Ownership structure and the performance of firms

... Nevertheless this indicator is not free of criticism. Indeed ROI uses the net profit that very often includes non-operating elements. That is why it would be better to choose EBITDA (earning before interest and taxes and depreciation) because this measurement excludes in particular amortisation. In ...

... Nevertheless this indicator is not free of criticism. Indeed ROI uses the net profit that very often includes non-operating elements. That is why it would be better to choose EBITDA (earning before interest and taxes and depreciation) because this measurement excludes in particular amortisation. In ...

To: Clients and Friends June 30, 2004 The articles below contain

... partnership, foreign trust (other than a foreign grantor trust) or a foreign estate is considered as being owned proportionately by its partners or beneficiaries. A U.S. person which wants to make a Section 1296 election for a taxable year must make it on or before the due date of its U.S. Federal i ...

... partnership, foreign trust (other than a foreign grantor trust) or a foreign estate is considered as being owned proportionately by its partners or beneficiaries. A U.S. person which wants to make a Section 1296 election for a taxable year must make it on or before the due date of its U.S. Federal i ...

STRONG ORDER BOOKINGS INCREASED MARKET RISK

... MSEK 1,071 as of 31 December 2014. This had a negative impact on cash flow from operating activities of MSEK 685 during the first half-year 2015. The operational cash flow amounted to MSEK -1,806 (-1,097). It is defined as cash flow from operating activities, excluding taxes and other financial item ...

... MSEK 1,071 as of 31 December 2014. This had a negative impact on cash flow from operating activities of MSEK 685 during the first half-year 2015. The operational cash flow amounted to MSEK -1,806 (-1,097). It is defined as cash flow from operating activities, excluding taxes and other financial item ...

89KB - NZQA

... can be used to pay back the mortgage (cover interest payments), which if finance costs remain constant, will result in a decrease in the finance cost percentage. ...

... can be used to pay back the mortgage (cover interest payments), which if finance costs remain constant, will result in a decrease in the finance cost percentage. ...

Management Accounting Practices in Egypt

... done in the USA, by Ernst and Young (2003); in the UK, (Abdel-Kader and Luther 2006 and 2008; Bhimani 1996; Burns et. al 1996, 1999), Ireland (Clarke 1997), Australia (Chenhall and LangfieldSmith 1998), New Zealand (Lamminmaki and Drury 2001) and South Africa (Weweru et. al 2005). Studies were also ...

... done in the USA, by Ernst and Young (2003); in the UK, (Abdel-Kader and Luther 2006 and 2008; Bhimani 1996; Burns et. al 1996, 1999), Ireland (Clarke 1997), Australia (Chenhall and LangfieldSmith 1998), New Zealand (Lamminmaki and Drury 2001) and South Africa (Weweru et. al 2005). Studies were also ...

Assignment 1 is compulsory and due

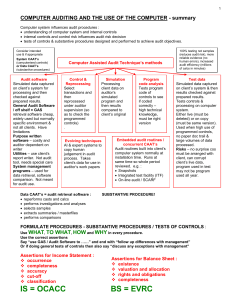

... extract a sample of purchase invoices and inspect that they are made out to the entity and that the items purchases appear on the entity’s inventory list and aren’t fictitious extract a sample of purchase invoices and inspect bank statements to confirm that payment for the goods was made to the ...

... extract a sample of purchase invoices and inspect that they are made out to the entity and that the items purchases appear on the entity’s inventory list and aren’t fictitious extract a sample of purchase invoices and inspect bank statements to confirm that payment for the goods was made to the ...

ACE HARDWARE CORPORATION 2015 Annual Report

... The Company determines the appropriate classification of its investments in marketable securities, which are predominately held by the Company’s New Age Insurance, Ltd. (“NAIL”) subsidiary, at the time of purchase and evaluates such designation at each balance sheet date. All marketable securities h ...

... The Company determines the appropriate classification of its investments in marketable securities, which are predominately held by the Company’s New Age Insurance, Ltd. (“NAIL”) subsidiary, at the time of purchase and evaluates such designation at each balance sheet date. All marketable securities h ...

Sample Glossary of Investment-Related Terms for

... Interest/Interest Rate: The fee charged by a lender to a borrower, usually expressed as an annual percentage of the principal. For example, someone investing in bonds will receive interest payments from the bond’s issuer. Interest Rate Risk: The possibility that a bond’s or bond fund’s market value ...

... Interest/Interest Rate: The fee charged by a lender to a borrower, usually expressed as an annual percentage of the principal. For example, someone investing in bonds will receive interest payments from the bond’s issuer. Interest Rate Risk: The possibility that a bond’s or bond fund’s market value ...

The Fallacy behind Investor versus Fund Returns

... application of an inadequately-analyzed, poorly-understood mathematical measure. As I will explain, there is no way to determine if investors underperform the mutual funds they own, either because of bad timing or for any other reason. Why is it a desirable result for investment professionals? A com ...

... application of an inadequately-analyzed, poorly-understood mathematical measure. As I will explain, there is no way to determine if investors underperform the mutual funds they own, either because of bad timing or for any other reason. Why is it a desirable result for investment professionals? A com ...

