Horizons US 7-10 Year Treasury Bond CAD

... performance of the U.S. 7-10 year Treasury bond market, hedged to the Canadian dollar. The Solactive US 7-10 Year Treasury Bond CAD Hedged Index constituents are selected based on size and maturity criteria, and generally have a maturity between 7 and 10 years at the time of inclusion. Volatility in ...

... performance of the U.S. 7-10 year Treasury bond market, hedged to the Canadian dollar. The Solactive US 7-10 Year Treasury Bond CAD Hedged Index constituents are selected based on size and maturity criteria, and generally have a maturity between 7 and 10 years at the time of inclusion. Volatility in ...

Comprehensive Case A.1 – Enron

... exist, the company's internal control over financial reporting cannot be considered effective.” In the Appendix of Auditing Standard #5, paragraph #A5 provides more specifics about the definition of an internal control system. According to that paragraph, such a system is “a process designed by, or ...

... exist, the company's internal control over financial reporting cannot be considered effective.” In the Appendix of Auditing Standard #5, paragraph #A5 provides more specifics about the definition of an internal control system. According to that paragraph, such a system is “a process designed by, or ...

The Timing of Asset Sales

... implicit contracts. Incentives arising from stakeholder costs are associated with the role of reported earnings in assessing the ability of the firm to honour implicit claims, such as warranties, employment contracts, use of trade credit and so on. Controlling for traditional earnings management inc ...

... implicit contracts. Incentives arising from stakeholder costs are associated with the role of reported earnings in assessing the ability of the firm to honour implicit claims, such as warranties, employment contracts, use of trade credit and so on. Controlling for traditional earnings management inc ...

Philippine Bond Market Guide

... International Experts for their contribution to provide information from their own market guides, as well as their valuable expertise. Because of their cooperation and contribution, the ADB Team started the research on solid ground. Last, but not least, the ADB Team would like to thank all the inter ...

... International Experts for their contribution to provide information from their own market guides, as well as their valuable expertise. Because of their cooperation and contribution, the ADB Team started the research on solid ground. Last, but not least, the ADB Team would like to thank all the inter ...

Document

... to record After studying this and summarize the effects chapter, you shouldof transactions on financial statements. be able to: 2. Describe the characteristics of an account. 3. List the rules of debit and credit and the normal balances of accounts. 4. Analyze and summarize the financial statement e ...

... to record After studying this and summarize the effects chapter, you shouldof transactions on financial statements. be able to: 2. Describe the characteristics of an account. 3. List the rules of debit and credit and the normal balances of accounts. 4. Analyze and summarize the financial statement e ...

Boeing 2006 Annual Report

... * Before cumulative effect of accounting change and net gain (loss) from discontinued operations. †Commercial Airplanes backlog at December 31, 2005, has been reduced by $7.8 billion to reflect the planned change in accounting for concessions effective January 1, 2006. Had December 31, 2004, reflect ...

... * Before cumulative effect of accounting change and net gain (loss) from discontinued operations. †Commercial Airplanes backlog at December 31, 2005, has been reduced by $7.8 billion to reflect the planned change in accounting for concessions effective January 1, 2006. Had December 31, 2004, reflect ...

Financing Durable Assets

... find that weak legal enforcement is associated with both older aircraft and older technologies. Our model abstracts from several features of durable asset markets that have been considered in the literature including adverse selection,8 illiquidity,9 and heterogeneity across firms other than that in ...

... find that weak legal enforcement is associated with both older aircraft and older technologies. Our model abstracts from several features of durable asset markets that have been considered in the literature including adverse selection,8 illiquidity,9 and heterogeneity across firms other than that in ...

WATSCO INC (Form: 10-K, Received: 02/29/2016 14:38:52)

... capital spending in the commercial construction market; ...

... capital spending in the commercial construction market; ...

Blanchard_Reinsurance_2012.xlsx

... X Freihaut, D.; and Vendetti, P., “Common Pitfalls and Practical Considerations in Risk Transfer Analysis,” Question: In the Reinsurance Attestation Supplement (RAS), what are the CEO and CFO required to confirm? Reasons for this? Answer: 1. There are no separate written or oral agreements between t ...

... X Freihaut, D.; and Vendetti, P., “Common Pitfalls and Practical Considerations in Risk Transfer Analysis,” Question: In the Reinsurance Attestation Supplement (RAS), what are the CEO and CFO required to confirm? Reasons for this? Answer: 1. There are no separate written or oral agreements between t ...

