received: 06/28/2013 12:36:19)

... fund and the participant notes fund. Loans used for the purchase of a primary residence have a maximum term of fifteen years. All other loans have a maximum term of five years. The interest rate on loan transactions is commensurate with current rates. As of December 31, 2012 and 2011, interest rates ...

... fund and the participant notes fund. Loans used for the purchase of a primary residence have a maximum term of fifteen years. All other loans have a maximum term of five years. The interest rate on loan transactions is commensurate with current rates. As of December 31, 2012 and 2011, interest rates ...