Rajiv Gandhi Equity Savings Scheme

... “ financial year” means a year commencing on the 1st day of April and ending on the 31st day of March; “Form” means the Form appended to the Scheme; “investment” means investment by an assessee in any of the eligible securities in accordance with the Scheme; “new retail investor” means the following ...

... “ financial year” means a year commencing on the 1st day of April and ending on the 31st day of March; “Form” means the Form appended to the Scheme; “investment” means investment by an assessee in any of the eligible securities in accordance with the Scheme; “new retail investor” means the following ...

Trial Measures for Overseas Securities Investment by Qualified

... and regulations and the stipulations of the contract on funds and contract on pooled assets management; (7) ensuring that the funds and the scheme can be confirmed and their profit distribution schemes implemented according to the relevant laws and regulations, contract on funds and contract on pool ...

... and regulations and the stipulations of the contract on funds and contract on pooled assets management; (7) ensuring that the funds and the scheme can be confirmed and their profit distribution schemes implemented according to the relevant laws and regulations, contract on funds and contract on pool ...

GAAP - WikiLeaks

... Revenues should include estimates of revenue over a period not to exceed ten years from the date of delivery of the first episode or, if still in production, five years from the date of delivery of the most recent episode, if later. Revenue estimates for secondary markets should be included only if ...

... Revenues should include estimates of revenue over a period not to exceed ten years from the date of delivery of the first episode or, if still in production, five years from the date of delivery of the most recent episode, if later. Revenue estimates for secondary markets should be included only if ...

e-Business

... The Demise of Dot Com Retailers. Weak financials, intense competition, and investor flight will drive many of today's online retailers out of business in 2000. Those that survive must refocus funding on building hard assets to achieve scale, service, and speed. ...

... The Demise of Dot Com Retailers. Weak financials, intense competition, and investor flight will drive many of today's online retailers out of business in 2000. Those that survive must refocus funding on building hard assets to achieve scale, service, and speed. ...

Long-Term Investment Policy - American Speech

... Interest-bearing checking accounts at insured commercial banking institutions Interest-bearing savings accounts at insured commercial banking institutions Certificates of deposit at insured commercial banking institutions Money market funds ...

... Interest-bearing checking accounts at insured commercial banking institutions Interest-bearing savings accounts at insured commercial banking institutions Certificates of deposit at insured commercial banking institutions Money market funds ...

Chapter 4 - Financial Statement Analysis and

... • If ACP is 40 days, and the firm’s credit policy is net 30, clearly, customers are not paying in keeping with the firm’s policy, and there may be concerns about the quality of the firm’s customers, and what might happen if economic conditions deteriorate. ...

... • If ACP is 40 days, and the firm’s credit policy is net 30, clearly, customers are not paying in keeping with the firm’s policy, and there may be concerns about the quality of the firm’s customers, and what might happen if economic conditions deteriorate. ...

Accounting for financial instruments with characteristics of debt and

... Framework) provides definitions of these elements. However, with equity defined as a residual the Framework provides only limited guidance for the classification of a transaction or event as representing a liability or equity. In addition, developments in the nature and complexity of compound financ ...

... Framework) provides definitions of these elements. However, with equity defined as a residual the Framework provides only limited guidance for the classification of a transaction or event as representing a liability or equity. In addition, developments in the nature and complexity of compound financ ...

View COLL 6.3 as PDF

... (2) The prospectus of a scheme must contain information about its regular valuation points for the purposes of dealing in units in accordance with ■ COLL 4.2.5R (16) (Table: contents of the prospectus). (3) Where a scheme operates limited redemption arrangements, (1) does not apply and the valuation ...

... (2) The prospectus of a scheme must contain information about its regular valuation points for the purposes of dealing in units in accordance with ■ COLL 4.2.5R (16) (Table: contents of the prospectus). (3) Where a scheme operates limited redemption arrangements, (1) does not apply and the valuation ...

Informational Asymmetry and the Demand for IPOs: An Explanation

... holds true for the stock exchanges, any alteration of a stock price reflects a change in its issuer's valuation. This value is determined by many factors and the valuation changes as either firm specific or general market news becomes available to the public. The laws governing the stock exchanges a ...

... holds true for the stock exchanges, any alteration of a stock price reflects a change in its issuer's valuation. This value is determined by many factors and the valuation changes as either firm specific or general market news becomes available to the public. The laws governing the stock exchanges a ...

Change in the rules regarding limitations for collateral in the form of

... counterparty or by a group of closely-related issuers. The Riksbank noted at that time that there was no evident optimum level for such a limit, but reached the conclusion that 25 per cent was a reasonable level. At present, however, the limitation only applies to (i) covered bonds issued by the cou ...

... counterparty or by a group of closely-related issuers. The Riksbank noted at that time that there was no evident optimum level for such a limit, but reached the conclusion that 25 per cent was a reasonable level. At present, however, the limitation only applies to (i) covered bonds issued by the cou ...

Classification of Financial Assets and Liabilities

... monetary authority sells gold bullion that is part of reserve assets to institutional units other than monetary authorities or international financial institutions, the gold is demonetized, resulting in a change in the classification of gold bullion from a financial asset to a nonfinancial asset bef ...

... monetary authority sells gold bullion that is part of reserve assets to institutional units other than monetary authorities or international financial institutions, the gold is demonetized, resulting in a change in the classification of gold bullion from a financial asset to a nonfinancial asset bef ...