TVN plc – the meaning behind the IPO

... Who are the Allowed Proprietors for TVN shares according to the bond issue agreement clauses? And who are the attested members of the Board of Directors? The TVN Prospectus provides no answer for such questions, though that is really basic information, taking into account the corporate rights of the ...

... Who are the Allowed Proprietors for TVN shares according to the bond issue agreement clauses? And who are the attested members of the Board of Directors? The TVN Prospectus provides no answer for such questions, though that is really basic information, taking into account the corporate rights of the ...

DOC - Investor Relations

... to help CIOs, senior IT executives and other business executives become more effective in their enterprises. An EP membership leverages the knowledge and expertise of Gartner in ways that are specific to the CIO’s needs and offers role-based offerings and member-only communities for peer-based colla ...

... to help CIOs, senior IT executives and other business executives become more effective in their enterprises. An EP membership leverages the knowledge and expertise of Gartner in ways that are specific to the CIO’s needs and offers role-based offerings and member-only communities for peer-based colla ...

Carbon avoidance? Accounting for the emissions hidden in reserves

... Higher-quality business reporting and disclosure are needed to better reflect the climate change uncertainties facing companies. This information is required by both companies and their investors in order to take appropriate action. To start improving the current situation, companies need to commit ...

... Higher-quality business reporting and disclosure are needed to better reflect the climate change uncertainties facing companies. This information is required by both companies and their investors in order to take appropriate action. To start improving the current situation, companies need to commit ...

Aue2602 Summary

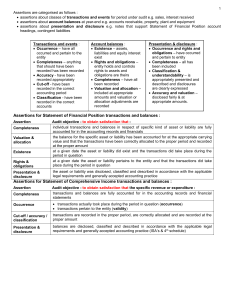

... recorded at correct amount (accuracy) and are allocated in proper accounting period (cut-off) have all been recorded (completeness) in the proper accounts (classification) Receipts (transactions) : payment from debtor actually occurred and pertains to entity (occurrence) receipts are recorde ...

... recorded at correct amount (accuracy) and are allocated in proper accounting period (cut-off) have all been recorded (completeness) in the proper accounts (classification) Receipts (transactions) : payment from debtor actually occurred and pertains to entity (occurrence) receipts are recorde ...

Accounting Codes - University of California | Office of The President

... II and III. Section II prescribes the use of each code and indicates the office responsible for assigning the code numbers. Section III is a detailed listing of the code numbers. The two sections are parallel in organization; subsections II.A. and III.A., for example, both cover ...

... II and III. Section II prescribes the use of each code and indicates the office responsible for assigning the code numbers. Section III is a detailed listing of the code numbers. The two sections are parallel in organization; subsections II.A. and III.A., for example, both cover ...

Financial reporting developments: Asset Retirement Obligations

... The accounting guidance in ASC 410-20 applies to legal obligations associated with the retirement of long-lived assets that result from the acquisition, construction, development and/or the normal operation of a long-lived asset. A legal obligation is an obligation that a party is required to settle ...

... The accounting guidance in ASC 410-20 applies to legal obligations associated with the retirement of long-lived assets that result from the acquisition, construction, development and/or the normal operation of a long-lived asset. A legal obligation is an obligation that a party is required to settle ...

Fair Value Measurement (Topic 820)

... rather than its gross exposure, to those risks. Financial institutions and similar reporting entities that hold financial assets and financial liabilities often manage those instruments on the basis of their net risk exposure. That exception permits a reporting entity to measure the fair value of su ...

... rather than its gross exposure, to those risks. Financial institutions and similar reporting entities that hold financial assets and financial liabilities often manage those instruments on the basis of their net risk exposure. That exception permits a reporting entity to measure the fair value of su ...

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

... changes in the interest rate environment that reduce our margins or reduce the fair value of our financial instruments; ...

... changes in the interest rate environment that reduce our margins or reduce the fair value of our financial instruments; ...

2014 Annual Report - McDonald`s Corporation

... at various affordable price points in more than 100 countries. McDonald’s global system is comprised of both Company-owned and franchised restaurants. McDonald’s franchised restaurants are owned and operated under one of the following structures conventional franchise, developmental license or affil ...

... at various affordable price points in more than 100 countries. McDonald’s global system is comprised of both Company-owned and franchised restaurants. McDonald’s franchised restaurants are owned and operated under one of the following structures conventional franchise, developmental license or affil ...